#electro optical eo

Text

The A-29B Super Tucano Aircraft of the Philippine Air Force (PAF) seems to be operating on a Buddy System, sharing one Electro-Optical/Forward Looking Infra-Red (EO/FLIR) “Ball” for every two Aircraft while the Armed Forces of the Philippines (AFP) used their newest Assets like the Super Tucanos, Autonomous Truck Mounted-howitzer System (ATMOS) and Hermes Drones to make a devastating strike against the New People's Army (NPA) even under the cover of Darkness

#a29b super tucano#philippine air force paf#electro optical eo#forward looking infra red flir#armed forces of the philippines afp#autonomous truck mounted howitzer system atmos#hermes 450#hermes 900#edwin andrews air base#zamboanga city#western mindanao command wescom#buddy system#new peoples army npa#malaybalay#bukidnon#philippine army pa#3rd howitzer platoon#alpha battery#4th field artillery battalion#strike from afar#8th infantry battalion#1st special forces battalion#88th infantry battalion

0 notes

Text

A combination of systems that can detect electromagnetic and radio frequency RF emissions generated by communication between the drone and its remote controller, as well as EO systems to detect IR and UV emissions is needed

#electro optics systems#electro optical systems#electro optical modulator#electro optics#eo systems#electro optic systems

0 notes

Text

New image shows how the B-52 will look after engine and radar replacement

Fernando Valduga By Fernando Valduga 10/19/22 - 21:29 in Military

A new image of Boeing shows how the B-52H will look after a series of modifications that the U.S. Air Force said were significant enough to justify the renaming of the aircraft as B-52J or K.

The image was rendered from a digital prototyping model system, so it is likely to be very close to the final version.

The image highlights the largest diameter F130 turbofan engines to be built by Rolls-Royce North America. Also noteworthy is how the engine springs, each containing two engines, are placed higher and further ahead than the Pratt & Whitney TF-33 engines with which the B-52 has been flying since 1962, in part to provide more distance from the ground. The need to validate how the new engines/aveles will behave in relation to the wing and flaps system is an important part of the flight test program scheduled to start in the next two years.

The nose of the aircraft will also be simplified, losing the bubbles that currently house the infrared/electro-optical viewing system to facilitate the new radar, a variant of the AN/APG-79 used in the Boeing F/A-18E/F SuperHornet. The FLIR/EO system was used to avoid terrain and battle evaluation, but some of these functions will migrate to the radar or have already changed to a Litening or Sniper aiming pod, which the B-52 can carry on a hanger on the wing.

In addition to the engines and radar, the B-52 is receiving an updated cockpit, a "hybrid" analog-digital motor control system, communication and navigation improvements and the exclusion of a crew station.

Two large ravens at the top of the fuselage, close to the roots of the wings, also stand out in the images. A Boeing spokesman said that the crows “are not new and are not part of our program”, but they look bigger than any fairings or bubbles now in that area, which house GPS and other communication/navigation equipment. Pressed, the Boeing spokesman said: "I have nothing for you about it", a phrase that sometimes indicates a confidential issue. The location and size of the corcovas may suggest a larger and anti-incrat GPS antenna.

New engines were the main reason why the B-52G became the B-52H in 1962, said in August to Colonel Louise Ruscetta, senior material leader of the B-52. But given that the combined engine/radar program represents “the biggest modification in history” of the B-52, a new designation is likely, Ruscetta said. There may be a provisional designation because the radar will be installed before the engines and will lead to a change in manuals and operating and maintenance documentation. The documents will be changed again as soon as the engines are replaced. The Air Force and the Air Force Global Attack Command are analyzing "how we define" the new variant or variants, Ruscetta said.

The new radar is a type of active electronic scanning matrix, used by fighters. It will take up much less space than the old mechanically scanned system, so the change will create space for electronic warfare functions, Ruscetta said. At least part of the B-52 fleet will be operational with new radars and new engines by the end of the decade.

Source: Air Force & Space Magazine

Tags: Military AviationBoeing B-52H StratofortressUSAF - United States Air Force / US Air Force

Previous news

Falcon 6X enters the final phase of flight tests

Fernando Valduga

Fernando Valduga

Aviation photographer and pilot since 1992, he has participated in several events and air operations, such as Cruzex, AirVenture, Dayton Airshow and FIDAE. It has works published in specialized aviation magazines in Brazil and abroad. Uses Canon equipment during his photographic work in the world of aviation.

Related news

Russian Su-57 fighter. (Photo: Global Look Press)

MILITARY

Su-57 fighter stood out in attacks in Ukraine, says Russian commander

19/10/2022 - 19:00

MILITARY

U.S. Navy stops T-45C flights due to engine blade failures

19/10/2022 - 16:00

MILITARY

Myanmar would have purchased FTC-2000G jets from China

19/10/2022 - 14:00

EMBRAER

VIDEO: Portugal presents the Air Force's first KC-390 aircraft

19/10/2022 - 12:00

A future JASDF E-2D Advanced Hawkeye is unloaded at the port of the Iwakuni Marine Corps Air Station, Japan, on October 18, 2022. (Photo: U.S. Marine Corps)

MILITARY

New E-2D arrives in Japan for the Japanese Air Self-Defense Force

19/10/2022 - 08:17

MILITARY

SALITRE: Air Force aircraft from Brazil, Chile and Argentina participate in exhibition

19/10/2022 - 08:07

home Main Page Editorials INFORMATION events Cooperate Specialities advertise about

Cavok Brazil - Digital Tchê Web Creation

Commercial

Executive

Helicopters

HISTORY

Military

Brazilian Air Force

Space

Specialities

Cavok Brazil - Digital Tchê Web Creation

40 notes

·

View notes

Text

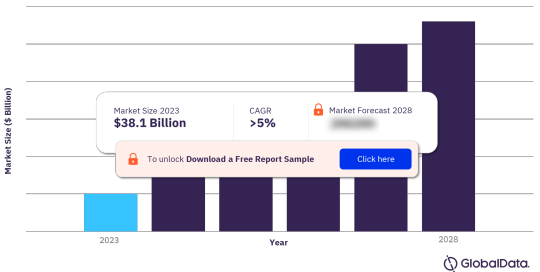

Shaping Tomorrow's Healthcare: Exploring the Growth Trajectory of 4D Printing

The 4D Printing in Healthcare Market represents a cutting-edge intersection of additive manufacturing technology and healthcare innovation, offering transformative solutions for patient care, personalized medicine, and medical device development. In this analysis, we explore the key drivers, trends, challenges, and opportunities shaping the 4D Printing in Healthcare Market.

𝐆𝐞𝐭 𝐟𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞:

https://www.marketdigits.com/request/sample/3917

One of the primary drivers of the 4D Printing in Healthcare Market is the increasing demand for patient-specific medical devices and implants. Traditional manufacturing techniques often struggle to produce complex, customized medical devices tailored to individual patient anatomy. 4D printing, an advanced form of additive manufacturing, enables the fabrication of dynamic, shape-changing structures with predetermined responses to external stimuli, such as temperature, humidity, or light. This capability allows for the creation of personalized implants, prosthetics, and orthotics that conform to patients' unique anatomical requirements and provide superior fit, comfort, and functionality.

The 4D Printing in Healthcare Market is valued at USD 9.5 million in 2024 and projected to reach USD 47.5 million by 2030, showing a Compound Annual Growth Rate (CAGR) of 22.3% during the forecast period from 2024 to 2032.

Moreover, 4D printing offers significant advantages over traditional manufacturing methods in terms of design flexibility, material selection, and manufacturing efficiency. With 4D printing, designers can create intricate, multi-material structures with precise control over geometry, porosity, and mechanical properties. This versatility enables the development of biocompatible scaffolds, drug delivery systems, and tissue-engineered constructs for regenerative medicine and tissue engineering applications. By integrating bioactive materials and cell-laden hydrogels into 4D-printed constructs, researchers can mimic native tissue architectures and promote tissue regeneration for wound healing, organ repair, and transplantation.

Major vendors in the global 4D printing in healthcare Market are 3D Systems, Organovo Holdings Inc., Stratasys Ltd., Dassault Systèmes, Materialise, EOS GmbH Electro Optical Systems, EnvisionTEC, and Poietis and others

Furthermore, the convergence of 4D printing with advanced imaging technologies, such as computed tomography (CT) and magnetic resonance imaging (MRI), facilitates the creation of patient-specific anatomical models and surgical guides for preoperative planning and intraoperative navigation. Surgeons can use 4D-printed models to visualize complex anatomical structures, simulate surgical procedures, and practice intricate maneuvers before entering the operating room. This enhanced visualization and surgical simulation improve surgical precision, reduce operative time, and minimize complications, ultimately leading to better patient outcomes and healthcare cost savings.

In addition to its applications in medical device manufacturing and surgical planning, 4D printing holds promise for drug delivery and personalized medicine. By incorporating stimuli-responsive polymers and controlled-release mechanisms into 4D-printed drug delivery systems, researchers can achieve targeted, on-demand drug release profiles tailored to individual patient needs. This precision drug delivery approach enables the administration of therapeutics at specific sites of action, optimized dosing regimens, and improved patient compliance. Furthermore, 4D-printed drug-eluting implants and microneedle arrays offer innovative solutions for localized drug delivery, chronic disease management, and regenerative therapies.

However, the 4D Printing in Healthcare Market also faces challenges and barriers to widespread adoption, including material biocompatibility, regulatory approval, and scalability of manufacturing processes. Ensuring the safety, efficacy, and biocompatibility of 4D-printed medical devices and implants requires rigorous testing, validation, and regulatory oversight to meet quality standards and regulatory requirements. Moreover, scaling up 4D printing technologies for mass production while maintaining cost-effectiveness and manufacturing consistency remains a challenge for commercialization and market penetration.

In conclusion, the 4D Printing in Healthcare Market holds immense promise for revolutionizing patient care, personalized medicine, and medical device development. By harnessing the unique capabilities of 4D printing technology, healthcare professionals can create customized solutions that improve treatment outcomes, enhance patient experiences, and advance the practice of precision medicine. While challenges remain, ongoing research, collaboration, and innovation in the field are driving progress and expanding the clinical applications of 4D printing in healthcare.

0 notes

Text

Navigating the Competitive Landscape of the Drone Countermeasures Market

Introduction

In recent years, the proliferation of drones has presented both opportunities and challenges across various industries. While drones offer numerous benefits such as aerial surveillance, package delivery, and agricultural monitoring, they also pose significant security risks, prompting the rapid growth of the drone countermeasures market.

According to the study by Next Move Strategy Consulting, the global Drone Countermeasures Market size is predicted to reach USD 6.99 billion with a CAGR of 18.5% by 2030.

Get a FREE Sample: https://www.nextmsc.com/drone-countermeasures-market/request-sample

Understanding the Drone Countermeasures Market

The drone countermeasures market encompasses a wide range of technologies and solutions designed to detect, track, and neutralize rogue drones. This includes detection systems utilizing radar, radio frequency (RF) sensors, electro-optical/infrared (EO/IR) cameras, acoustic sensors, and advanced artificial intelligence (AI) algorithms to identify and classify drones in real time.

In addition to detection technologies, the market also includes countermeasure solutions such as jamming, spoofing, netting, and even deploying trained birds of prey to intercept and neutralize hostile drones. These innovative solutions aim to provide comprehensive protection against unauthorized drone activities while minimizing collateral damage and disruption to legitimate drone operations.

Drivers of Growth

One of the key drivers fueling the growth of the drone countermeasures market is the increasing incidents of unauthorized drone activities. From trespassing and smuggling to espionage and malicious attacks, drones are being used for a variety of nefarious purposes, posing significant security threats to governments, critical infrastructure operators, defense agencies, and private enterprises.

In response to these growing threats, there is a heightened demand for effective drone countermeasures solutions that can detect and neutralize rogue drones in real time. This has led to the rapid development and adoption of advanced technologies and innovative approaches to address evolving security challenges.

Competitive Landscape

The competitive landscape of the drone countermeasures market is dynamic and evolving, driven by technological advancements, regulatory developments, and shifting security threats. Companies operating in this space are continuously innovating to stay ahead of emerging challenges and capitalize on lucrative opportunities.

Competition in the drone countermeasures market is fierce, with a multitude of companies vying for market share by offering a diverse range of products and services. These include established players with decades of experience in defense and security, as well as startups and technology firms specializing in drone detection and mitigation solutions.

Technological Innovation

Technological innovation is a key differentiator in the drone countermeasures market, with companies investing heavily in research and development to stay ahead of the competition. Advancements in sensor technology, AI algorithms, and signal processing techniques are enabling more accurate and reliable detection of rogue drones, while innovative countermeasure solutions are becoming increasingly sophisticated and effective.

For example, some companies are developing drone detection systems that can differentiate between different types of drones based on their size, shape, and flight characteristics. This enables security personnel to assess the level of threat posed by a rogue drone and take appropriate action to neutralize it.

Similarly, advancements in countermeasure technologies such as jamming and spoofing are making it more difficult for rogue drones to evade detection and carry out malicious activities. By disrupting communication signals or feeding false GPS coordinates to the drone, these countermeasures can effectively neutralize the threat posed by unauthorized drone operations.

Regulatory Compliance

Regulatory compliance is another important factor shaping the competitive landscape of the drone countermeasures market. As governments worldwide implement stricter regulations governing the operation of drones, companies must ensure that their products and services adhere to relevant legal requirements and certifications.

For example, many countries have implemented no-fly zones and flight restrictions around sensitive locations such as airports, military bases, and government buildings to prevent unauthorized drone activities. Companies developing drone countermeasures solutions must ensure that their products are capable of detecting and neutralizing rogue drones within these restricted areas while complying with applicable regulations and safety standards.

Strategic Partnerships and Collaborations

Strategic partnerships, collaborations, and mergers and acquisitions (M&A) play a crucial role in shaping the competitive landscape of the drone countermeasures market. By leveraging complementary strengths and capabilities, companies can enhance their market position, expand their product portfolios, and capitalize on synergies to better serve their customers.

For example, a drone detection technology company may partner with a defense contractor to integrate its sensors into existing security systems and infrastructure. Similarly, a company specializing in countermeasure solutions may collaborate with law enforcement agencies and security providers to deploy its products in high-risk environments and critical infrastructure facilities.

Inquire before buying, here: https://www.nextmsc.com/drone-countermeasures-market/inquire-before-buying

Challenges and Opportunities

However, navigating the competitive landscape of the drone countermeasures market is not without its challenges. Rapid technological advancements, evolving threat landscapes, and regulatory uncertainties require companies to remain agile, adaptable, and vigilant to stay ahead of the curve.

One of the biggest challenges facing companies in the drone countermeasures market is the cat-and-mouse game between security professionals and malicious actors. As security measures become more sophisticated, so too do the tactics employed by those seeking to evade detection and neutralization. This requires companies to continuously innovate and develop new strategies and technologies to stay one step ahead of emerging threats.

At the same time, the growing demand for drone countermeasures solutions presents significant opportunities for companies willing to invest in research and development and expand their market presence. As drones become more ubiquitous and their capabilities continue to evolve, the need for effective countermeasures will only increase, creating a ripe market for innovative solutions that can address emerging security challenges.

Resource Allocation: Developing and deploying effective drone countermeasures solutions requires substantial financial resources, technical expertise, and infrastructure. Companies must carefully allocate resources to research and development, testing, marketing, and sales to ensure the successful development and commercialization of their products.

Ethical and Legal Considerations: The use of countermeasure technologies such as jamming and spoofing raises ethical and legal questions regarding privacy, safety, and interference with lawful drone operations. Companies must navigate complex legal and regulatory frameworks governing the use of such technologies while upholding ethical standards and societal expectations.

Interoperability and Compatibility: With the proliferation of drone countermeasures solutions from various vendors, ensuring interoperability and compatibility between different systems and platforms is essential for seamless integration and effectiveness. Companies must collaborate with industry partners and standardization bodies to develop interoperable solutions that can communicate and collaborate effectively in multi-vendor environments.

Education and Awareness: Despite the growing awareness of the security risks posed by drones, many organizations and individuals remain uninformed or ill-prepared to address these threats effectively. Companies in the drone countermeasures market must invest in education and awareness initiatives to educate customers, stakeholders, and the public about the risks associated with rogue drones and the importance of implementing effective countermeasures.

Cybersecurity Risks: As drones become increasingly connected and reliant on digital technologies, they are also vulnerable to cybersecurity threats such as hacking, malware, and data breaches. Companies developing drone countermeasures solutions must incorporate robust cybersecurity measures to protect against cyber threats and ensure the integrity, confidentiality, and availability of their systems and data.

Environmental Impact: The deployment of countermeasure technologies such as jamming and spoofing may have unintended environmental consequences, including electromagnetic interference, signal pollution, and disruption to wildlife and ecosystems. Companies must conduct comprehensive environmental assessments and mitigation measures to minimize the impact of their operations on the environment and wildlife habitats.

Conclusion

In conclusion, the drone countermeasures market presents significant opportunities for companies offering innovative solutions to address the growing threat of rogue drones. By focusing on technological innovation, regulatory compliance, strategic partnerships, and continuous adaptation to emerging trends, companies can successfully navigate the competitive landscape and capitalize on the burgeoning demand for effective drone security solutions. As the market continues to evolve, companies that can anticipate and respond to changing customer needs and market dynamics will be well-positioned to thrive in this rapidly growing industry.

0 notes

Text

Revolutionizing Industries: 3D Printing Materials Market Set to Surge to US$ 6.6 Billion by 2033

The market for 3D printing materials is anticipated to reach an estimated value of US$ 6.6 billion by 2033, up from US$ 1.8 billion in 2023, and grow at a compound annual growth rate of 14.2% between 2023 and 2033.

During the projection period, it is expected that the market for 3D printing materials will grow at an astounding 14.2% CAGR. Worldwide sales of 3D printers are being driven by the quick uptake of technologically superior production equipment across numerous industries, which is anticipated to expand the market in the upcoming years.

Raw materials used for 3D printing include plastics, ABS, PLA, metals & powders, carbon fibers, and resins. The market is being supported by the growing trend of using 3D printers to produce a range of small and large products.

Request a Sample of this Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-1777

Additionally, the market is anticipated to develop as 3D printing is increasingly used in the building and construction industry. Additionally, it is projected that the rise of the automotive, aerospace, electronics, and medical industries will continue to be a major growth driver of the global market for 3D printing materials.

North America is anticipated to continue to be a lucrative region in the global market for 3D printing materials, according to FMI. The rapid commercialization of cutting-edge technology like 3D printing across a variety of businesses in the area is responsible for the growth.

Key Takeaways:

By material type, sales in the metal segment are forecast to grow at a 14.9% CAGR over the assessment period.

Based on form, demand for powder 3D printing materials is projected to increase at a 13.5% CAGR through 2031.

In terms of applications, sales in the automotive sector are forecast to gain traction at a 13.6% CAGR over the forecast period.

The U.S. will emerge as a lucrative pocket in the North American 3D printing materials market.

Sales in the China 3D printing materials market are projected to increase at a 15.2% CAGR through 2031.

Competition Landscape

Key market participants in the global 3D printing materials market elaborated in the report include Covestro AG, Arkema S.A., Sandvik A.B., Evonik Industries A.G., EOS GmbH Electro Optical Systems, Ultimaker B.V., Hoganas AB, The EXONE Company, General Electrics, 3D Systems Corporation, Materialise NV, STRATASYS LTD, and MARKFORGED Inc.

Key market participants are focusing on the development of innovative 3D printing products to improve their product portfolios. Besides this, players are also investing in mergers, acquisitions, and collaborations to expand their global presence.

For instance:

In April 2021, Sandvik and its subsidiary BEAMIT Group announced a new capacity for additive manufacturing components in super-duplex stainless steel, an alloy that combines mechanical strength with extremely high corrosion resistance.

Request for Methodology:

https://www.futuremarketinsights.com/request-report-methodology/rep-gb-1777

3D printing materials Market By Category

By Material Type:

Plastics

Metals

Ceramics

Others

By Form:

Filament

Powder

Liquid

By Application:

Electronics & Consumers

Automotive

Medical

Industrial

Education

Aerospace

Others

0 notes

Text

Airborne Weapon System Market Forecasted to Expand Rapidly, Projecting US$ 119 Billion Value by 2032, with 3.6% CAGR

The market for airborne weapon systems was estimated to be worth US$ 80.5 billion in 2021 and is expected to grow by 3.7% year over year to reach US$ 83.6 billion in 2022. Demand is predicted to increase at a 3.6% value CAGR over the assessment period of 2022–2032, most likely reaching US$ 119 billion by the conclusion of the forecast period.

Until 2032, the market for airborne weapon systems is expected to provide an absolute monetary opportunity of US$ 38.5 billion. Fighter jet airborne weapon system sales are expected to grow at a recorded CAGR of 3.1% from 2015 to 2021. Furthermore, airborne missiles will probably see a 3.8% compound annual growth rate (CAGR) from 2022 to 2032, remaining the predominant armament choice. During the projection period, North America is expected to maintain its leading position and generate an opportunity valued at US$ 13 billion.

𝗗𝗼𝘄𝗻𝗹𝗼𝗮𝗱 𝗮 𝗦𝗮𝗺𝗽𝗹𝗲 𝗖𝗼𝗽𝘆 𝗢𝗳 𝗥𝗲𝗽𝗼𝗿𝘁:

In the context of contemporary conflict, air superiority continues to be a vital goal for armed forces across the globe. Modern airborne weaponry is essential to achieving this goal because it allows planes to carry out precision strikes with unmatched efficacy and accuracy. This article explores the ever-changing Airborne Weapon System Market, revealing its history, major developments, and the forces propelling innovation and expansion.

𝗖𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗶𝘃𝗲 𝗟𝗮𝗻𝗱𝘀𝗰𝗮𝗽𝗲:

Leading producers of airborne weapon systems are keeping an eye on technical advancements to ensure that their clients receive the most exact and accurate weapon system configurations. In order to increase their presence in key regions, businesses are collaborating with governments as the possibility of war looms large over the globe.

The new FN® Airborne Extended Digital Suite was unveiled by FN Herstal at the DSEI international trade event in London in September 2021. This suite integrates high-performance technology, including digital machine gun pods from Thales, EO/IR systems from Safran, and laser-guided/unguided rockets from Thales, to substantially improve the combat capabilities of rotary and fixed-wing aerial aircraft.

Similarly, Safran SA provides the Airborne Electro-Optical System Euroflir 410. The device enables search and rescue, protection, and intelligence missions to be conducted by unmanned aerial vehicles (UAVs) and fixed and rotary wing aircraft in any weather. Its long-range observation, precise targeting, and designating capabilities make this possible.

For the US military's ground and flight tests, Lockheed Martin finished the factory acceptance testing of the Airborne High Energy Laser (AHEL) in October 2021. The AHEL component was supplied by the business to be integrated with other systems in advance of ground testing and, eventually, flight testing on the AC-130J aircraft. Lockheed Martin was given a $12 million cost-plus-fixed fee, indefinite-delivery, five-year contract in July 2021 by the Naval Surface Warfare Center, Dahlgren Division for technical services, integration, test, and demonstration for the AHEL system.

Airborne Weapon Systems' Development:

Due to developments in military tactics, technology, and geopolitical dynamics, airborne weapon systems have seen a remarkable transformation from the early days of aerial conflict to the present. Simple bombs and machine guns mounted atop airplanes gave way to a complex arsenal of guided missiles, precision-guided munitions, and intelligent weapons that could hit targets at great distances with extreme accuracy. Airborne weapon systems nowadays are equipped with a broad range of capabilities, including as anti-ship, air-to-air, and air-to-ground weapons, that are intended to neutralize threats in the air, sea, and land domains.

Growth catalysts and market dynamics:

The market for airborne weapon systems is expanding rapidly due to a number of causes. Governments are investing in advanced airborne weapon systems as a means of modernizing their defense capabilities in response to global security concerns and rising geopolitical tensions. Furthermore, the emergence of challenges related to asymmetric warfare, such insurgency and terrorism, has highlighted the necessity of having precision-strike capabilities in order to counter non-traditional enemies. Further fueling innovation in airborne weapon systems is the development of technological innovations like stealth technology, unmanned aerial vehicles (UAVs), and network-centric warfare systems, which improve the lethality, survivability, and interoperability of these systems.

𝗞𝗲𝘆 𝗖𝗼𝗺𝗽𝗮𝗻𝗶𝗲𝘀 𝗣𝗿𝗼𝗳𝗶𝗹𝗲𝗱:

Safran S.A

FN Herstal

Rheinmetall AG

Boeing

BAE Systems Plc.

Saab AB

Lockheed Martin Corporation

Raytheon Company

Ultra-Electronics Holdings

Airbus SE

Important Market Trends:

The development of the airborne weapon system market is being shaped by several trends. The use of machine learning and artificial intelligence (AI) into military systems to improve targeting precision, self-governing decision-making, and responsiveness is one noteworthy development. Aerial vehicles can function with more autonomy and efficiency thanks to AI-enabled systems that can evaluate enormous volumes of data in real-time, recognize risks, and suggest the best courses of action. In addition, there is a growing need for integrated airborne weapon systems that can work together and share data easily because to the emergence of network-centric warfare ideas, which connect various platforms and sensors into a single battlefield network.

Opportunities and Difficulties in the Market:

Notwithstanding its expansion, the Airborne Weapon System Market encounters obstacles including financial limitations, legal impediments, and unstable geopolitical environments. But these difficulties also offer chances for uniqueness in the market and creativity. Through the utilization of open-system architectures, modular design principles, and commercial off-the-shelf (COTS) components, manufacturers may create affordable and versatile airborne weapon systems that satisfy the changing requirements of military forces across the globe. Furthermore, partnerships with universities, research centers, and tech companies can stimulate creativity and hasten the creation of cutting-edge aerial weapon systems of the future.

𝗥𝗲𝗮𝗱 𝗠𝗼𝗿𝗲:

Prospects for the Future:

The market for airborne weapon systems seems to have a bright future. The need for sophisticated airborne weapon systems is predicted to increase due to the military's continuous modernization, the rise of new threats, and the quick speed of technological advancement. Furthermore, manufacturers have a chance to profit from the rising demand for precision-strike and standoff capabilities as defense budgets rise and governments prioritize expenditures in defense capabilities. In the dynamic and competitive global defense market, companies in the Airborne Weapon System Market can position themselves for success by embracing market trends, attending to customer needs, and allocating resources towards research and development.

Key Segments Covered in the Airborne Weapon Systems Market Study:

Airborne Weapon System by Aircraft Type

Airborne Weapon System for Fighter Jets

Airborne Weapon System for Helicopters

Airborne Weapon System by Weapons Type

Airborne Bombs

Airborne Guns

Airborne Rifles

Airborne Missiles

Other Airborne Weapons

Airborne Weapon System by Region

North America Airborne Weapon System Market

Europe Airborne Weapon System Market

Asia Pacific Airborne Weapon System Market

Latin America Airborne Weapon System Market

Middle East & Africa Airborne Weapon System Market

In summary, the market for airborne weapon systems is essential to contemporary military capabilities because it allows air forces to sustain air superiority and project power with accuracy and efficacy. Manufacturers can sustain development and innovation in this critical and dynamic market area by leveraging technical innovation, adjusting to changing threats, and working in tandem with military stakeholders. It is impossible to overestimate the significance of cutting-edge airborne weapon systems in preserving international peace and defending national security in the face of progressively complex security problems.

0 notes

Text

Airborne Intelligence Surveillance and Reconnaissance (ISR) Market Supply-Demand, Investment Feasibility and Forecast 2033

Market Definition

The Airborne Intelligence Surveillance and Reconnaissance (ISR) Market encompasses the industry involved in the development, manufacturing, and deployment of airborne platforms and systems for gathering, analyzing, and disseminating intelligence, surveillance, and reconnaissance data. These platforms and systems are utilized by defense and security agencies to monitor, track, and gather information on enemy activities, threats, and potential targets for strategic, operational, and tactical purposes.

Market Outlook

The Airborne Intelligence Surveillance and Reconnaissance (ISR) Market is experiencing robust growth driven by increasing defense budgets, evolving security threats, and advancements in sensor technologies and unmanned aerial systems (UAS). As defense and security agencies prioritize situational awareness and intelligence gathering capabilities, there is a growing demand for airborne ISR platforms and systems that can provide real-time, actionable intelligence for decision-makers on the battlefield.

One of the primary drivers of market growth is the rising demand for persistent surveillance and reconnaissance capabilities to address asymmetric and hybrid threats, counterterrorism operations, and border security challenges. Airborne ISR platforms, such as manned aircraft, unmanned aerial vehicles (UAVs), and aerostats, play a crucial role in monitoring vast areas of interest, tracking moving targets, and conducting wide-area surveillance for extended durations, providing valuable intelligence for mission planning and execution.

Furthermore, advancements in sensor technologies, data analytics, and communication systems are driving innovation in airborne ISR systems, enabling the integration of multi-sensor payloads, high-resolution imaging sensors, signals intelligence (SIGINT) systems, and synthetic aperture radar (SAR) sensors for enhanced intelligence collection and analysis capabilities. Manufacturers are developing next-generation ISR platforms and payloads that offer improved detection, identification, and tracking of targets, as well as enhanced situational awareness and data fusion capabilities for intelligence analysts.

Moreover, the increasing adoption of unmanned aerial systems (UAS) for ISR missions is driving market growth, as defense and security agencies seek to leverage the operational flexibility, persistence, and cost-effectiveness of unmanned platforms for ISR missions. UAVs equipped with ISR payloads, such as electro-optical/infrared (EO/IR) cameras, SIGINT systems, and communication relays, are being deployed for a wide range of ISR applications, including border surveillance, maritime patrol, counterinsurgency operations, and disaster response.

Additionally, geopolitical tensions, territorial disputes, and the proliferation of asymmetric threats are fueling investments in airborne ISR capabilities by defense forces worldwide. Governments are modernizing their ISR capabilities and investing in advanced airborne platforms, sensor technologies, and data analytics capabilities to maintain strategic superiority, enhance situational awareness, and protect national security interests in contested environments.

To Know More @ https://www.globalinsightservices.com/reports/airborne-intelligence-surveillance-and-reconnaissance-isr-market/

Research Objectives

Estimates and forecast the overall market size for the total market, across product, service type, type, end-user, and region

Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

Identify factors influencing market growth and challenges, opportunities, drivers and restraints

Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

Thoroughly analyze smaller market segments strategically, focusing on their potential, individual patterns of growth, and impact on the overall market

To thoroughly outline the competitive landscape within the market, including an assessment of business and corporate strategies, aimed at monitoring and dissecting competitive advancements.

Identify the primary market participants, based on their business objectives, regional footprint, product offerings, and strategic initiatives

Request the sample copy of report @ https://www.globalinsightservices.com/request-sample/GIS25512/

Market Segmentation

The Airborne Intelligence Surveillance and Reconnaissance (ISR) Market can be segmented by aircraft type, fuel type, and region. By aircraft type, the market can be divided into unmanned ISR and manned ISR. By fuel type, the market can be divided into battery-operated, hydrogen fuel cells, alternate fuel, gas-electric hybrids, and solar-powered. By region, the market is divided into North America, Europe, Asia-Pacific, and the Rest of the World.

Request For Report Customization @ https://www.globalinsightservices.com/request-customization/GIS25512

Major Players

The market includes players such as Bae Systems PLC (UK), Elbit Systems Ltd. (Israel), L3Harris Technologies (US), Northrop Grumman (US), Lockheed Martin Corporation (US), Leonardo Company (Italy), Teledyne Technologies, Inc. (US), Raytheon Technologies (US), Metrea LLC(UK), and Airbus SE(FR).

Request For Discounted Pricing @ https://www.globalinsightservices.com/request-special-pricing/GIS25512

Research Scope

Scope – Highlights, Trends, Insights. Attractiveness, Forecast

Market Sizing – Product Type, End User, Offering Type, Technology, Region, Country, Others

Market Dynamics – Market Segmentation, Demand and Supply, Bargaining Power of Buyers and Sellers, Drivers, Restraints, Opportunities, Threat Analysis, Impact Analysis, Porters 5 Forces, Ansoff Analysis, Supply Chain

Business Framework – Case Studies, Regulatory Landscape, Pricing, Policies and Regulations, New Product Launches. M&As, Recent Developments

Competitive Landscape – Market Share Analysis, Market Leaders, Emerging Players, Vendor Benchmarking, Developmental Strategy Benchmarking, PESTLE Analysis, Value Chain Analysis

Company Profiles – Overview, Business Segments, Business Performance, Product Offering, Key Developmental Strategies, SWOT Analysis

For In-Depth Competitive Analysis, Buy Now @ https://www.globalinsightservices.com/checkout/single_user/GIS25512/

About Us

With Global Insight Services, you receive:

10-year forecast to help you make strategic decisions

In-depth segmentation which can be customized as per your requirements

Free consultation with lead analyst of the report

Infographic excel data pack, easy to analyze big data

Robust and transparent research methodology

Unmatched data quality and after sales service

Contact Us:

Global Insight Services LLC

16192, Coastal Highway, Lewes DE 19958

E-mail: [email protected]

Phone: +1-833-761-1700

Website: https://www.globalinsightservices.com/

0 notes

Text

The Impact of Fifth-Generation Fighters on Modern Warfare

The world of military aviation has witnessed remarkable advancements over the decades, with each generation of fighter aircraft pushing the boundaries of technology, performance, and capabilities. Among these, the Fifth-Generation Fighter stands out as a pinnacle of innovation, integrating cutting-edge technologies to redefine aerial warfare. In this blog post, we delve into the evolution, features, and impact of Fifth-Generation Fighters on modern air combat.

Understanding Fifth-Generation Fighters

Fifth-Generation Fighters represent the latest leap in fighter aircraft design, characterized by a combination of stealth capabilities, advanced avionics, high-performance engines, integrated sensor suites, and network-centric warfare capabilities. These aircraft are designed to operate in highly contested environments, engaging both air and ground targets with unprecedented precision and lethality.

Evolution from Fourth to Fifth Generation

The transition from Fourth-Generation to Fifth-Generation Fighters marks a significant leap in technological sophistication and operational capabilities. Here's a brief overview of the key differences between these generations:

Stealth Technology: Fifth-Generation Fighters incorporate advanced stealth technology, including radar-absorbent materials, reduced radar cross-section (RCS), and stealthy shaping to evade enemy detection and enhance survivability in hostile environments.

Sensor Fusion: Fifth-Generation aircraft feature integrated sensor suites that combine radar, infrared sensors, electronic warfare systems, and data fusion algorithms to provide pilots with real-time situational awareness and actionable intelligence.

Networking Capabilities: Fifth-Generation Fighters are designed for network-centric warfare, enabling seamless communication and data sharing with other platforms, ground stations, and command centers to facilitate collaborative operations and decision-making.

Advanced Avionics: These aircraft are equipped with state-of-the-art avionics, including advanced flight control systems, digital cockpit displays, helmet-mounted displays (HMDs), and next-generation mission computers for enhanced mission planning and execution.

Precision Weapons Systems: Fifth-Generation Fighters employ precision-guided munitions, advanced air-to-air missiles, and standoff weapons to engage targets with unmatched accuracy and lethality, minimizing collateral damage and maximizing mission success.

Key Features of Fifth-Generation Fighters

Let's delve deeper into the key features that define Fifth-Generation Fighters and set them apart from their predecessors:

Stealth and Low Observability: Fifth-Generation aircraft leverage stealth technology to reduce their radar, infrared, and acoustic signatures, making them difficult for enemy radars and sensors to detect and track, thus enhancing survivability in contested airspace.

Integrated Sensor Fusion: These fighters integrate multiple sensors, including active and passive radar, electro-optical/infrared (EO/IR) sensors, and electronic support measures (ESM), to provide pilots with a comprehensive and fused picture of the battlespace in real time.

Data Link and Connectivity: Fifth-Generation Fighters are equipped with advanced data link systems that enable secure communication and data sharing among friendly forces, allowing for coordinated operations, target sharing, and situational awareness across the battlespace.

High-Performance Engines: These aircraft are powered by advanced turbofan engines optimized for performance, efficiency, and stealth characteristics, providing exceptional speed, maneuverability, and range while minimizing infrared and radar signatures.

Advanced Cockpit and Human-Machine Interface: Fifth-Generation cockpits feature digital displays, touch screens, voice-activated controls, and helmet-mounted displays (HMDs) that enhance pilot situational awareness, decision-making, and mission effectiveness.

Impact on Modern Air Combat

The introduction of Fifth-Generation Fighters has had a profound impact on modern air combat operations, offering several advantages and capabilities:

Stealth and Survivability: Fifth-Generation aircraft's stealth capabilities allow them to penetrate defended airspace, conduct strikes deep inside enemy territory, and evade detection and engagement by hostile air defenses, enhancing mission success and survivability.

Situational Awareness: Integrated sensor fusion and advanced avionics provide pilots with unparalleled situational awareness, enabling them to detect, track, and engage multiple threats simultaneously while prioritizing targets based on real-time intelligence.

Precision Strikes: Fifth-Generation Fighters employ precision-guided munitions and advanced targeting systems to conduct surgical strikes with high accuracy, minimizing collateral damage and civilian casualties while maximizing operational effectiveness.

Electronic Warfare and Countermeasures: These aircraft are equipped with sophisticated electronic warfare (EW) systems, including jamming capabilities, radar warning receivers (RWR), and defensive countermeasures, to protect against enemy threats and disrupt adversary communications and sensors.

Network-Centric Operations: Fifth-Generation Fighters are integral to network-centric warfare, leveraging data link connectivity to share information, coordinate with other platforms, and contribute to a cohesive and synergistic air combat environment.

Examples of Fifth-Generation Fighters

Several countries have developed and deployed Fifth-Generation Fighters, each with unique capabilities and roles. Some notable examples include:

Lockheed Martin F-22 Raptor (United States): The F-22 Raptor is renowned for its stealth, supercruise capability, and advanced avionics, making it a dominant force in air superiority missions.

Lockheed Martin F-35 Lightning II (United States): The F-35 Lightning II is a versatile multirole fighter with stealth capabilities, integrated sensor fusion, and vertical takeoff and landing (VTOL) capabilities, serving the needs of various branches of the U.S. military and several international partners.

Sukhoi Su-57 (Russia): The Su-57 is Russia's first operational Fifth-Generation Fighter, featuring stealth technology, advanced avionics, and supermaneuverability for air superiority and ground attack missions.

Chengdu J-20 (China): China's J-20 is a stealthy air superiority fighter designed to counter advanced adversaries, showcasing China's advancements in aerospace technology and military capabilities.

Eurofighter Typhoon (Europe): While not classified as a Fifth-Generation Fighter, the Eurofighter Typhoon incorporates advanced technologies and capabilities, including AESA radar, advanced avionics, and high maneuverability, making it a formidable platform in modern air combat scenarios.

Conclusion: Advancing Air Power with Fifth-Generation Fighters

In conclusion, Fifth-Generation Fighters represent a paradigm shift in aerial warfare, combining stealth, advanced sensors, networking capabilities, and precision weaponry to dominate the skies and achieve mission success in highly contested environments. These aircraft serve as force multipliers for modern air forces, offering unmatched capabilities for air superiority, strike missions, reconnaissance, electronic warfare, and beyond. As technology continues to evolve, Fifth-Generation Fighters will remain at the forefront of military aviation, shaping the future of air power and defense capabilities worldwide.

0 notes

Text

L'RWS R400 di EOS impiegato con successo nelle prove anti drone

In Australia Electro Optic Systems (EOS) e il Robotic and Autonomous Systems Implementation & Coordination Office (RICO) hanno raggiunto un traguardo significativo nella loro collaborazione, dimostrando le avanzate capacità di fuoco a lungo raggio e la precisione del sistema d’arma remota R400 di EOS (RWS). Dalla struttura high-tech di EOS a Canberra, il team ha controllato a distanza l’RWS integrato su un veicolo corazzato da trasporto personale M113 modificato di stanza presso l’area militare di Puckapunyal dell’Australian Defence Force (ADF) , a circa 550 chilometri di distanza, ingaggiando con successo obiettivi a distanze da 300 a 600 metri. Dopo la dimostrazione, EOS ha

#Epirus#Forze_Armate#Forze_Terrestri#Industria_della_Difesa#australia#Australian_Army#c_uas#EOS#RWS_R400

0 notes

Text

Airborne Sensors Market 2029 By Size, Share, Trends, Growth, Top Companies Forecast

Surge in Unmanned Aerial Vehicles (UAVs) demand and the escalating requirement for environmental monitoring and climate research are factors driving the Global Airborne Sensors market in the forecast period 2025-2029.

According to TechSci Research report, “Airborne Sensors Market - Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2029”, the Global Airborne Sensors Market stood at USD 9.2 billion in 2023 and is anticipated to grow with a CAGR of 6.90% in the forecast period, 2025-2029. The global airborne sensors market is a crucial component of the aerospace and defense industry, playing a pivotal role in various applications ranging from military surveillance to environmental monitoring and disaster management. As technological advancements continue to drive innovation, the airborne sensors market has witnessed significant growth and evolution in recent years.

One of the primary drivers propelling the growth of the airborne sensors market is the increasing demand for unmanned aerial vehicles (UAVs) or drones across both military and commercial sectors. UAVs equipped with sophisticated sensors enable real-time data collection, intelligence gathering, and surveillance, making them indispensable assets for defense and security agencies worldwide. Moreover, the growing adoption of UAVs in civil applications such as agriculture, infrastructure inspection, and disaster response further fuels the demand for airborne sensors.

Advancements in sensor technology, including the development of lightweight and compact sensors with enhanced capabilities, have expanded the scope of airborne surveillance and reconnaissance missions. These sensors encompass a wide range of technologies, including electro-optical/infrared (EO/IR), synthetic aperture radar (SAR), hyperspectral imaging, LiDAR (Light Detection and Ranging), and multispectral imaging, among others. Such sensors enable precise detection, identification, and tracking of targets or objects of interest, enhancing situational awareness and mission effectiveness.

In addition to military and civil applications, the airborne sensors market is witnessing growing opportunities in environmental monitoring, climate research, and disaster management. Airborne remote sensing platforms equipped with specialized sensors play a vital role in monitoring environmental parameters, detecting natural disasters such as wildfires, floods, and hurricanes, and assessing their impact. These sensors provide valuable data for scientific research, resource management, and decision-making processes aimed at mitigating environmental risks and enhancing resilience.

The increasing focus on border security, maritime surveillance, and counter-terrorism efforts drives the demand for airborne sensor systems capable of monitoring vast areas and detecting potential threats in real-time. Integrated sensor suites, including electro-optical, infrared, and radar sensors, enable comprehensive surveillance capabilities, enabling defense and security agencies to enhance border protection and maritime domain awareness.

The commercial aviation sector also contributes to the growth of the airborne sensors market, particularly in the context of aircraft health monitoring and maintenance. Advanced sensor systems installed onboard commercial aircraft enable continuous monitoring of various parameters such as engine performance, structural integrity, and component health, facilitating predictive maintenance and reducing downtime. These sensors play a crucial role in ensuring the safety, reliability, and efficiency of commercial air transportation.

However, the airborne sensors market faces challenges such as regulatory hurdles, privacy concerns, and interoperability issues, particularly in the context of cross-border operations and data sharing. Additionally, cybersecurity threats pose a significant risk to airborne sensor systems, emphasizing the need for robust cybersecurity measures to safeguard sensitive data and ensure mission integrity.

Browse over XX market data Figures spread through XX Pages and an in-depth TOC on "Global Airborne Sensors Market”

https://www.techsciresearch.com/report/airborne-sensors-market/22482.html

North America is a significant player in the global airborne sensors market, driven by the presence of leading aerospace and defense companies, as well as robust investments in research and development. The region benefits from a strong military presence, which drives demand for advanced sensor technologies for surveillance, reconnaissance, and intelligence gathering purposes. Additionally, the growing adoption of unmanned aerial vehicles (UAVs) for both military and commercial applications further fuels the demand for airborne sensors in this region.

Europe is another prominent market for airborne sensors, with countries like the UK, France, and Germany leading the way in defense spending and technological innovation. The region hosts several key players in the aerospace and defense sector, contributing to the development of cutting-edge sensor technologies. Moreover, increasing investments in border security and surveillance systems drive the demand for airborne sensors across Europe. In the CIS (Commonwealth of Independent States) region, defense modernization efforts and geopolitical tensions stimulate the procurement of advanced airborne sensor systems.

The Asia-Pacific region is witnessing rapid growth in the airborne sensors market, fueled by rising defense budgets, territorial disputes, and the modernization of military capabilities. Countries like China, India, Japan, and South Korea are investing heavily in defense infrastructure and indigenous development of sensor technologies. Additionally, the growing commercial application of UAVs for tasks such as agriculture, infrastructure monitoring, and disaster management contributes to the expansion of the airborne sensors market in the region.

The Middle East & Africa region represents a growing market for airborne sensors, primarily driven by security concerns, regional conflicts, and counter-terrorism efforts. Countries in the Middle East, such as Saudi Arabia, UAE, and Israel, are major buyers of advanced military equipment, including airborne sensor systems, to bolster their defense capabilities. Moreover, the need for surveillance and reconnaissance in remote and hostile environments drives the adoption of unmanned aerial systems equipped with sophisticated sensor payloads.

South America exhibits moderate growth in the airborne sensors market, with countries like Brazil, Argentina, and Chile investing in defense modernization programs and border surveillance systems. The region's vast territorial expanse and diverse geographic features necessitate the use of airborne sensors for monitoring and security purposes. Furthermore, increasing commercial applications of UAVs in industries such as agriculture, mining, and environmental monitoring contribute to the demand for airborne sensor technologies in South America.

Major companies operating in Global Airborne Sensors Market are:

HEXAGON AB

Thales Group

RTX Corporation

Lockheed Martin Corporation

Information Systems Laboratories (ISL)

Teledyne Optech

General Dynamics Corporation

Honeywell International Inc

ITT INC

AVT Airborne Sensing GmbH

Download Free Sample Report

https://www.techsciresearch.com/sample-report.aspx?cid=22482

Customers can also request for 10% free customization on this report

“The global airborne sensors market is a dynamic sector within the aerospace and defense industry, fueled by the escalating demand for advanced situational awareness and data collection capabilities across military, commercial, and scientific applications. Innovations in miniaturization, high-resolution imaging, and the integration of artificial intelligence drive the market's evolution. As airborne platforms, including UAVs and commercial aircraft, play increasingly vital roles, the market's growth is propelled by technological trends that enhance surveillance, reconnaissance, and environmental monitoring capabilities.

However, challenges such as complexity, cybersecurity, and regulatory compliance require strategic solutions. Despite these hurdles, the global airborne sensors market remains a critical enabler of intelligence and operational effectiveness in diverse aerial endeavors.” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based management consulting firm.

“Airborne Sensors Market– Global Industry Size, Share, Trends, Opportunity, and Forecast, Segmented By Type (Non-Scanning, Scanning), By Application (Defense Aircraft, Commercial Aircraft, Others), By Region, Competition, 2019-2029”, has evaluated the future growth potential of Global Airborne Sensors Market and provides statistics & information on market size, structure and future market growth. The report intends to provide cutting-edge market intelligence and help decision makers take sound investment decisions. Besides, the report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in Global Airborne Sensors Market.

Contact Us-

TechSci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Website: www.techsciresearch.com

#Airborne Sensors Market#Airborne Sensors Market Size#Airborne Sensors Market Share#Airborne Sensors Market Trends#Airborne Sensors Market Growth#Airborne Sensors Market Forecast

0 notes

Text

0 notes

Text

Advance Material in Defense Market Forecast Research Report by 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Advance Material in Defense Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Advance Material in Defense Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Advance Material in Defense Market?

The advance material in defense market is expected to grow at a CAGR of 6.4% during the forecast period of 2024 to 2032.

What are Advance Material in Defense?

Advanced materials in defense are specialized materials designed for military use, offering superior performance in terms of strength, durability, and resistance to harsh conditions. These materials, including advanced composites, nanomaterials, and metamaterials, are used in aircraft, vehicles, body armor, and weapons. They are essential for enhancing the capabilities and effectiveness of defense systems, ensuring the safety and success of military operations.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2022

What are the growth prospects and trends in the Advance Material in Defense industry?

The advance material in defense market growth is driven by various factors. The market for advanced materials in defense is growing at a fast pace due to factors such as increased defense spending, advancements in technology, and the demand for materials that are both lightweight and high-performing. These advanced materials, which include composites, ceramics, and alloys, are used in various defense applications, such as aircraft, vehicles, body armor, and weapons systems. Market growth is being driven by the rising need for materials that offer superior strength, durability, and resistance to extreme conditions. Additionally, the development of innovative materials with enhanced properties is expected to create attractive opportunities in the market. Hence, all these factors contribute to advance material in defense market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Type

Aluminum Alloys

Titanium Alloys

Stainless Steel

Nickel-Based Superalloys

Cobalt-Based Superalloys

High-Strength Steel Alloys

Composite Materials

Tungsten and Tungsten Alloys

Beryllium

Magnesium Alloys

By Application

Laser & Microwave Communications

Avionics

Optical Radar Systems

Intelligence, surveillance and reconnaissance (ISR)

Light Detection and Ranging (LIDAR)

Electro-Optical Infrared (EO/IR) Systems

Photonics Lasers

Thermal Imaging

Weapon Systems

Market Segmentation by Region:

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Materion Corporation

Alpine Advanced Materials

Morgan Advanced Materials

Corning

Mitsubishi Chemical Group

Spirit AeroSystems

Permali

View Full Report: https://www.reportsandinsights.com/report/Advance Material in Defense-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

#Advance Material in Defense Market share#Advance Material in Defense Market size#Advance Material in Defense Market trends

0 notes

Text

In videos and new images, see how was the first flight of the KF-21 Boramae, South Korea's first national fighter.

Fernando Valduga By Fernando Valduga 07/21/2022 - 12:00 PM in Military

On July 19, the KF-21 Boramae fighter (Gavian) made its first flight, which lasted about 35 minutes.

According to the Korean Defense Blog's Facebook page, the Republic of Korea Air Force (ROKAF) recently held an official press conference during the presentation of the KF-21 Boramae and revealed several new information about the program.

The Republic of Korea Air Force (RoKAF) commissioned a feasibility study to update the KF-21 to a "5.5" fighter, the first recognition that they are seeking the possible development of a 5th generation fighter. If ROKAF approves such a program after its internal feasibility study, the proposed "Block III" update program may begin after 2026/2028.

ROKAF could also look for a larger aircraft based on the KF-21 platform, nicknamed the KF-XX, instead of the Block III program. This would be a similar update of legacy F/A-18 Hornet for F/A-18E Super Hornet, or F-15 Eagle for F-15E Strike Eagle.

The KF-21 is currently designed to be a "4.5+" generation fighter intended to be one of the most capable in its class with its "stealth" design. Being larger than the F-35, the KF-21 will be significantly more capable than the last F-16V and will eventually replace the F-16s in service at ROKAF.

Block I of KF-21 will only have air-to-air capacity, while Block II will have ground attack capacity.

All 6 flight prototypes were assembled by Korea Aerospace Industries (KAI). According to the Administration of the Defense Acquisition Program (DAPA), approximately 62% of the KF-21 development program has been completed.

Due to global hyperinflation, the initial cost of KF-21 may increase by up to 20%. However, it is expected that the cost will stabilize and that there will be no reduction in orders.

Indonesia has not yet made any progress on late payment. Although negotiations continue, KAI stated that it will not provide prototype aircraft to Indonesia if it does not meet the deadline. Even so, the jet had the flag of Indonesia next to the flag of South Korea painted on the fuselage.

youtube

According to KAI, the aircraft was designed to fly at a maximum speed of Mach 1.81, with a flight range of 2,900 kilometers.

With dimensions of 16.9 m x 4.7 m x 11.2 m, the KF-X is larger than the F-16 and is of similar size to the F-18. The development of the KF-21 began seriously in January 2016 and the ?? Assembly process began in 2019 after the completion of the Critical Design Review (CDR) in 2018.

Lockheed Martin is an official partner of the KF-X program. When ROKAF acquired 40 F-35A fighters, one of the main clauses of the contract included technology transfers, four of which were categorized as "essential technologies" necessary for the development of the KF-21.

The four "main technologies" were: Active Electronic Scanning Radar (AESA), Radio Frequency Jammer (RF), Electro-Optical Targeting Pod (EO-TGP) and Infrared Search and Tracking (IRST).

However, as the U.S. Congress considered them very sensitive and the technology transfer has not been completed, these technologies are being developed internally.

Tags: Military AviationKAI - Korea Aerospace Industries Ltd.KF-21 BoramaeROKAF - Republic of Korea Air Force

Previous news

Azerbaijan Airlines wants to expand its Boeing 787 Dreamliner fleet with four more planes

Next news

Fundraising campaign began in Norway to buy Bayraktar drones to Ukraine

Fernando Valduga

Fernando Valduga

Aviation photographer and pilot since 1992, he has participated in several events and air operations, such as Cruzex, AirVenture, Dayton Airshow and FIDAE. He has works published in a specialized aviation magazine in Brazil and abroad. He uses Canon equipment during his photographic work in the world of aviation.

Related news

TB2 Bayraktar drone donated by the Turkish company Baykar, after fundraising made by Lithuania.

MILITARY

Fundraising campaign began in Norway to buy Bayraktar drones to Ukraine

07/21/2022 - 12:30 PM

MILITARY

Russia may have knocked down another of its fighter jets - were they aiming at an American missile?

07/21/2022 - 08:32 AM

MILITARY

U.S. senators say Pentagon should donate fighter jets to Ukraine

07/20/2022 - 9:41 PM

F/A-18 demonstrates compatibility of aircraft carriers with the requirements of the Indian Navy.

MILITARY

VIDEO: Boeing F/A-18 Super Hornet successfully concludes operational demonstrations in India

07/20/2022 - 6:40 PM

MILITARY

US authorizes training for Ukrainian pilots on F-15 and F-16 fighters

07/20/2022 - 4:00 PM

MILITARY

Kratos completes series of flights with two production XQ-58A Valkyrie UAVs

07/20/2022 - 2:00 PM

HOME Main Page Editorials Information Events Collaborate SPECIALS Advertise About

Cavok Brasil - Digital Tchê Web Creation

Commercial

Executive

Helicopters

History

Military

Brazilian Air Force

Space

SPECIALS

Cavok Brasil - Digital Tchê Web Creation

9 notes

·

View notes

Text

EOS and Australian Army Set Uncrewed M113 APC Live Fire Milestone

Electro Optic Systems (EOS) and the Robotic and Autonomous Systems Implementation & Coordination Office (RICO) have reached a significant milestone in their collaboration, demonstrating the advanced long-range firing capabilities and precision of EOS' R400 remote weapon system (RWS). From EOS’ high-tech facility in Canberra, the team remotely controlled the RWS integrated on a modified M113 Armoured Personnel Carrier (APC) stationed at the Australian Defence Force (ADF) Puckapunyal Military Area, approximately 550 kilometres away, successfully engaging targets at distances of 300 and 600 metres.

#military #defense #defence #militaryleak #m113 #australia

Electro Optic Systems (EOS) and the Robotic and Autonomous Systems Implementation & Coordination Office (RICO) have reached a significant milestone in their collaboration, demonstrating the advanced long-range firing capabilities and precision of EOS’ R400 remote weapon system (RWS). From EOS’ high-tech facility in Canberra, the team remotely controlled the RWS integrated on a modified M113…

View On WordPress

0 notes

Text

Key Players in the Australian Defense Market: Defense Contractors, Suppliers, and Technology Providers

In the Australian defense market, there are several key players, including defense contractors, suppliers, and technology providers.

To gain more information about the Australia defense market forecast, download a free report sample

Here are some of the prominent companies operating in this sector:

1. Defense Contractors:

BAE Systems Australia: BAE Systems Australia is a subsidiary of the British multinational defense, security, and aerospace company BAE Systems plc. It is one of the largest defense contractors in Australia, providing a wide range of products and services including naval ships, submarines, armored vehicles, and defense electronics.

Thales Australia: Thales Australia is a subsidiary of the French multinational aerospace and defense company Thales Group. It is a leading provider of defense technology and solutions in Australia, specializing in areas such as communication systems, electronic warfare, cybersecurity, and naval systems.

Lockheed Martin Australia: Lockheed Martin Australia is a subsidiary of the American aerospace and defense company Lockheed Martin Corporation. It provides a diverse range of defense and aerospace products, including aircraft, missile systems, surveillance systems, and cybersecurity solutions.

Northrop Grumman Australia: Northrop Grumman Australia is a subsidiary of the American aerospace and defense company Northrop Grumman Corporation. It offers a wide range of defense and security solutions, including unmanned aircraft systems, electronic warfare systems, and cybersecurity services.

Rheinmetall Defence Australia: Rheinmetall Defence Australia is a subsidiary of the German multinational defense and automotive company Rheinmetall AG. It specializes in armored vehicles, weapon systems, ammunition, and military technology solutions.

2. Suppliers and Technology Providers:

ASC Pty Ltd: ASC Pty Ltd is Australia's largest defense shipbuilding company, specializing in the construction, maintenance, and sustainment of naval vessels including submarines and surface ships.

Electro Optic Systems (EOS): EOS is an Australian technology company that designs, manufactures, and supplies advanced electro-optic systems, including remotely operated weapon systems, laser systems, and surveillance sensors for defense and security applications.

Cubic Defence Australia: Cubic Defence Australia is a subsidiary of Cubic Corporation, a leading provider of defense training and simulation systems. It delivers training and simulation solutions for defense forces in Australia and around the world.

Cochlear Limited: Cochlear Limited is an Australian medical technology company that develops and manufactures cochlear implant systems for people with hearing loss. Its technology has applications in defense, particularly in communication and hearing protection for military personnel.

Saab Australia: Saab Australia is a subsidiary of the Swedish aerospace and defense company Saab AB. It provides a range of defense and security solutions, including surveillance systems, naval combat systems, and communication systems.

These are just a few examples of the key players in the Australian defense market. The sector also includes a diverse range of small and medium-sized enterprises (SMEs) specializing in niche areas such as aerospace, cybersecurity, and intelligence technology, which contribute to the overall defense industry ecosystem in Australia.

0 notes

Last Seen Blogs

sparklitive-sonya

boys behind closed doors...

tigerafe-blog

Black Panther

savedbylace

Saved By Lace Boutique

marsweetie02

marsweetie02

galerisoyut

GALERİ SOYUT