#the federal reserve financial services

Photo

#ian connor#stacks#racks#money#bread#dough#cheese#fetti#breesh#federal reserve#the federal reserve financial services#mula#munyun#dinero#$100000#$100k#rackades

8 notes

·

View notes

Text

The Federal Reserve System: A Pillar of the U.S. Economy

Written by Delvin

Established in 1913, the Federal Reserve System, commonly known as the Fed, stands as the central banking system of the United States. Over the past century, the Fed has played a crucial role in maintaining financial stability, promoting economic growth, and safeguarding the nation’s monetary system. In this blog post, we will explore the key functions and responsibilities of…

View On WordPress

#Bank Supervision and Regulation#Central Banking System#dailyprompt#Federal Reserve#Financial#Financial Literacy#Financial System Stability#knowledge#Monetary Policy#money#Money Fun Facts#Payment Systems and Services#Research and Economic Analysis#The Federal Reserve System: A Pillar of the U.S. Economy

0 notes

Text

Fed ethics inquiry clears Powell and Clarida trades | Business News

Fed ethics inquiry clears Powell and Clarida trades | Business News

If you know of local business openings or closings, please notify us here.

PREVIOUS OPENINGS AND CLOSINGS

· Air Products and Chemicals Inc.’s chosen warehouse developer, Prologis Inc., will have to wait until July 13 for a final decision by Upper Macungie Township’s zoning hearing board on 2.61 million square feet of warehouses.

· Chubby’s of Southside Easton has added Krispy Krunchy Chicken to…

View On WordPress

#apmediaapi#Banking and credit#business#Central banking#Clarida#Clears#dcc#Economy#Ethics#Fed#federal reserve-trading#Financial crisis#Financial Markets#Financial services#general news#government and politics#inquiry#investment management#News#political ethics#political issues#Powell#private equity management#trades#Wire

0 notes

Note

Why do you think tumblr will die in only a few years?

Answer with jargon: a strong correlation between recent economic shifts and chaotic choices by major tech companies is most easily explained if the 'traditional' social media platforms of 2005-2020 are mostly a zero-interest rate phenomenon.

Longer answer, with less jargon: Even though Musk's takeover is making all the headlines recently, the last year has in fact seen major shakeups at many social media platforms, so Twitter is actually part of a trend. Almost inevitably, these are cases of social media companies trying to find a way to squeeze more money out of their userbase (Reddit), cut costs dramatically (Twitter), or both. This marks a sudden departure from a much more relaxed attitude towards revenue in the Pictures Of Cats industry, where the focus was historically more on expanding the userbase to a global scale and then counting on world domination to sort of <????> and then the company would become profitable eventually.

We joke, correctly, that Tumblr has never been profitable. But the entire structure of ad-supported content curation between human users is deeply suspect as a business model; IIRC Twitter was never profitable either, and Facebook has been juicing its numbers in very shenanigany ways. Discord was actually making money on net last I checked, at least a bit, so they're not all completely in the hole. But even if you take the accounting figures at face value, none of these companies has anything like the amount of money that their cultural prominence would suggest. Instead, they're heavily fueled by investment dollars, money given by super-rich people and institutions in the expectation that fueling the growth of the company now will pay off with interest later.

So what changed?

I'm not an expert here, but I'll do my best to muddle through. The American Federal Reserve has one mandate that dominates all others (sometimes called the 'dual mandate'), and one primary tool that it uses to enforce that mandate. The goal is to maintain low (but nonzero) rates of inflation and unemployment, which in their models are deeply interlinked phenomena. The tool is 'rate hikes', or more specifically, tweaking the mandatory rate of interest that banks charge one another when making loans.

As a particular consequence of this, hiking the rate also means that bonds start paying out much better. When the rate hike goes through, that affects people who let the government borrow their personal cash- that is, people who buy bonds- as well as institutions like banks that lend to one another. A rate hike means that you, personally, can make a little extra money by letting the government borrow it for a while. The federal government of the US is a rock-solid low-risk choice for this kind of moneymaking scheme, so the federal interest rate sort of defines the 'number to beat'; to attract investors, a company has to give those investors money at a better percentage than whatever the feds are offering. Particularly since a company is a lot more likely to go out of business than the state!

To wrap this back around to the Pictures Of Cats industry: the higher the rate hike, the better your company needs to be doing (or the less risky it needs to be as an option) to attract big investment dollars. Very high rates make it very hard to convince people to invest in business activity rather than the government itself, and very low rates put moonshots and big dreams on the table, investment-wise, in a way that wouldn't otherwise be possible. Social media companies were one of these big dreams.

In the great financial crisis of 2008, the Fed took the dramatic step of reducing their rate to zero, trying to juice the economy back to life. And ever since then, they've kept it there. This has produced an unprecedented amount of funding for very crazy stuff; it's part of what has allowed so many weird new tech companies (Uber, streaming services, etc.) to get so much money, so quickly, and use that to grow to massive size without a clear model of how they're ever going to make money. This state of affairs kept going for quite a while, with no clear stopping point; that zero-interest environment has been one of the shadowy forces in the background that shaped fundamental contours and limits in how our Very Online World has grown and developed. Until COVID.

Or rather, the bounce back from COVID: we suddenly saw a massive spike in inflation and an incredibly strong labor market, as employees quit in record numbers, negotiated higher salaries, and found better work, and at the same time supply chain issues and other economy stuff caused prices to climb dramatically. Recall the Fed's 'dual mandate', to control the employment rate and inflation. This was, basically, kicking them right in the jooblies. They responded in kind, finally finally raising their rates for the first time in 15 years. For some of the people reading this, it'll be the first significant shift in their entire adult lives.

The goal, as I understand it, is to fight inflation by reducing the amount of outside investment into private companies, forcing them to hire fewer people and pay smaller salaries, ultimately drawing money out of the working economy and driving prices back down by lowering demand for everything. You get paid less, so you eat out less, and buy at cheaper restaurants when you do, so restaurants have to compete harder by lowering their prices; seems pretty dodgy to me as a theory, but it's the theory. And the first part will almost certainly work- companies are going to see less investment.

For social media companies that are still paying most of their salaries with investor dollars instead of revenues, this is especially catastrophic. Without outside investment, they're just a massive pile of expenses waiting to happen, huge yearly costs in developer salaries and server fees. This is why, all of a sudden, every social media company is suddenly making bonkers decisions. They're noticing that nobody wants to give them any more money! So they're trying to figure out how to live a lot more cheaply, to actually somehow for reals turn their giant userbases in to some kind of actual revenue stream, or both.

Tumblr is kind of the ur-example of this kind of thing, supporting a very large userbase with no coherent plan whatsoever to start paying its staff with our dollars instead of investors' dollars. When interest rates were low and Scrooge McDuck had nowhere else to hide his pile of gold coins, a crazy kid with a dream was the best alternative available to him. But now, unless something changes, he's going to notice he can just buy bonds instead, and that crazy kid can go take a hike.

That's why I think Tumblr is living on borrowed time, though I don't know how much. Like all cartoons, the economy doesn't really fall off a cliff until somebody looks down and notices they've been standing on thin air this whole time. But they always fall eventually; that's the gag.

#I am not an economics#so if somebody wants to grade my accuracy here#that would be welcome#this is the situation as I understand it but my models are hazy

2K notes

·

View notes

Text

Why the Fed wants to crush workers

The US Federal Reserve has two imperatives: keeping employment high and inflation low. But when these come into conflict — when unemployment falls to near-zero — the Fed forgets all about full employment and cranks up interest rates to “cool the economy” (that is, “to destroy jobs and increase unemployment”).

An economy “cools down” when workers have less money, which means that the prices offered for goods and services go down, as fewer workers have less money to spend. As with every macroeconomic policy, raising interest rates has “distributional effects,” which is economist-speak for “winners and losers.”

Predicting who wins and who loses when interest rates go up requires that we understand the economic relations between different kinds of rich people, as well as relations between rich people and working people. Writing today for The American Prospect’s superb Great Inflation Myths series, Gerald Epstein and Aaron Medlin break it down:

https://prospect.org/economy/2023-01-19-inflation-federal-reserve-protects-one-percent/

Recall that the Fed has two priorities: full employment and low interest rates. But when it weighs these priorities, it does so through “finance colored” glasses: as an institution, the Fed requires help from banks to carry out its policies, while Fed employees rely on those banks for cushy, high-paid jobs when they rotate out of public service.

Inflation is bad for banks, whose fortunes rise and fall based on the value of the interest payments they collect from debtors. When the value of the dollar declines, lenders lose and borrowers win. Think of it this way: say you borrow $10,000 to buy a car, at a moment when $10k is two months’ wages for the average US worker. Then inflation hits: prices go up, workers demand higher pay to keep pace, and a couple years later, $10k is one month’s wages.

If your wages kept pace with inflation, you’re now getting twice as many dollars as you were when you took out the loan. Don’t get too excited: these dollars buy the same quantity of goods as your pre-inflation salary. However, the share of your income that’s eaten by that monthly car-loan payment has been cut in half. You just got a real-terms 50% discount on your car loan!

Inflation is great news for borrowers, bad news for lenders, and any given financial institution is more likely to be a lender than a borrower. The finance sector is the creditor sector, and the Fed is institutionally and personally loyal to the finance sector. When creditors and debtors have opposing interests, the Fed helps creditors win.

The US is a debtor nation. Not the national debt — federal debt and deficits are just scorekeeping. The US government spends money into existence and taxes it out of existence, every single day. If the USG has a deficit, that means it spent more than than it taxed, which is another way of saying that it left more dollars in the economy this year than it took out of it. If the US runs a “balanced budget,” then every dollar that was created this year was matched by another dollar that was annihilated. If the US runs a “surplus,” then there are fewer dollars left for us to use than there were at the start of the year.

The US debt that matters isn’t the federal debt, it’s the private sector’s debt. Your debt and mine. We are a debtor nation. Half of Americans have less than $400 in the bank.

https://www.fool.com/the-ascent/personal-finance/articles/49-of-americans-couldnt-cover-a-400-emergency-expense-today-up-from-32-in-november/

Most Americans have little to no retirement savings. Decades of wage stagnation has left Americans with less buying power, and the economy has been running on consumer debt for a generation. Meanwhile, working Americans have been burdened with forms of inflation the Fed doesn’t give a shit about, like skyrocketing costs for housing and higher education.

When politicians jawbone about “inflation,” they’re talking about the inflation that matters to creditors. Debtors — the bottom 90% — have been burdened with three decades’ worth of steadily mounting inflation that no one talks about. Yesterday, the Prospect ran Nancy Folbre’s outstanding piece on “care inflation” — the skyrocketing costs of day-care, nursing homes, eldercare, etc:

https://prospect.org/economy/2023-01-18-inflation-unfair-costs-of-care/

As Folbre wrote, these costs are doubly burdensome, because they fall on family members (almost entirely women), who have to sacrifice their own earning potential to care for children, or aging people, or disabled family members. The cost of care has increased every year since 1997:

https://pluralistic.net/2023/01/18/wages-for-housework/#low-wage-workers-vs-poor-consumers

So while politicians and economists talk about rescuing “savers” from having their nest-eggs whittled away by inflation, these savers represent a minuscule and dwindling proportion of the public. The real beneficiaries of interest rate hikes isn’t savers, it’s lenders.

Full employment is bad for the wealthy. When everyone has a job, wages go up, because bosses can’t threaten workers with “exile to the reserve army of the unemployed.” If workers are afraid of ending up jobless and homeless, then executives seeking to increase their own firms’ profits can shift money from workers to shareholders without their workers quitting (and if the workers do quit, there are plenty more desperate for their jobs).

What’s more, those same executives own huge portfolios of “financialized” assets — that is, they own claims on the interest payments that borrowers in the economy pay to creditors.

The purpose of raising interest rates is to “cool the economy,” a euphemism for increasing unemployment and reducing wages. Fighting inflation helps creditors and hurts debtors. The same people who benefit from increased unemployment also benefit from low inflation.

Thus: “the current Fed policy of rapidly raising interest rates to fight inflation by throwing people out of work serves as a wealth protection device for the top one percent.”

Now, it’s also true that high interest rates tend to tank the stock market, and rich people also own a lot of stock. This is where it’s important to draw distinctions within the capital class: the merely rich do things for a living (and thus care about companies’ productive capacity), while the super-rich own things for a living, and care about debt service.

Epstein and Medlin are economists at UMass Amherst, and they built a model that looks at the distributional outcomes (that is, the winners and losers) from interest rate hikes, using data from 40 years’ worth of Fed rate hikes:

https://peri.umass.edu/images/Medlin_Epstein_PERI_inflation_conf_WP.pdf

They concluded that “The net impact of the Fed’s restrictive monetary policy on the wealth of the top one percent depends on the timing and balance of [lower inflation and higher interest]. It turns out that in recent decades the outcome has, on balance, worked out quite well for the wealthy.”

How well? “Without intervention by the Fed, a 6 percent acceleration of inflation would erode their wealth by around 30 percent in real terms after three years…when the Fed intervenes with an aggressive tightening, the 1%’s wealth only declines about 16 percent after three years. That is a 14 percent net gain in real terms.”

This is why you see a split between the one-percenters and the ten-percenters in whether the Fed should continue to jack interest rates up. For the 1%, inflation hikes produce massive, long term gains. For the 10%, those gains are smaller and take longer to materialize.

Meanwhile, when there is mass unemployment, both groups benefit from lower wages and are happy to keep interest rates at zero, a rate that (in the absence of a wealth tax) creates massive asset bubbles that drive up the value of houses, stocks and other things that rich people own lots more of than everyone else.

This explains a lot about the current enthusiasm for high interest rates, despite high interest rates’ ability to cause inflation, as Joseph Stiglitz and Ira Regmi wrote in their recent Roosevelt Institute paper:

https://rooseveltinstitute.org/wp-content/uploads/2022/12/RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

The two esteemed economists compared interest rate hikes to medieval bloodletting, where “doctors” did “more of the same when their therapy failed until the patient either had a miraculous recovery (for which the bloodletters took credit) or died (which was more likely).”

As they document, workers today aren’t recreating the dread “wage-price spiral” of the 1970s: despite low levels of unemployment, workers wages still aren’t keeping up with inflation. Inflation itself is falling, for the fairly obvious reason that covid supply-chain shocks are dwindling and substitutes for Russian gas are coming online.

Economic activity is “largely below trend,” and with healthy levels of sales in “non-traded goods” (imports), meaning that the stuff that American workers are consuming isn’t coming out of America’s pool of resources or manufactured goods, and that spending is leaving the US economy, rather than contributing to an American firm’s buying power.

Despite this, the Fed has a substantial cheering section for continued interest rates, composed of the ultra-rich and their lickspittle Renfields. While the specifics are quite modern, the underlying dynamic is as old as civilization itself.

Historian Michael Hudson specializes in the role that debt and credit played in different societies. As he’s written, ancient civilizations long ago discovered that without periodic debt cancellation, an ever larger share of a societies’ productive capacity gets diverted to the whims of a small elite of lenders, until civilization itself collapses:

https://www.nakedcapitalism.com/2022/07/michael-hudson-from-junk-economics-to-a-false-view-of-history-where-western-civilization-took-a-wrong-turn.html

Here’s how that dynamic goes: to produce things, you need inputs. Farmers need seed, fertilizer, and farm-hands to produce crops. Crucially, you need to acquire these inputs before the crops come in — which means you need to be able to buy inputs before you sell the crops. You have to borrow.

In good years, this works out fine. You borrow money, buy your inputs, produce and sell your goods, and repay the debt. But even the best-prepared producer can get a bad beat: floods, droughts, blights, pandemics…Play the game long enough and eventually you’ll find yourself unable to repay the debt.

In the next round, you go into things owing more money than you can cover, even if you have a bumper crop. You sell your crop, pay as much of the debt as you can, and go into the next season having to borrow more on top of the overhang from the last crisis. This continues over time, until you get another crisis, which you have no reserves to cover because they’ve all been eaten up paying off the last crisis. You go further into debt.

Over the long run, this dynamic produces a society of creditors whose wealth increases every year, who can make coercive claims on the productive labor of everyone else, who not only owes them money, but will owe even more as a result of doing the work that is demanded of them.

Successful ancient civilizations fought this with Jubilee: periodic festivals of debt-forgiveness, which were announced when new monarchs assumed their thrones, or after successful wars, or just whenever the creditor class was getting too powerful and threatened the crown.

Of course, creditors hated this and fought it bitterly, just as our modern one-percenters do. When rulers managed to hold them at bay, their nations prospered. But when creditors captured the state and abolished Jubilee, as happened in ancient Rome, the state collapsed:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Are we speedrunning the collapse of Rome? It’s not for me to say, but I strongly recommend reading Margaret Coker’s in-depth Propublica investigation on how title lenders (loansharks that hit desperate, low-income borrowers with triple-digit interest loans) fired any employee who explained to a borrower that they needed to make more than the minimum payment, or they’d never pay off their debts:

https://www.propublica.org/article/inside-sales-practices-of-biggest-title-lender-in-us

[Image ID: A vintage postcard illustration of the Federal Reserve building in Washington, DC. The building is spattered with blood. In the foreground is a medieval woodcut of a physician bleeding a woman into a bowl while another woman holds a bowl to catch the blood. The physician's head has been replaced with that of Federal Reserve Chairman Jerome Powell.]

#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters

465 notes

·

View notes

Text

Supreme Court poised to appoint federal judges to run the US economy.

January 18, 2024

ROBERT B. HUBBELL

JAN 17, 2024

The Supreme Court heard oral argument on two cases that provide the Court with the opportunity to overturn the “Chevron deference doctrine.” Based on comments from the Justices, it seems likely that the justices will overturn judicial precedent that has been settled for forty years. If they do, their decision will reshape the balance of power between the three branches of government by appointing federal judges as regulators of the world’s largest economy, supplanting the expertise of federal agencies (a.k.a. the “administrative state”).

Although the Chevron doctrine seems like an arcane area of the law, it strikes at the heart of the US economy. If the Court were to invalidate the doctrine, it would do so in service of the conservative billionaires who have bought and paid for four of the justices on the Court. The losers would be the American people, who rely on the expertise of federal regulators to protect their water, food, working conditions, financial systems, public markets, transportation, product safety, health care services, and more.

The potential overruling of the Chevron doctrine is a proxy for a broader effort by the reactionary majority to pare the power of the executive branch and Congress while empowering the courts. Let’s take a moment to examine the context of that effort.

But I will not bury the lead (or the lede): The reactionary majority on the Court is out of control. In disregarding precedent that conflicts with the conservative legal agenda of its Federalist Society overlords, the Court is acting in a lawless manner. It is squandering hard-earned legitimacy. It is time to expand the Court—the only solution that requires a simple majority in two chambers of Congress and the signature of the president.

The “administrative state” sounds bad. Is it?

No. The administrative state is good. It refers to the collective body of federal employees, regulators, and experts who help maintain an orderly US economy. Conservatives use the term “administrative state” to denigrate federal regulation and expertise. They want corporations to operate free of all federal restraint—free to pollute, free to defraud, free to impose dangerous and unfair working conditions, free to release dangerous products into the marketplace, and free to engage in deceptive practices in public markets.

The US economy is the largest, most robust economy in the world because federal regulators impose standards for safety, honesty, transparency, and accountability. Not only is the US economy the largest in the world (as measured by nominal GDP), but its GDP per capita ($76,398) overshadows that of the second largest economy, China ($12,270). The US dollar is the reserve currency for the world and its markets are a haven for foreign investment and capital formation. See The Top 25 Economies in the World (investopedia.com)

US consumers, banks, investment firms, and foreign investors are attracted to the US economy because it is regulated. US corporations want all the benefits of regulations—until regulations get in the way of making more money. It is at that point that the “administrative state” is seen as “the enemy” by conservatives who value profit maximization above human health, safety, and solvency.

It is difficult to comprehend how big the US economy is. To paraphrase Douglas Adams’s quote about space, “It’s big. Really big. You just won't believe how vastly, hugely, mindbogglingly big it is.” Suffice to say, the US economy is so big it cannot be regulated by several hundred federal judges with dockets filled with criminal cases and major business disputes.

Nor can Congress pass enough legislation to keep pace with ever changing technological and financial developments. Congress can’t pass a budget on time; the notion that it would be able to keep up with regulations necessary to regulate Bitcoin trading in public markets is risible.

What is the Chevron deference doctrine?

Managing the US economy requires hundreds of thousands of subject matter experts—a.k.a. “regulators”—who bring order, transparency, and honesty to the US economy. Those experts must make millions of judgments each year in creating, implementing and applying federal regulations.

And this is where the “Chevron deference doctrine” comes in. When federal experts and regulators interpret federal regulations in esoteric areas such as maintaining healthy fisheries, their decisions should be entitled to a certain amount of deference. And they have received such deference since 1984, when the US Supreme Court created a rule of judicial deference to decisions by federal regulators in the case of Chevron v. NRDC.

What happened at oral argument?

In a pair of cases, the US Supreme Court heard argument on Tuesday as to whether the Chevron deference doctrine should continue—or whether the Court should overturn the doctrine and effectively throw out 17,000 federal court decisions applying the doctrine. According to Court observers, including Mark Joseph Stern of Slate, the answer is “Yes, the Court is poised to appoint federal judges as regulators of the US economy.” See Mark Joseph Stern in Slate, The Supreme Court is seizing more power from Democratic presidents. (slate.com)

I recommend Stern’s article for a description of the grim atmosphere at the oral argument—kind of “pre-demise” wake for the Chevron deference doctrine. Stern does a superb job of explaining the effects of overruling Chevron:

Here’s the bottom line: Without Chevron deference, it’ll be open season on each and every regulation, with underinformed courts playing pretend scientist, economist, and policymaker all at once. Securities fraud, banking secrecy, mercury pollution, asylum applications, health care funding, plus all manner of civil rights laws: They are ultravulnerable to judicial attack in Chevron’s absence. That’s why the medical establishment has lined up in support of Chevron, explaining that its demise would mark a “tremendous disruption” for patients and providers; just rinse and repeat for every other area of law to see the convulsive disruptions on the horizon.

The Kochs and the Federalist Society have bought and paid for this sad outcome. The chaos that will follow will hurt consumers, travelers, investors, patients and—ultimately—American businesses, who will no longer be able to rely on federal regulators for guidance as to the meaning of federal regulations. Instead, businesses will get an answer to their questions after lengthy, expensive litigation before overworked and ill-prepared judges implement a political agenda.

Expand the Court. Disband the reactionary majority by relegating it to an irrelevant minority. If we win control of both chambers of Congress in 2024 and reelect Joe Biden, expanding the Court should be the first order of business.

[Robert B. Hubbell Newsletter]

#Corrupt SCOTUS#Robert B. Hubbell#Robert b. Hubbell Newsletter#Expand the Court#Chevron deference#regulatory agencies#consumer protection#government by Federalist Society

78 notes

·

View notes

Text

Have a Heart Day 2024

This is a letter I wrote to the Canadian Government for Have a Heart Day 2024. I am asking the government to stop discriminating against First Nations children, to stop giving them inadequate services, education, and support, to stop treating them unequally compared to non-Indigenous children, and to stop taking them away from their loving families. I really hope that you read my letter and that you either copy paste it or write your own, and email the Canadian government yourself.

Hello. Our names are ____ and we are people from various parts of so-called Canada. We are writing to you to ask that you ensure the government stops discriminating against First Nations children, by signing a Final Settlement Agreement on Reform that meets and goes beyond the Agreement in Principle on Reform, and by following the Spirit Bear Plan and enshrining it into law.

First Nations children and families on reserves are being discriminated against in many ways. Most communities do not receive the same amount of and access to social services that non-Indigenous people receive. Most communities do not receive as good quality social services as non-Indigenous people. While there has been progress, Jordan's Principle, which is about meeting children's needs, is still not being properly applied. Most children don't have access to an equal quality of education as children off reserves, and many children receive very inadequate education services. And, very horrifyingly, children are being separated from families who love them and want to take care of them. This all needs to stop. We need to make, follow, and enforce laws that stop this discrimination.

First of all, let's talk about the fact that social services are inadequate on most reserves. As you know, the federal government funds services on reserves that the provincial or municipal governments fund elsewhere. The government generally funds services on reserves far less than services are funded off reserves. These include education, water infrastructure, housing, financial assistance, transportation, basic infrastructure, utilities, healthcare, mental healthcare, addiction support, job training, childcare, youth programs, cultural programs, recreation programs, libraries, child welfare, and more. These services are human rights and should be well-funded for everyone. It's not fair that non-Indigenous people have better services to better meet more of their fundamental human rights and basic needs while people on reserves don't.

The fact that people don't have access to the services they need is part of why there are high levels of poverty on reserves. Ongoing and historical racism, trauma, and discrimination have caused a lot of people on reserves to be poor. And this lack of services is part of that discrimination that is causing people to be poor. If people had the healthcare, education, housing, childcare, mental healthcare, addiction support, cultural support, job training, basic food and water, disability support, and other things they needed, they would be able to have the peace of mind, mental strength, knowledge, support, and resources necessary to pull themselves and their communities out of poverty. Also, since there is so much poverty on reserves, these communities need even more services to help meet their basic needs and human rights.

Services delivered need to be good and effective for the communities they are delivered in. This means that services need to meet each community's different needs. Because each community has different needs due to different connectivity to the outside world, poverty levels, local prices, etc. Service providers need to first see what services people need and how to best deliver them, then work out how much money is needed. Money should be the last thing considered. What each person, family, and community needs should be the first thing considered. And of course, services must all be culturally sensitive and relevant.

And part of why services are so low quality, as well as part of why so much discrimination and cruelty happens, is because Indigenous Services Canada has biases in its systems and people, and must be reformed. Indigenous Services Canada doesn't listen to experts about what communities need and how things should be done. They don't try to do their actual job, which is ensuring good services are provided to Indigenous people. They need to be reformed and communities need to lead their own service provision.

The Spirit Bear plan must be properly implemented and properly followed. It must be enshrined in law and the law must be completely enforced. The Spirit Bear Plan is the following:

"Spirit Bear calls on:

CANADA to immediately comply with all rulings by the Canadian Human Rights Tribunal ordering it to immediately cease its discriminatory funding of First Nations child and family services. The order further requires Canada to fully and properly implement Jordan's Principle (www.jordansprinciple.ca).

PARLIAMENT to ask the Parliamentary Budget Officer to publicly cost out the shortfalls in all federally funded public services provided to First Nations children, youth and families (education, health, water, child welfare, etc.) and propose solutions to fix it.

GOVERNMENT to consult with First Nations to co-create a holistic Spirit Bear Plan to end all of the inequalities (with dates and confirmed investments) in a short period of time sensitive to children's best interests, development and distinct community needs.

GOVERNMENT DEPARTMENTS providing services to First Nations children and families to undergo a thorough and independent 360° evaluation to identify any ongoing discriminatory ideologies, policies or practices and address them. These evaluation must be publicly available.

ALL PUBLIC SERVANTS including those at a senior level, to receive mandatory training to identify and address government ideology, policies and practices that fetter the implementation of the Truth and Reconciliation Commission's Calls to Action." This information is from the First Nations Child and Family Caring Society.

Another huge factor contributing to the inequality faced by many First Nations children is the fact that Jordan's Principle isn't being properly implemented.

The federal government, not the provincial government, typically pays for the services on reserves. But many times disputes arise about who should pay for a service, and the children don't get the services non-Indigenous children would get as a matter of course. Jordan's Principle is named after Jordan River Anderson, a young disabled boy from Norway House Cree Nation who passed away in the hospital after the provincial government and the federal government couldn't decide which one should pay the costs of his healthcare. The Principle states that if a First Nations child needs something for their well-being, they need to be given that service first and payment disputes should get addressed later. This includes medical, psychological, educational, cultural, disability, and basic needs support. Non-Indigenous children get these supports without having to ask because they have access to many more and better services. These supports are human rights that everyone deserves, especially children going through generational and contemporary trauma.

Jordan's Principle is not being properly implemented, and this is hurting kids. Though there has been much progress, Jordan's Principle requests, which are for things children need, are often denied, which goes against children's rights. Indigenous Services Canada, which runs the Jordan's Principle approval process, doesn't have an adequate complaints mechanism to hold to account its provision of the Principle. The government isn't making data available on whether they're meeting children's needs. Many children have delays in getting help, including time-sensitive medical, psychological, educational, and development help.

The application process, though easier than before, is still difficult and many families don't have adequate help and guidance through it. As well, most doctors don't know which children are eligible for Jordan's Principle supports, 40% don't know which services are covered, and ⅓ don't know how to access funding through it.

Long term reform is needed. An Agreement in Principle on long term reform has been drafted by the government and First Nations advocates, and it looks promising. It talks about increasing funding for Jordan's Principle services and trying to root out prejudice in the system. But the Agreement in Principle is not legally binding. It's not something the government has to follow, or is following, but rather what they claim they might do eventually. Negotiations for the creation of a Final Settlement Agreement based on the Agreement in Principle were underway but have been on standstill for months. A Final Settlement Agreement would be legally binding and would if done right increase the chances of achieving change.

The school system is also horribly unfair. Many First Nations schools on reserves get less funding than schools off reserve, with an average of 30% less funding per school. They don't have adequate funding for computers, software, technology, sports equipment, field trips, labs, lab equipment, extracurriculars, cultural learning, job training, and the list goes on. They don't even have enough money to have adequate heating, good quality infrastructure, adequate and safe ventilation, enough textbooks, and reasonable class sizes. Many schools don't have a safe and appropriate learning environment. All children, including First Nations children, deserve good education.

There is no clear plan to eliminate education and employment gaps.

The government claims it's negotiating with Indigenous groups but there's no evidence that they're actually doing anything to lower inequality. They also claim that they're funding education on reserves equally but all the evidence says they're not. You need to actually, genuinely fund education on reserves adequately and equitably, and make sure that children on reserves are actually receiving a good and equal and equitable quality of education.

A lot of communities don't have self-determination over their own education systems, meaning they can't teach about the history of their people and other important cultural knowledge. First Nations children need and deserve to learn about their culture, about the ecosystems their people are connected to and how to interact with those ecosystems, their history, their language, their traditions. And if communities have self-determination over their own education systems, and they have adequate resources and funding from the government, they'll be able to teach these things so that children grow up proud of who they are.

And what is perhaps the most horrible thing is that so many children are being separated from families who love them. This is the most traumatic thing that can happen to a child, and all children deserve and need to be with the families who love them.

At the height of residential schools, many children were separated from their families. Currently, 3 times as many children are in foster care, away from their families. One tenth of First Nations children have been in foster care. Children in foster care experience higher rates of physical and sexual abuse and do not get as much cultural immersion. Not to mention, even in the best circumstances, they're away from their families.

Most Indigenous children in foster care have loving families that try their best to take care of them, who they want and need deeply. But their families are poor or mentally ill or disabled, or have other factors that make it hard for them to meet their children's needs. Preventative support like financial, housing, health, and mental health aid could keep many families together. If child and family service agencies have the resources and the empathy to help families with what they need so that families stay together, that would be a great relief. Child and family service agencies need adequate money, infrastructure, and personnel to give families real help instead of taking children away. Most agencies do not have these. Programs that help the wider community such as healthcare, financial aid, housing services, mental healthcare, parenting classes, food support, community programs, youth programs, cultural programs, pregnancy support, and others would greatly decrease the number of children taken from their homes. Most communities do not have adequate levels of these programs.

Child and family service agencies need to be completely reformed, and should be led by First Nations communities themselves. Most child and family service agencies are not. This is especially important since there is bias against First Nations people in many agencies. Some communities are getting the opportunities to start their own child and family service agencies, but most communities do not have this opportunity. Canada needs binding laws to ensure child and family service agencies are led by First Nations communities and are based in the unique culture of each community, which they often aren't. Each community has unique needs depending on local prices, remoteness, poverty levels, and other factors. The way child and family services should be funded is by first seeing what services the children truly need, then seeing how to best deliver them, then determining how much money will be needed.

There is a promising Agreement in Principle on Reform, created by the government and First Nations advocates. It discusses increasing funding for child welfare services and trying to root out prejudice in the system. However this is not a legally binding agreement that the government has to follow. It's just something that they claim they'll maybe do in the future. A Final Settlement Agreement based on the Agreement in Principle would be legally binding. It would, if done right, enact more funding and reform. But negotiations for this have been on pause for months. Canada needs to implement evidence-based solutions to keep kids with their families. This means creating a legally binding and well-enforced Final Settlement Agreement on Reform that meets and goes beyond the Agreement in Principle on Reform.

Some communities are trying a new funding model for child and family services that may give more funding, allowing them to do more preventative services instead of taking children away. However, the results of this new funding model are not clear yet, and most communities do not have the opportunity to be funded by it. And there is no guarantee that the new funding model will be applied to all communities if it indeed does work. There is no guarantee that enough funding for prevention services will be given to all communities, whether or not the new funding model works.

The government often promises to create reform or adequately fund things, but they don't follow through on those promises. If the government does make progress, safeguards need to be in place to stop them from backsliding.

So here are our asks for you:

-Implement the Spirit Bear plan and adequately fund all social services on reserves.

-Make sure all services are available de facto just like they are off reserve.

-Fund cultural services and make sure all services are culturally-rooted.

-Eliminate all discrimination and bias in service providers.

-Listen to experts such as doctors and teachers, the community, and community-led service providers.

-Allow and help First Nations communities to lead their own social services rooted in their own cultural values.

-Keep funding flexible and adaptable to changing needs.

-Have adequate accountability measures for all service providers.

-Make a binding law to adequately fund all social services and have communities lead social service provision.

-Create a binding law to ensure that once you start adequately funding social services you don't stop.

-In a reasonable timeframe, reach a Final Settlement Agreement on Long-Term Reform that meets and goes beyond the Agreement in Principle.

-Make sure all Jordan's Principle requests in the best interests of children are accepted.

-Give presumptive approval for Jordan's Principle requests under $250.

-Support organizations and communities already providing Jordan's Principle services.

-Accept urgent requests within 12 hours and non urgent requests within 48 hours.

-Don't require more than one document from a professional or elder for making requests.

-Make data available on Jordan's Principle provision effectiveness.

-Make sure all supports are given in a timely manner without delays.

-Make it easy and convenient for families and professionals to make Jordan's Principle requests.

-Fund schools on reserves as much as schools off reserve. This includes funding for computers, libraries, software, teacher training, special education, education research, language programs, cultural programs, mental health support, support for kids with special needs, extracurriculars, ventilation, heating, mold removal, vocation training for students, and more.

-Make sure all schools have the resources, funding, and support necessary to teach culture.

-Make a clear joint strategy to eliminate the education and employment gap.

-Make sure all school staff are non-discriminatory.

-Make sure communities have self-determination to create culturally rooted education.

-Adequately fund child and family services on reserves, and make sure they can hire enough people and have good infrastructure.

-Stop discrimination within child and family service agencies.

-Allow and help all First Nations communities to lead and run their own child and family service agencies that are based on their cultural values.

-Enact evidence based solutions to keep families together.

-Don't take children from families that love them.

-Have and fund adequate preventative services so families can take care of their children and no child is taken away.

-Keep funding for child and family services flexible and responsive to each community's needs, and listen to communities to learn what their needs are.

-Have adequate accountability in child and family services so that any underfunding, discrimination, or failure is stopped and remedied.

-Family support needs to start at or even before pregnancy.

-Fund culturally-based healing of people who have been harmed and are being harmed by the government's discrimination.

———

Find your MP here: https://www.ourcommons.ca/en/members

justin.trudeau(at)parl.gc.ca- Prime Minister Trudeau

chrystia.freeland(at)parl.gc.ca- Deputy Prime Minister Freeland

patty.hajdu(at)parl.gc.ca- Minister of Indigenous Services

gary.anand(at)parl.gc.ca - Minister of Crown-Indigenous Relations

#canadian#canada#canadian politics#cdnpoli#indigenous lives matter#indigenous rights#indigenous sovereignty#every child matters#bipoc lives matter#discrimination#racism#oppression#social juatice#child rights#children’s rights#social issues#inequality#injustice#family#community#childhood#childhood trauma#trauma#family separation#separation#hurt#pain#saddness#letter#action

49 notes

·

View notes

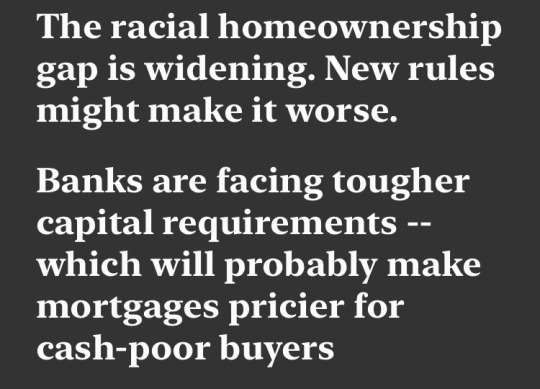

Text

Holy fuck they are hawking this bullshit again about high mortgage rates being racist

Borrowing costs for mortgages have more than doubled over the last two years as the Federal Reserve has battled inflation by hiking interest rates, which hit a 22-year high earlier this year. […]

The Financial Services Forum, representing eight of the biggest U.S. banks, said it is spending a seven-figure sum on television advertising blasting the proposal as an added fee on Americans already burdened by inflation.

“The fed has hiked interest rates to reduce inflation, and also as the Evil League of Evil points out, these high interest rates exacerbate the problem of inflation.” Could you try to hide the doublethink a bit harder?

After George Floyd’s murder ignited nationwide protests in the summer of 2020, corporations across the economy committed to projects aimed at battling systemic racism. Mortgage lenders pledged to work with financial regulators to provide credit to more minority borrowers.

“To honour the death of George floyd, we need to use interest rates to hike housing values.” Shameless. Just fucking shameless.

Then again, if she extends the lease on her two-bedroom apartment — where her 11-year-old son is sharing a bedroom with his 22-year-old brother — her rent will increase by $70 a month, to nearly $1,400.

“To hear costs just keep going up is really disheartening,” she said. “Where do they want people to live?”

If the problem this woman is facing is that the rent is too damn high, I think the natural thing to do would be to focus on policies with the ability to make the rent less damn high. But no, increasing homeownership forever at all costs is clearly the only solution, which actually dovetails with instead of flatly contradicting addressing the problem of rentiers being able to extort more money from their tenants bc of their high property values

Sen. Sherrod Brown (D-Ohio), who chairs the Senate Banking Committee, struck an incredulous tone over the industry’s lobbying push as the bank CEOs testified before the panel Wednesday.

“Wall Street banks are actually saying that cracking down on them will, quote, ‘hurt working families.’ Really?” he asked. “You’re going to claim that?”

Love that the obligatory “And now we will give coverage to the other side” section is just sherrod brown saying “Sorry do u expect me to actually swallow this tripe?” Lol

40 notes

·

View notes

Text

There were 173 Banks around the World that failed this week – and went unreported by the Mainstream Media.

The Rothschild Banks in controlled collapse, including the US Federal Reserve:

Afghanistan: Bank of Afghanistan

Albania: Bank of Albania

Algeria: Bank of Algeria

Argentina: Central Bank of Argentina

Armenia: Central Bank of Armenia

Aruba: Central Bank of Aruba

Australia: Reserve Bank of Australia

Austria: Austrian National Bank

Azerbaijan: Central Bank of Azerbaijan Republic

Bahamas: Central Bank of The Bahamas

Bahrain: Central Bank of Bahrain

Bangladesh: Bangladesh Bank

Barbados: Central Bank of Barbados

Belarus: National Bank of the Republic of Belarus

Belgium: National Bank of Belgium

Belize: Central Bank of Belize

Benin: Central Bank of West African States (BCEAO)

Bermuda: Bermuda Monetary Authority

Bhutan: Royal Monetary Authority of Bhutan

Bolivia: Central Bank of Bolivia

Bosnia: Central Bank of Bosnia and Herzegovina

Botswana: Bank of Botswana

Brazil: Central Bank of Brazil

Bulgaria: Bulgarian National Bank

Burkina Faso: Central Bank of West African States (BCEAO)

Burundi: Bank of the Republic of Burundi

Cambodia: National Bank of Cambodia

Came Roon: Bank of Central African States

Canada: Bank of Canada – Banque du Canada

Cayman Islands: Cayman Islands Monetary Authority

Central African Republic: Bank of Central African States

Chad: Bank of Central African States

Chile: Central Bank of Chile

China: The People’s Bank of China

Colombia: Bank of the Republic

Comoros: Central Bank of Comoros

Congo: Bank of Central African States

Costa Rica: Central Bank of Costa Rica

Côte d’Ivoire: Central Bank of West African States (BCEAO)

Croatia: Croatian National Bank

Cuba: Central Bank of Cuba

Cyprus: Central Bank of Cyprus

Czech Republic: Czech National Bank

Denmark: National Bank of Denmark

Dominican Republic: Central Bank of the Dominican Republic

East Caribbean Area: Eastern Caribbean Central Bank

Ecuador: Central Bank of Ecuador

Egypt: Central Bank of Egypt

El Salvador: Central Reserve Bank of El Salvador

Equatorial Guinea: Bank of Central African States

Estonia: Bank of Estonia

Ethiopia: National Bank of Ethiopia

European Union: European Central Bank

Fiji: Reserve Bank of Fiji

Finland: Bank of Finland

France: Bank of France

Gabon: Bank of Central African States

The Gambia: Central Bank of The Gambia

Georgia: National Bank of Georgia

Germany: Deutsche Bundesbank

Ghana: Bank of Ghana

Greece: Bank of Greece

Guatemala: Bank of Guatemala

Guinea Bissau: Central Bank of West African States (BCEAO)

Guyana: Bank of Guyana

Haiti: Central Bank of Haiti

Honduras: Central Bank of Honduras

Hong Kong: Hong Kong Monetary Authority

Hungary: Magyar Nemzeti Bank

Iceland: Central Bank of Iceland

India: Reserve Bank of India

Indonesia: Bank Indonesia

Iran: The Central Bank of the Islamic Republic of Iran

Iraq: Central Bank of Iraq

Ireland: Central Bank and Financial Services Authority of Ireland

Israel: Bank of Israel

Italy: Bank of Italy

Jamaica: Bank of Jamaica

Japan: Bank of Japan

Jordan: Central Bank of Jordan

Kazakhstan: National Bank of Kazakhstan

Kenya: Central Bank of Kenya

Korea: Bank of Korea

Kuwait: Central Bank of Kuwait

Kyrgyzstan: National Bank of the Kyrgyz Republic

Latvia: Bank of Latvia

Lebanon: Central Bank of Lebanon

Lesotho: Central Bank of Lesotho

Libya: Central Bank of Libya (Their most recent conquest)

Uruguay: Central Bank of Uruguay

Advertisements

REPORT THIS AD

Lithuania: Bank of Lithuania

Luxembourg: Central Bank of Luxembourg

Macao: Monetary Authority of Macao

Macedonia: National Bank of the Republic of Macedonia

Madagascar: Central Bank of Madagascar

Malawi: Reserve Bank of Malawi

Malaysia: Central Bank of Malaysia

Mali: Central Bank of West African States (BCEAO)

Malta: Central Bank of Malta

Mauritius: Bank of Mauritius

Mexico: Bank of Mexico

Moldova: National Bank of Moldova

Mongolia: Bank of Mongolia

Montenegro: Central Bank of Montenegro

Morocco: Bank of Morocco

Mozambique: Bank of Mozambique

Namibia: Bank of Namibia

EVERYTHING is going to crash!

Are You Prepared? 🤔

#pay attention#educate yourself#educate yourselves#reeducate yourself#knowledge is power#reeducate yourselves#think for yourself#think for yourselves#think about it#do your homework#do your research#do your own research#question everything#ask yourself questions#ask yourself#central banking#everything is going to crash#everything is falling apart

112 notes

·

View notes

Text

By Prem Thakker

States across the country are moving to provide universal free school meals to all our children. Meanwhile, Republicans are trying to stop them from doing just that.

The Republican Study Committee (of which some three-quarters of House Republicans are members) on Wednesday released its desired 2024 budget, in which the party boldly declares its priority to eliminate the Community Eligibility Provision, or CEP, from the School Lunch Program. Why? Because “CEP allows certain schools to provide free school lunches regardless of the individual eligibility of each student.”

The horror.

Of note is that the CEP is not even something every school participates in; it is a meal service program reserved for qualifying schools and districts in low-income areas. The program enables schools that predominantly serve children from low-income backgrounds to offer all students free breakfast and lunch, instead of means-testing them and having to manage collecting applications on an individual basis. As with many universal-oriented programs, it is more practically efficient and, as a bonus, lifts all boats. This is what Republicans are looking to eliminate.

It’s the kind of provision that many would want every school to participate in. Why not guarantee all our children are well fed as they learn and think about our world and their place in it, after all?

But indeed, as California, Colorado, Maine, Minnesota, New Mexico, and as of this week, Vermont, all move to provide universal free school meals in one form or another—and at least another 21 states consider similar moves—Republicans are trying to whittle down avenues to accomplish that goal.

Along with trying to stop schools from giving all their students free meals, the proposed 2024 Republican budget includes efforts to:

• cut Social Security and Medicare

• make Trump’s tax cuts for the top 1% permanent

• impose work requirements on “all federal benefit programs,” like food stamps and Medicare

• extend work requirements on those aged 55–64

• bring back all of twice-impeached and twice-arrested former President Donald Trump’s deregulations, including the weakening of environmental protection.

And that’s just a taste of their hopes and dreams. But don’t mistake it all as just wish-casting: “The RSC Budget is more than just a financial statement. It is a statement of priorities,” the party assures in the document.

#us politics#news#the new republic#2023#republicans#conservatives#gop platform#gop policy#gop#Republican Study Committee#2024 Republican budget#Community Eligibility Provision#School Lunch Program#universal free school meals#California#Colorado#Maine#Minnesota#new mexico#Vermont#social security cuts#medicare cuts#trump tax cuts#work requirements#deregulation

77 notes

·

View notes

Text

In 2022, the first year of sharp rate hikes to curb rising inflation, the countries of the Global South paid almost $50 billion more in debt than they received in new financing, according to data from the UN’s trade and development arm

Crises, like successes, are seen through different eyes depending on who the passive subject is. And this is one of those silent shocks, a blind spot in the wide angle of the world economy. Far from the headlines, rising interest rates are taking their toll on emerging and developing countries: the Global South paid more on its debt last year in principal and interest repayments than it received in development aid and new loans. Inflows to this group of nations fell to their lowest level since the global financial crisis, according to figures from the NGO ONE Campaign. A warning sign that should give the Federal Reserve and the European Central Bank (ECB) pause for thought.

In 2022, the first year of sharp rate hikes to curb rising inflation, the countries of the Global South paid almost $50 billion more in debt than they received in new financing, according to data from the UN’s trade and development arm (UNCTAD). At the same time, official development assistance (ODA) fell for the second consecutive year and remained well below the target of 0.7% of gross national income (GNI). This target dates to the 1970s and, more than 50 years later, it has still not been met.

“We are witnessing a worrying trend: financial flows are flowing out of the developing countries that need them most and towards their creditors,” summarizes the head of UNCTAD, Rebeca Grynspan, in statements to EL PAÍS. “These are nations that need external resources to complement their internal efforts and, without a positive trend in external financing, their capacity for growth is severely limited.” The fiscal constraints imposed by this situation, she adds, make it almost impossible to achieve Sustainable Development Goals (SDGs): “Addressing the overlapping crises, such as the climate emergency, will be an unattainable challenge if these trends are not reversed.”

continue reading

#global south#debt repayments#greater than#development aid#sustainable development goals (SDGs)#nigh unachievable#capitalism

7 notes

·

View notes

Text

Millions of Americans strapped with student loan debt are still not paying their bills after a three-year payment hiatus ended this fall.

Federal student loan payments restarted at the beginning of October after President Biden declined to extend the pandemic-era pause that first began in March 2020 under his predecessor, former President Trump.

However, 40% of the 22 million borrowers who had bills due failed to make a payment as of mid-November, according to a new report published by the Department of Education. That means about 9 million Americans who have payments due are not making them.

The figure does not include borrowers who are still in school or who recently left and do not yet owe payments, or whose payment deadlines were extended due to loan servicing errors.

"While most borrowers have already made their first payment, others will need more time," Education Department Under Secretary James Kvaal wrote in the report. "Some are confused or overwhelmed about their options. We want to make sure borrowers know that our top priority is to support student loan borrowers as they return to repayment."

Although payments did not officially restart until the beginning of October, interest began accruing again on Sept. 1. As a result, borrowers who do not make payments now will see their payments continue to grow.

MANY STUDENT LOAN BORROWERS UNSURE HOW THEY’LL RESTART PAYMENTS AFTER PAUSE ENDS, SURVEY SAYS

The average monthly bill hovers between $200 and $299 per person, although it is even higher for some borrowers, according to the most recent Federal Reserve data.

Collectively, borrowers resumed paying about $10 billion a month in October, according to a separate analysis from JPMorgan.

The resumption of student loan payments comes as consumers continue to face sky-high interest rates and chronic inflation, which has rapidly eroded their purchasing power. Experts say the addition of student loan payments could deliver a financial shock to millions of Americans – and hinder their ability to shop at big-name stores like Target, Nike, Under Armour and Gap.

Many borrowers hoped that their loans would be wiped out, but the Supreme Court earlier this year struck down Biden's student loan forgiveness plan that would have erased up to $20,000 in loans per borrower.

Since then, the White House has announced other efforts to reduce student loan debt, including erasing $127 billion of debt owed by about 3.6 million borrowers.

14 notes

·

View notes

Text

BREAKING: House Financial Services Committee passes bill to ban the Federal Reserve from creating a Central Bank Digital Currency This is a huge step forward

22 notes

·

View notes

Text

For the past 25 years, Japan’s central bank and government have found common cause in trying to end deflationary pressures that have been seen as a drag on economic growth. Now that they are succeeding, the verdict is in: People don’t like it.

Under standard economic theory, high levels of deficit spending coupled with ultra-low interest rates should almost inevitably lead to higher rates of inflation—usually a problematic outcome for most economies. But Japan has become the poster child for the risks of the opposite problem, persistent price and wage deflation.

Former U.S. Federal Reserve Chairman Ben Bernanke was a strong advocate of action by the Bank of Japan (BOJ). “Addressing the deflation problem would bring substantial real and psychological benefits to the Japanese economy, and ending deflation would make solving the other problems that Japan faces only that much easier,” he said in an address to the Japan Society of Monetary Economics in May 2003, when he was still just a member of the Fed board. At stake, he said, was not just the economic health of Japan “but also, to a significant degree, the prosperity of the rest of the world.” His worries of a similar deflationary trap in the United States were one of the reasons he would later propose as Fed chairman the massive quantitative easing, or QE, program following the 2007-08 global financial crisis.

To achieve this, the BOJ first tried ultra-low interest rates and, when that failed, zero interest rates and finally negative interest rates. In addition, there were various programs to encourage lending, including special funding to banks that lend to smaller companies with growth potential and to banks that increased their lending by a certain amount. The lending initiatives ran into two primary obstacles: Japanese banks only want to lend money to companies that don’t need it (big companies in Japan sit on massive cash holdings), and with such low rates, the cost of initiating and servicing the loans outweighed the profits in terms of interest payments.

The ultimate plan to defeat all this came from the affable Haruhiko Kuroda, appointed in 2013 by newly elected Prime Minister Shinzo Abe as the head of the BOJ. Kuroda, a former Finance Ministry official who was therefore an outsider within the central bank, threw caution to the wind. He would, he promised, create 2 percent inflation in two years by doubling the BOJ’s balance sheet.

Moving beyond the Fed’s QE, Japan would have QQE, adding in the idea of qualitative to quantitative easing, meaning that the bank would not buy just government bonds but also riskier assets. The result was indeed a massive expansion in the balance sheet, in effect monetizing the government’s steady diet of fiscal overspending equal to around 30 percent of the total budget each year. Even though the balance sheet more than quadrupled over Kuroda’s 10-year term, the idea of a “virtuous cycle” of higher wages driving higher prices remained elusive for almost all of his tenure, with the consumer price index stuck around zero.

This was to change but not because of any central bank policy. Instead, it was due mainly to the world’s recent No. 1 game-changer: COVID-19. With higher import costs and supply chain disruptions, higher prices, albeit at a modest level by global standards, became visible in virtually every sector of the economy. By January 2023, the consumer price index jumped to 4 percent, the highest level since 1981 and well over the 2 percent target set by the BOJ. Within this, hotel prices have surged, rising 63 percent as foreign tourists again pack central Tokyo and Kyoto. For Japanese shoppers, much of the impact has been in the form of “shrinkflation” as food producers try to hide the higher costs. A bag of coffee in central Tokyo can still be found for around $4—it’s just that the same package now holds 40 percent less coffee. No wonder major food packaging companies saw their earnings jump 33 percent last year.

As a result, stagnant wages finally have started to show signs of movement as a shrinking workforce, good economic growth, and skills shortages have bid up salaries. Wages in October 2023 were up 1.5 percent year-on-year, and union workers logged average increases of 3.6 percent in their spring round of labor negotiations.

So why isn’t everyone happy? The reality is that the two growth lines have resulted in a steady decline in real wages adjusted for inflation. According to government figures, real wages fell for 20 consecutive months up to November 2023, registering a 3 percent decline year-on-year.

“People are not stupid,” said Jesper Koll, a global ambassador for the Monex Group and one of Japan’s best-known economists. “The 30 years of deflation have come to an end, but are the Japanese people getting the kind of inflation they want?”

Indeed, while deflation has had policymakers gnashing their teeth as Japan became relatively poorer (some tech jobs pay better in Vietnam than in Japan today), it was good for salaried workers who saw their pay rise modestly while prices would fall around 1 percent annually. The new scenario is more complex. As workers in any inflationary economy can attest, wages almost always rise more slowly than retail prices. One BOJ official in the pre-Kuroda days in 2012 said privately that their surveys showed people preferred deflation even as the central bank was trying to stamp it out.

The sticker shock of rising prices has been an unwanted blow to Prime Minister Fumio Kishida, who is facing a crisis in confidence for no clear reason—except that people don’t seem to like his administration. Kishida and U.S. President Joe Biden could no doubt commiserate on that front.

Last fall, when the government’s approval ratings fell below the “danger zone” of 30 percent—the figure that often heralds a party search for a fresh face as prime minister—Kishida started handing out cash that the government didn’t have, offering subsidies to limit the impact of higher prices in energy and utilities. Even this backfired badly, raising allegations that he was trying to buy his way back to popularity.

“What people are frustrated with is that he increases spending all the time but has no program to pay for it. The Japanese people are rational with their money—they don’t go out on spending sprees,” Koll said.

Kishida, who took office in October 2021, now has support of just above 20 percent by most polls, with two-thirds of respondents saying they disapprove of his administration. This would normally make him ripe for removal by the party elders who effectively control the ruling Liberal Democratic Party (LDP). That has been the model ever since the party was founded in 1955 and helped the LDP to remain in power for all but six years since then.

But Kishida may well survive for a while. The latest in a string of scandals also involves other senior figures in the LDP over potentially illegal fundraising, which has had the effect of shrinking the pool of potential successors. There is also no clear replacement for Kishida who would satisfy both the more liberal and hawkish wings of the party, part of the reason he got the job in the first place.

Another open question is whether Kishida—or a successor—will get to actually see an end to the 25 years of deflationary pressures. The latest inflation figures show a softening in price increases, with core inflation (without fresh food prices) rising just 2.5 percent in November 2023, its lowest in 16 months. That may be good news for consumers, but it has some economists skeptical over whether the economy has really turned the corner toward self-sustaining wage-price increases or if the new figures point to a consumer slowdown that would lead to a downturn. The focus will be on this spring’s union wage negotiations, where both the workers and the government are hopeful that increases will finally put workers ahead of inflation, at least for now. The companies that would have to pay for this have shown less enthusiasm.

But some economists remain skeptical. “I would venture that the wage hike to come during next spring’s negotiations won’t quite reach the level expected,” Takahide Kiuchi, an economist at the Nomura Research Institute and a former BOJ board member, wrote in a November report. He said this may prompt the BOJ to hold off on any changes to its negative rates. Japan remains the only country to maintain ultra-low rates as other advanced economies have switched to tighter money policies as inflation surged.

At the same time, Kiuchi noted, delaying for too long means the bank’s balance sheet will continue to grow as it buys bonds to keep yields at zero or below. This will increase the risks to its own financial position if interest rates rise in the future, since the massive holdings would plummet in value. With the balance sheet now larger than Japan’s annual GDP, the implications could be severe, a polite way of saying that it would face insolvency. If that happened, the government would be forced to bail it out. But the government is already using the BOJ to pay for its own financial excesses.

It’s all enough to leave the average Japanese yearning for the good old days of deflation.

17 notes

·

View notes

Note

Dearest Bitches,

I signed up for an Ally high interest savings account (per your suggestion)! And now they keep raising the interest rate, like, every week. Latest email:

"Your Online Savings Account rate is increasing from 2.25% to 2.35% Annual Percentage Yield (APY) on all balance tiers. Your new APY goes into effect on 10/20/2022, and will appear in your account on 10/21/2022. As you’re no doubt aware, the economy is a hot topic at the moment. From prices at the gas tank, to everyday groceries, inflation is having a real effect on wallets everywhere. But on the bright side, our rates have reached a new high. So now’s a great time to build your savings habits and save more on every dollar."

Is this good?? It seems like it should be good but why is this happening. Surely they're not just raising interest to be nice. Can you please explain? Is this a scam?

XOXO

This is a bit of a complicated answer. So I'll try to simplify.

THIS IS A GOOD THING FOR YOU. It's not a scam, it's not just happening to you. It's happening to everyone. All HYSAs (high yield savings accounts) are raising their interest rates right now. This means your money is making MORE money by sitting in that savings account.

THIS IS A SIGN OF BAD THINGS FOR THE WIDER ECONOMY. Remember our advice on how to protect your money from inflation? Here, in case you missed it:

How To Protect Cash Savings During High Inflation

The tl;dr is we were like "you could put it in a HYSA but interest rates are so low right now that that's not super effective." That was before inflation skyrocketed to its current levels.

See, when shit's going well in the economy, HYSA interest rates are low. They know things are stable. You have all the money in the world to spend on goods and services! They ain't trying to compete with the stock market, where they know you'll get much higher rates of return.

But right now, inflation is making all those goods and services more expensive. And the stock market has been doing its best impression of the Hindenberg. Plus, interest rates for loans are going up as the Fed (Federal Reserve, which is the governmental organization that controls how our money works) keeps raising them to try to slow inflation (I will NOT explain that logic here because I don't have nineteen hours). So things like mortgages just got wicked expensive.

All of this leads to HYSAs knowing that they are now our best bet for earning money on our money. So along with some external factors, this has caused them to raise their rates.

Again--great time to open a HYSA! Keep celebrating those increasing interest rates! But it's all happening because the economy's in the shitter. Hope that helps, baby!

From HYSAs to CDs, Here's How to Level Up Your Financial Savings

83 notes

·

View notes

Text

LETTERS FROM AN AMERICAN

May 15, 2024

HEATHER COX RICHARDSON

MAY 16, 2024

All three of the nation’s major stock indexes hit record highs today after the latest data showed inflation cooling. Standard and Poor’s 500, more commonly known as the S&P 500, measures the stock performance of 500 of the largest companies listed on U.S. stock exchanges. Today it was up 61 points, or 1.2%. The Nasdaq Composite is weighted toward companies in the information technology sector. Today it was up 231 points, or 1.4%. The Dow Jones Industrial Average, often just called the Dow, measures 30 prominent companies listed on U.S. stock exchanges. Today it was up 350 points, or 0.9%. The Dow has risen now for eight straight days, ending the day at 39,908, approaching 40,000.

Driving the hike in the stock market, most likely, is the information released today by the Bureau of Labor Statistics in the Labor Department saying that inflation eased in April. Investors are guessing this makes it more likely that the Federal Reserve will cut interest rates this year.

People note—correctly—that the stock market does not reflect the larger economy. This makes a report released yesterday from the nonpartisan Congressional Budget Office, or CBO, an important addition to the news from the stock market. It concludes that the goods and services an American household consumed in 2019 were cheaper in 2023 than they were four years before, because incomes grew faster than prices over that four-year period. That finding was true for all levels of the economy.

That is, “for all income groups…the portion of household income required to purchase the same bundle of goods and services declined.” Those in the bottom 20% found that the share of their income required to purchase the same bundle dropped by 2%. For those in the top 20%, the share of their income required to purchase as they did in 2019 dropped by 6.3%.