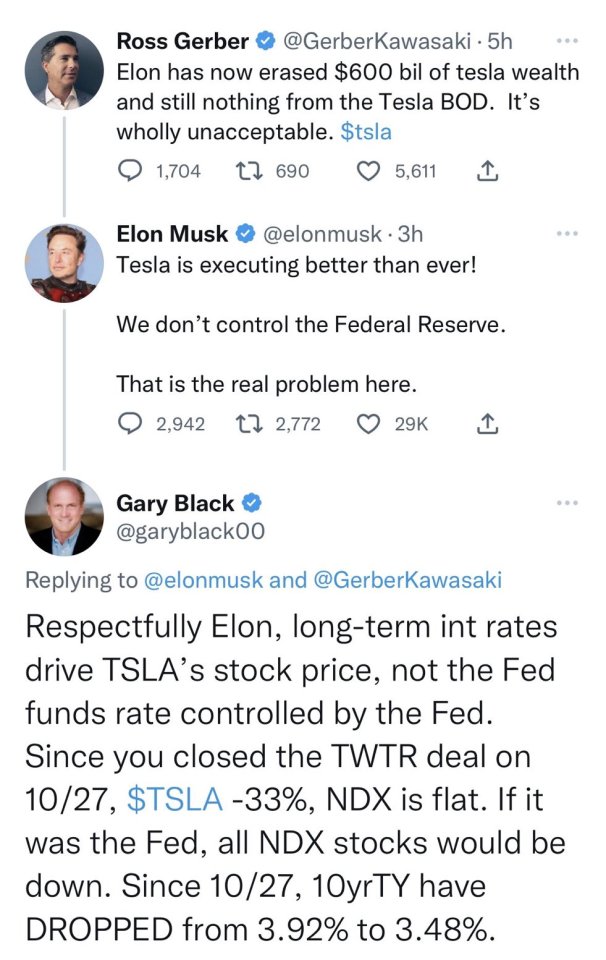

#Federal Reserve

Text

An alternate angle on the Francis Scott Key Bridge shows what appears to be a large explosion, which you can see 👀 from the other angles I posted. Something reeks like a possible Black Swan Event?

Does it seem like a barge bumping into a pillar would cause the whole bridge to collapse? 🤔

#pay attention#educate yourselves#educate yourself#knowledge is power#reeducate yourself#reeducate yourselves#think about it#think for yourselves#think for yourself#do your homework#do some research#do your own research#federal reserve#question everything#francis scott key bridge#bridge collapse#baltimore maryland#you decide#we are the news#black swan event#government corruption

964 notes

·

View notes

Text

There are no coincidences.

913 notes

·

View notes

Text

Fortress of Finance

The Federal Reserve Bank of San Francisco, California

Bob Cronk

#federal reserve#the federal reserve bank of San Francisco#San Francisco#california#urban photography#interest rates#urban explorers#bob cronk#bob cronk photography#tightening#economy#original photographers#original photography#photographers on tumblr#photography on tumblr#urban exploring photography#urban exploration

135 notes

·

View notes

Text

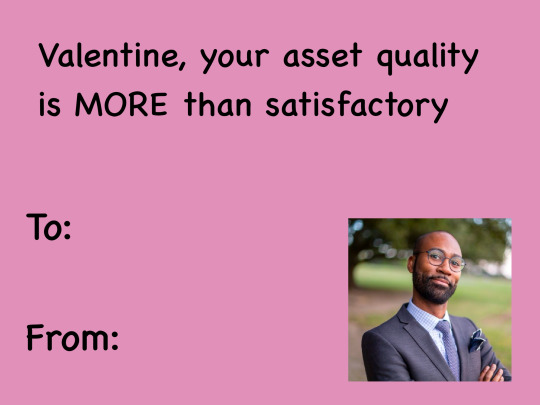

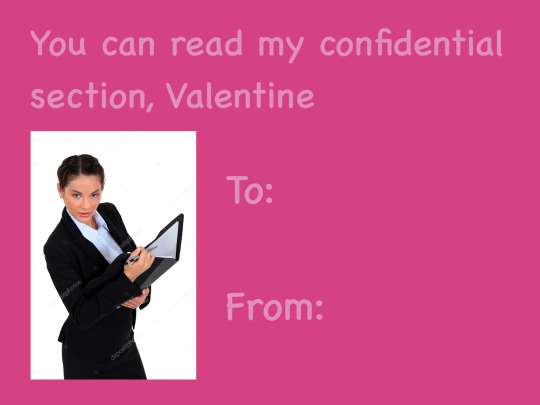

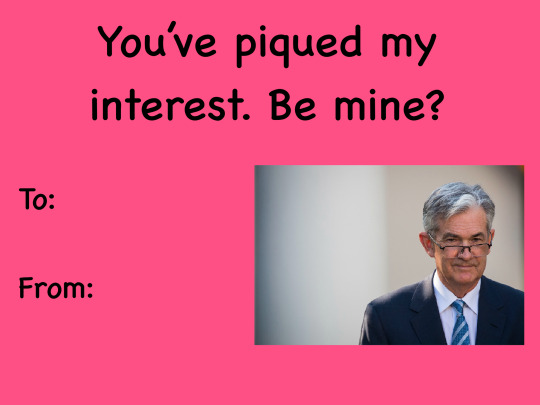

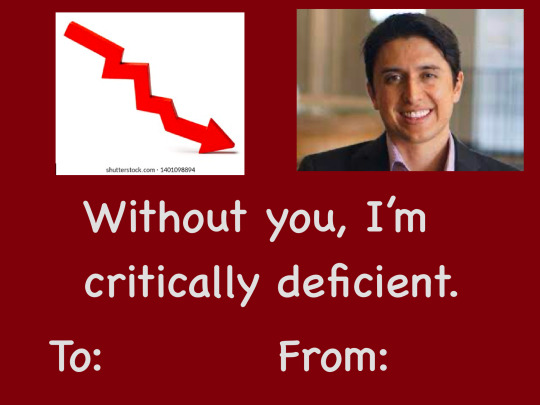

I made some Valentine’s Day cards for you all to share with your favorite bank examiners and/or economists! With a little help from my friend @tricksypixie of course ☺️

#valentines memes#valentines day#valentines cards#jay speaks#federal reserve#the fed#interest rates#economics

54 notes

·

View notes

Text

699 notes

·

View notes

Text

32 notes

·

View notes

Text

Gold hoarders laden with bags, boxes, and suitcases enter and leave the Federal Reserve Bank to deposit their hidden currency, March 10, 1933. In one day, they deposited $30 million (worth around $700 million today), hoping to escape the penalties that the government would exact on hoarders effective May 1. The U.S. was still on the gold standard at the time, and President Roosevelt felt that hoarding the stuff prevented it from increasing the money supply.

Photo: Associated Press

#vintage New York#1930s#gold hoarding#Great Depression#New Deal#1930s economy#gold standard#money supply#Federal Reserve#Executive Order#March 10#10 March

21 notes

·

View notes

Text

Classicum Aureum Elementium.

The oldest gold artifacts in the world are from Bulgaria dating back to the 5ᵗʰ millennium BC

Gold artifacts probably made their first appearance in Ancient Egypt at beginning of the pre-dynastic period, at the end of the 5ᵗʰ millennium BC & the start of the 4ᵗʰ.

In the past, a gold standard was often implemented as a monetary policy. Gold coins ceased to be minted as a circulating currency in the 1930s, and the world gold standard was abandoned for a fiat currency system after the Nixon shock measures of 1971.

#gold#classic#element#atom#loop#trapcode#tao#after effects#shiny#motion#animation#gif art#egypt#bulgaria#artifacts#standard#federal reserve

91 notes

·

View notes

Text

Do You Know What is Real? 🤔

More examples of CGI Deep Fake Technology

#pay attention#educate yourself#educate yourselves#knowledge is power#reeducate yourself#reeducate yourselves#think for yourself#think for yourselves#think about it#do your homework#do some research#do your research#federal reserve#question everything#ask yourself questions

194 notes

·

View notes

Text

Why the Fed wants to crush workers

The US Federal Reserve has two imperatives: keeping employment high and inflation low. But when these come into conflict — when unemployment falls to near-zero — the Fed forgets all about full employment and cranks up interest rates to “cool the economy” (that is, “to destroy jobs and increase unemployment”).

An economy “cools down” when workers have less money, which means that the prices offered for goods and services go down, as fewer workers have less money to spend. As with every macroeconomic policy, raising interest rates has “distributional effects,” which is economist-speak for “winners and losers.”

Predicting who wins and who loses when interest rates go up requires that we understand the economic relations between different kinds of rich people, as well as relations between rich people and working people. Writing today for The American Prospect’s superb Great Inflation Myths series, Gerald Epstein and Aaron Medlin break it down:

https://prospect.org/economy/2023-01-19-inflation-federal-reserve-protects-one-percent/

Recall that the Fed has two priorities: full employment and low interest rates. But when it weighs these priorities, it does so through “finance colored” glasses: as an institution, the Fed requires help from banks to carry out its policies, while Fed employees rely on those banks for cushy, high-paid jobs when they rotate out of public service.

Inflation is bad for banks, whose fortunes rise and fall based on the value of the interest payments they collect from debtors. When the value of the dollar declines, lenders lose and borrowers win. Think of it this way: say you borrow $10,000 to buy a car, at a moment when $10k is two months’ wages for the average US worker. Then inflation hits: prices go up, workers demand higher pay to keep pace, and a couple years later, $10k is one month’s wages.

If your wages kept pace with inflation, you’re now getting twice as many dollars as you were when you took out the loan. Don’t get too excited: these dollars buy the same quantity of goods as your pre-inflation salary. However, the share of your income that’s eaten by that monthly car-loan payment has been cut in half. You just got a real-terms 50% discount on your car loan!

Inflation is great news for borrowers, bad news for lenders, and any given financial institution is more likely to be a lender than a borrower. The finance sector is the creditor sector, and the Fed is institutionally and personally loyal to the finance sector. When creditors and debtors have opposing interests, the Fed helps creditors win.

The US is a debtor nation. Not the national debt — federal debt and deficits are just scorekeeping. The US government spends money into existence and taxes it out of existence, every single day. If the USG has a deficit, that means it spent more than than it taxed, which is another way of saying that it left more dollars in the economy this year than it took out of it. If the US runs a “balanced budget,” then every dollar that was created this year was matched by another dollar that was annihilated. If the US runs a “surplus,” then there are fewer dollars left for us to use than there were at the start of the year.

The US debt that matters isn’t the federal debt, it’s the private sector’s debt. Your debt and mine. We are a debtor nation. Half of Americans have less than $400 in the bank.

https://www.fool.com/the-ascent/personal-finance/articles/49-of-americans-couldnt-cover-a-400-emergency-expense-today-up-from-32-in-november/

Most Americans have little to no retirement savings. Decades of wage stagnation has left Americans with less buying power, and the economy has been running on consumer debt for a generation. Meanwhile, working Americans have been burdened with forms of inflation the Fed doesn’t give a shit about, like skyrocketing costs for housing and higher education.

When politicians jawbone about “inflation,” they’re talking about the inflation that matters to creditors. Debtors — the bottom 90% — have been burdened with three decades’ worth of steadily mounting inflation that no one talks about. Yesterday, the Prospect ran Nancy Folbre’s outstanding piece on “care inflation” — the skyrocketing costs of day-care, nursing homes, eldercare, etc:

https://prospect.org/economy/2023-01-18-inflation-unfair-costs-of-care/

As Folbre wrote, these costs are doubly burdensome, because they fall on family members (almost entirely women), who have to sacrifice their own earning potential to care for children, or aging people, or disabled family members. The cost of care has increased every year since 1997:

https://pluralistic.net/2023/01/18/wages-for-housework/#low-wage-workers-vs-poor-consumers

So while politicians and economists talk about rescuing “savers” from having their nest-eggs whittled away by inflation, these savers represent a minuscule and dwindling proportion of the public. The real beneficiaries of interest rate hikes isn’t savers, it’s lenders.

Full employment is bad for the wealthy. When everyone has a job, wages go up, because bosses can’t threaten workers with “exile to the reserve army of the unemployed.” If workers are afraid of ending up jobless and homeless, then executives seeking to increase their own firms’ profits can shift money from workers to shareholders without their workers quitting (and if the workers do quit, there are plenty more desperate for their jobs).

What’s more, those same executives own huge portfolios of “financialized” assets — that is, they own claims on the interest payments that borrowers in the economy pay to creditors.

The purpose of raising interest rates is to “cool the economy,” a euphemism for increasing unemployment and reducing wages. Fighting inflation helps creditors and hurts debtors. The same people who benefit from increased unemployment also benefit from low inflation.

Thus: “the current Fed policy of rapidly raising interest rates to fight inflation by throwing people out of work serves as a wealth protection device for the top one percent.”

Now, it’s also true that high interest rates tend to tank the stock market, and rich people also own a lot of stock. This is where it’s important to draw distinctions within the capital class: the merely rich do things for a living (and thus care about companies’ productive capacity), while the super-rich own things for a living, and care about debt service.

Epstein and Medlin are economists at UMass Amherst, and they built a model that looks at the distributional outcomes (that is, the winners and losers) from interest rate hikes, using data from 40 years’ worth of Fed rate hikes:

https://peri.umass.edu/images/Medlin_Epstein_PERI_inflation_conf_WP.pdf

They concluded that “The net impact of the Fed’s restrictive monetary policy on the wealth of the top one percent depends on the timing and balance of [lower inflation and higher interest]. It turns out that in recent decades the outcome has, on balance, worked out quite well for the wealthy.”

How well? “Without intervention by the Fed, a 6 percent acceleration of inflation would erode their wealth by around 30 percent in real terms after three years…when the Fed intervenes with an aggressive tightening, the 1%’s wealth only declines about 16 percent after three years. That is a 14 percent net gain in real terms.”

This is why you see a split between the one-percenters and the ten-percenters in whether the Fed should continue to jack interest rates up. For the 1%, inflation hikes produce massive, long term gains. For the 10%, those gains are smaller and take longer to materialize.

Meanwhile, when there is mass unemployment, both groups benefit from lower wages and are happy to keep interest rates at zero, a rate that (in the absence of a wealth tax) creates massive asset bubbles that drive up the value of houses, stocks and other things that rich people own lots more of than everyone else.

This explains a lot about the current enthusiasm for high interest rates, despite high interest rates’ ability to cause inflation, as Joseph Stiglitz and Ira Regmi wrote in their recent Roosevelt Institute paper:

https://rooseveltinstitute.org/wp-content/uploads/2022/12/RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

The two esteemed economists compared interest rate hikes to medieval bloodletting, where “doctors” did “more of the same when their therapy failed until the patient either had a miraculous recovery (for which the bloodletters took credit) or died (which was more likely).”

As they document, workers today aren’t recreating the dread “wage-price spiral” of the 1970s: despite low levels of unemployment, workers wages still aren’t keeping up with inflation. Inflation itself is falling, for the fairly obvious reason that covid supply-chain shocks are dwindling and substitutes for Russian gas are coming online.

Economic activity is “largely below trend,” and with healthy levels of sales in “non-traded goods” (imports), meaning that the stuff that American workers are consuming isn’t coming out of America’s pool of resources or manufactured goods, and that spending is leaving the US economy, rather than contributing to an American firm’s buying power.

Despite this, the Fed has a substantial cheering section for continued interest rates, composed of the ultra-rich and their lickspittle Renfields. While the specifics are quite modern, the underlying dynamic is as old as civilization itself.

Historian Michael Hudson specializes in the role that debt and credit played in different societies. As he’s written, ancient civilizations long ago discovered that without periodic debt cancellation, an ever larger share of a societies’ productive capacity gets diverted to the whims of a small elite of lenders, until civilization itself collapses:

https://www.nakedcapitalism.com/2022/07/michael-hudson-from-junk-economics-to-a-false-view-of-history-where-western-civilization-took-a-wrong-turn.html

Here’s how that dynamic goes: to produce things, you need inputs. Farmers need seed, fertilizer, and farm-hands to produce crops. Crucially, you need to acquire these inputs before the crops come in — which means you need to be able to buy inputs before you sell the crops. You have to borrow.

In good years, this works out fine. You borrow money, buy your inputs, produce and sell your goods, and repay the debt. But even the best-prepared producer can get a bad beat: floods, droughts, blights, pandemics…Play the game long enough and eventually you’ll find yourself unable to repay the debt.

In the next round, you go into things owing more money than you can cover, even if you have a bumper crop. You sell your crop, pay as much of the debt as you can, and go into the next season having to borrow more on top of the overhang from the last crisis. This continues over time, until you get another crisis, which you have no reserves to cover because they’ve all been eaten up paying off the last crisis. You go further into debt.

Over the long run, this dynamic produces a society of creditors whose wealth increases every year, who can make coercive claims on the productive labor of everyone else, who not only owes them money, but will owe even more as a result of doing the work that is demanded of them.

Successful ancient civilizations fought this with Jubilee: periodic festivals of debt-forgiveness, which were announced when new monarchs assumed their thrones, or after successful wars, or just whenever the creditor class was getting too powerful and threatened the crown.

Of course, creditors hated this and fought it bitterly, just as our modern one-percenters do. When rulers managed to hold them at bay, their nations prospered. But when creditors captured the state and abolished Jubilee, as happened in ancient Rome, the state collapsed:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Are we speedrunning the collapse of Rome? It’s not for me to say, but I strongly recommend reading Margaret Coker’s in-depth Propublica investigation on how title lenders (loansharks that hit desperate, low-income borrowers with triple-digit interest loans) fired any employee who explained to a borrower that they needed to make more than the minimum payment, or they’d never pay off their debts:

https://www.propublica.org/article/inside-sales-practices-of-biggest-title-lender-in-us

[Image ID: A vintage postcard illustration of the Federal Reserve building in Washington, DC. The building is spattered with blood. In the foreground is a medieval woodcut of a physician bleeding a woman into a bowl while another woman holds a bowl to catch the blood. The physician's head has been replaced with that of Federal Reserve Chairman Jerome Powell.]

#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters

464 notes

·

View notes

Text

youtube

The Biden administration announced a rule Tuesday to cap all credit card late fees, the latest effort in the White House push to end what it has called junk fees and a move that regulators say will save Americans up to $10 billion a year.

The Consumer Financial Protection Bureau’s new regulations will set a ceiling of $8 for most credit card late fees or require banks to show why they should charge more than $8 for such a fee.

The rule would bring the average credit card late fee down from $32. The bureau estimates banks brought in roughly $14 billion in credit card late fees a year.

“In credit cards, like so many corners of the economy today, consumers are beset by junk fees and forced to navigate a market dominated by relatively few, powerful players who control the market,” said Rohit Chopra, director of the bureau, in a statement.

President Joe Biden planned to highlight the proposal along with other efforts to reduce costs to Americans at a meeting of his competition council on Tuesday. The Democratic president is forming a new strike force to crack down on illegal and unfair pricing on things like groceries, prescription drugs, health care, housing and financial services.

The strike force will be led by the Justice Department and the Federal Trade Commission, according to a White House statement.

The Biden administration has portrayed the White House Competition Council as a way to save people money and promote greater competition within the U.S. economy.

The White House Council of Economic Advisers produced an analysis indicating that the Biden administration’s efforts overall will eliminate $20 billion in annual junk fees. The analysis found that consumers pay about $90 billion a year in junk fees, including for concerts, apartment rentals and auto dealers.

The effort appears to have done little to help Biden politically ahead of this year’s presidential election. Just 34 percent of U.S. adults approve of Biden’s economic leadership, according to a new survey by The Associated Press-NORC Center for Public Affairs Research.

Sen. Tim Scott, R-South Carolina, criticized the CFPB cap on credit card late fees, saying that consumers would ultimately face greater costs through higher interest rates and less access to credit.

“It will decrease the availability of credit card products for those who need it most, raise rates for many borrowers who carry a balance but pay on time, and increase the likelihood of late payments across the board,” Scott said.

Americans held more than $1.05 trillion on their credit cards in the third quarter of 2023, a record, and a figure certain to grow once the fourth-quarter data is released by the Federal Deposit Insurance Corp. next month. Those balances are now carrying interest on them, which is the highest it has been since the Federal Reserve started tracking the data back in the mid-1990s.

Further, more Americans are falling behind on their credit card debts as well. Delinquency rates at the major credit card issuers such as American Express, JPMorgan Chase, Citigroup, Capital One and Discover have been trending upward for several quarters. Some analysts have become concerned Americans, particularly poorer households hurt by inflation, might be taking on too much debt.

“Overall, the consumer is credit healthy. However, the reality is that there are starting to be some significant signs of stress,” said Silvio Tavares, president and CEO of VantageScore, one of the country’s two major credit scoring systems, in an interview last month.

The growth of the credit card industry is partly why Capital One announced it would buy Discover Financial last month for $35 billion. The two companies, which are two of the largest credit card issuers, are also two companies whose customers regularly carry a balance on their accounts.

This is not the first time policymakers have weighed in on credit card fees. Congress in 2010 passed the CARD Act, which banned credit card companies from charging excessive penalty fees and established clearer disclosures and consumer protections.

The Federal Reserve issued a rule in 2010 that capped the first credit card late fee at $25, and $35 for subsequent late payments, and tied that fee to inflation. The CFPB, which took over the regulation of the credit card industry from the Fed after it was established, is proposing going further than the Fed.

The bureau’s proposal is similar in structure to what the bureau announced in January when it proposed capping overdraft fees to as little as $3. In that proposed regulation, banks would be required to either accept the bureau’s benchmark or show regulators why they should charge more, a method that few bank industry executives expect to use.

Biden has made the elimination of junk fees one of the cornerstones of his administration’s economic agenda heading into the 2024 election. Fees that banks charge customers have been at the center of that campaign, and the White House directed government regulators last year to do whatever is in their power to further curtail the practice.

In another move being highlighted by the White House, the Agriculture Department said it has finalized a rule to stop what it deems to be deceptive contracts by meat processors and to ban retaliation against small farmers and ranchers that work together in associations.

#us politics#news#pbs#president joe biden#2024#Consumer Financial Protection Bureau#credit cards#late fees#junk fees#Rohit Chopra#Federal Trade Commission#department of justice#White House Competition Council#White House Council of Economic Advisers#Sen. Tim Scott#Federal Deposit Insurance Corp#federal reserve#youtube#videos#economy#economics

13 notes

·

View notes

Text

I will take poll results into account next week. I’m sure the FOMC will be very grateful to hear your responses, valued citizens of the Tumblr ^.^

#federal open market committee#federal reserve#the fed#interest rates#jerome powell#polls#finance#finance polls#jay speaks

149 notes

·

View notes

Text

🚨🚨Jacob Rothschild gets confronted by patriots 🔥 :

“The Federal Reserve is a source of inhumane products all around the world, because it’s a PRIVATE BANK that was started by your family!! Do you have any comment?”

“We can go on about all the stuff your family has done to society, but we just want you to know that the #NewWorldOrder does NOT have any legitimacy!!!”

“#WeThePeople are not AFRAID and we are waking up to the ROBBER barons and the BIG BANKS who are LOOTING this economy with the #FederalReserve”

LET’S GO!!!!!!!!!🔥🔥🔥

Rothschild #EndTheFed

the video is great!

16 notes

·

View notes

Text

Federal Reserve stuck between a rock and a hard place

#Federal Reserve#US Federal Reserve#Interest rate#High inflation#Biden inflation#Bidenflation#Banking crisis#Biden economy#Here comes the recession#2023 crash#Daily struggle

42 notes

·

View notes

Last Seen Blogs

9ineine

the ultimate simp

jestain

girdle, interrupted

spicygingerhoney

🌶️🍯

tokidokitokyo

Tokidoki Tokyo

swiftiessid

TSDelRey_13