#Crop Protection Market Major Players

Text

Market Segmentation and Regional Analysis in the Crop Protection Industry

The crop protection market is diverse and complex, with a wide range of products, technologies, and applications catering to different crops and regions. In this blog, we will explore the market segmentation and regional dynamics of the crop protection industry, providing insights into key market trends and opportunities.

Market Segmentation:

The Crop Protection Market can be segmented based on product type, crop type, application method, and mode of action. Major product categories include herbicides, insecticides, fungicides, and biopesticides, each targeting specific pests, diseases, and weeds. Crop protection products are used across various crop categories, including cereals, fruits, vegetables, and oilseeds.

Regional Analysis:

The global crop protection market is geographically diverse, with different regions exhibiting varying market dynamics and growth potentials. Some of the key regions driving market growth include:

North America: North America is a significant market for crop protection products, driven by extensive agricultural land, advanced farming practices, and high adoption of biotechnology. The United States and Canada are major contributors to market growth, with a strong focus on innovation and technology adoption.

Europe: Europe is another prominent market for crop protection products, characterized by stringent regulatory frameworks and increasing demand for sustainable agriculture solutions. The European Union has strict regulations governing pesticide use, driving the adoption of biological and organic alternatives.

Asia-Pacific: The Asia-Pacific region is witnessing rapid growth in the crop protection market, fueled by population growth, urbanization, and increasing food demand. Countries such as China, India, and Australia are key contributors to market expansion, with a growing focus on improving crop yields and quality.

Latin America: Latin America is a major agricultural hub, known for its large-scale production of crops such as soybeans, corn, and sugarcane. Brazil and Argentina are key markets for crop protection products, driven by extensive cropland and favorable climatic conditions.

Key Market Trends:

Shift Towards Biologicals: There is a growing trend towards the use of biological crop protection products in response to consumer demand for safer and more sustainable agricultural practices. Biopesticides, biofertilizers, and microbial-based solutions are gaining popularity as alternatives to synthetic chemicals.

Digitalization and Precision Agriculture: Digital farming technologies are transforming crop protection practices, enabling farmers to monitor fields, detect pest infestations, and optimize inputs more efficiently. Sensors, drones, and satellite imagery provide real-time data for precision application of crop protection products.

Sustainable Agriculture Initiatives: Sustainability is a key focus area in the crop protection industry, with companies and policymakers promoting eco-friendly solutions and conservation practices. Integrated pest management (IPM), organic farming, and agroecological approaches are gaining traction as sustainable alternatives to conventional crop protection methods.

Opportunities and Challenges:

The Crop Protection Market presents numerous opportunities for innovation, collaboration, and market expansion. However, it also faces challenges such as regulatory constraints, resistance issues, and environmental concerns. Companies that invest in research and development, develop sustainable solutions, and adapt to changing market dynamics can succeed in this competitive landscape.

Conclusion:

In conclusion, the crop protection market is dynamic and evolving, driven by changing consumer preferences, technological advancements, and sustainability imperatives. Understanding market segmentation and regional dynamics is essential for stakeholders to identify growth opportunities, navigate regulatory challenges, and capitalize on emerging market trends. By staying informed and proactive, companies can position themselves for success and contribute to sustainable agriculture practices globally.

#Crop Protection market#Crop Protection Industry#Crop Protection market share#Crop Protection market analysis#Crop Protection market challenges#Crop Protection market emerging players#Crop Protection market growth#Crop Protection market top players#Crop Protection market major players#Crop Protection market opportunities#Crop Protection market trends#Crop Protection market research reports#Crop Protection Industry research reports#Global Crop Protection Industry#Global Crop Protection Market#Crop Protection Industry outlook

0 notes

Text

The Green Shield Explored - Understanding Crop Protection Market

Introduction

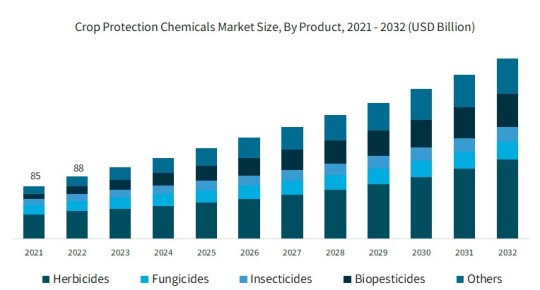

In the intricate tapestry of agriculture, where the dance of nature meets the demands of a growing population, the Crop Protection Chemicals Market emerges as a crucial guardian. This market, projected to grow from USD 66.04 billion in 2023 to USD 80.35 billion by 2028, at a CAGR of 4%, plays a pivotal role in ensuring healthy crops and securing agricultural productivity. As we navigate through the nuances of this industry, we'll explore market trends, regional dynamics, and the significant players shaping the landscape.

Market Analysis and Research Reports

Crop Protection Market Analysis

A comprehensive Crop Protection market analysis involves scrutinizing various facets, from industry trends to economic factors influencing market dynamics. Analyzing the market allows stakeholders to gain insights into the demand for crop protection products, emerging technologies, and competitive landscapes.

Crop Protection Market Research Report

In-depth Crop Protection market research reports serve as invaluable resources for industry stakeholders. These reports offer detailed analyses of market trends, growth opportunities, and challenges. Armed with this information, businesses can make informed decisions, anticipate market shifts, and formulate strategic plans.

Market Size and Share

Crop Protection Market Size

The Crop Protection market size is a pivotal metric, reflecting the magnitude of the industry's influence. It encompasses the total value of crop protection products traded globally, indicating the economic significance of safeguarding agricultural yields.

Crop Protection Market Share

Understanding Crop Protection market share is essential for gauging the competitive landscape. This metric delineates the distribution of market influence among key players, allowing for insights into industry dominance and areas for potential collaboration or disruption.

Market Trends and Dynamics

Crop Protection Market Trends

Staying abreast of evolving Crop Protection market trends is crucial for industry stakeholders. These trends encompass advancements in integrated pest management, the rise of biopesticides, and the integration of precision agriculture technologies. Embracing these trends positions businesses to meet the changing needs of farmers and consumers.

Challenges and Opportunities

The Crop Protection industry is not without challenges. Crop Protection market challenges may include regulatory hurdles, resistance development in pests, and public concerns about the environmental impact of certain products. Addressing these challenges requires innovative solutions and collaboration across the industry.

Amid challenges, there are abundant Crop Protection market opportunities. The industry is witnessing increased demand for sustainable and eco-friendly solutions, creating avenues for innovation. Opportunities also abound in digital technologies that enhance precision in application and reduce environmental impact.

Major, Top, and Emerging Players

1.Crop Protection Market Major Players

Several companies stand out as major players in the Crop Protection market. These industry giants contribute significantly to the development and distribution of crop protection solutions, shaping the overall landscape.

2.Crop Protection Market Top Players

The top players in the Crop Protection market are those that lead in terms of market share, innovation, and global presence. Their strategies and product offerings influence market trends and set benchmarks for the industry.

3.Crop Protection Market Emerging Players

The emerging players in the Crop Protection market represent the innovative vanguard, introducing novel solutions and technologies. These players often disrupt traditional markets, contributing to the industry's growth and evolution.

Growth and Opportunities

Crop Protection Market Growth

Crop Protection market growth is fueled by a combination of factors, including population growth, increasing awareness about sustainable agriculture, and the need for enhanced food production. Understanding the drivers of growth is key to capitalizing on emerging opportunities.

Crop Protection Market Opportunities

Beyond challenges, the Crop Protection market opportunities lie in embracing sustainable practices, developing precision agriculture technologies, and creating solutions tailored to specific regional needs. Seizing these opportunities contributes to the industry's resilience and long-term success.

Conclusion: Safeguarding Agriculture Future

In conclusion, the Crop Protection Chemicals Market stands as a dynamic force in the world of agriculture, addressing challenges, fostering sustainable practices, and ensuring the guardianship of tomorrow's harvest. From the rising tide of organic farming to the regional dynamics shaping consumption patterns, the journey through this market is a testament to the industry's resilience and commitment to global food security. As players continue to innovate and navigate challenges, the guardians of the harvest remain steadfast, ready to embrace the evolving landscape of agriculture

#Crop Protection market#Crop Protection market analysis#Crop protection market research report#Crop Protection market share#Crop Protection market trends#Crop Protection market challenges#Crop Protection market major players#Crop Protection market top players#Crop Protection market emerging players#Crop Protection market growth#Crop Protection market opportunities

0 notes

Text

The artificial intelligence race is gathering pace, and the stakes could not be higher. Major corporate players—including Alibaba, DeepMind, Google, IBM, Microsoft, OpenAI, and SAP—are leveraging huge computational power to push the boundaries of AI and popularize new AI tools such as GPT-4 and Bard. Hundreds of other private and non-profit players are rolling out apps and plugins, staking their claims in this fast-moving frontier market that some enthusiasts predict will upend the way we work, play, do business, create wealth, and govern.

Amid all the enthusiasm, there is a mounting sense of dread. A growing number of tech titans and computer scientists have expressed deep anxiety about the existential risks of surrendering decision-making to complex algorithms and, in the not so distant future, super-intelligent machines that may abruptly find little use for humans. A 2022 survey found that roughly half of all responding AI experts believed there is at least a one in 10 chance these technologies could doom us all. Whatever the verdict, as recent U.S. congressional testimony from OpenAI CEO Sam Altman reveals, AI represents an unprecedented shift in the social contract that will fundamentally redefine relations between people, institutions, and nations.

Adding to these ominous existential worries is the already lopsided distribution of power and wealth, ensuring that the winnings of future upheaval will accrue disproportionately to the 1 percent. But if AI menaces white-collar jobs and empowers undemocratic interests in privileged countries, what to say about the fallout in those parts of the world where billions toil in the informal sector without safety nets, making them even easier marks for power elites and their digital tools? However the AI disruption plays out worldwide, there is scant hope that, without mitigation, safeguards, and compensation such as universal basic income, the world will be a more equitable place to live, work, or vote.

Fears about the existential risks posed by machine intelligence are hardly new. In his 1872 novel Erewhon, Samuel Butler prophesied that sentient machines would eventually replace humans. In 1942, master science fiction writer Isaac Asimov famously laid out his three laws for robotics: Robots may not injure humans, must obey orders from humans as long as this does not violate the first law, and must protect humans’ existence as long as this does not violate the first two laws. A few years later, in 1950, Alan Turing imagined machines that could converse with humans, while in 1965 Irving John Good predicted a machine-driven “intelligence explosion.” The world had to wait another half century for the promised AI revolution to arrive.

And yet for all the historical premonitions, the current furor over AI is as unprecedented as it is uniquely unsettling. For one, the latest crop of highly advanced large language models and the computational power driving them are no longer confined to the laboratory but are already being used by hundreds of millions of people. Another cause for concern is that some of the most outspoken AI advocates are now convinced that its unregulated use poses a fatal risk to humanity in the near future. What was once floated as a distant theoretical threat is now a clear and present danger—so much so that technologists such as Eliezer Yudkowsky, Geoffrey Hinton, and Max Tegmark and more than 31,000 other people have called for a pause in training the most powerful forms of AI, which they see as among the “most profound risks to society and humanity” today.

Well before the latest outbreak of anxiety, governments, businesses and universities across North America and Western Europe were debating the real and potential harms associated with AI. Their attention converged on at least four possible threats. The first is the existential threat posed by super intelligent machines that may quickly dispose of humans. The second is widespread and accelerating unemployment, with Goldman Sachs recently estimating that as many as 300 million jobs are at risk of being replaced by AI. The third major concern relates to the disturbing way AI imitates and shares text, voice, and video—and could thus supercharge misinformation and disinformation. A fourth fear is that AI could be used to build doomsday technologies—such as biological or cyber viruses—with devastating consequences.

We are not yet at the mercy of thinking machines. As awareness of AI risks has grown, so too have standards and guidance to mitigate them. But for the most part, these are voluntary, including hundreds of protocols and principles advocating for responsible design and self-restraint. Common priorities include aligning AI with the best interests of humans and promoting safety in the design and deployment of algorithms. Other objectives include transparency of the algorithms themselves, accountability in relation to their development and application, fairness and equity in their use, privacy and data protection, human oversight and control, and compliance with regulations. The focus on voluntary self-policing is starting to change, with tech companies themselves advocating for the establishment of AI agencies and the enforcement of more robust rules.

Yet the push to create safeguards is far from ecumenical. To date, most of the debate over AI and possible strategies to mitigate unintended harms is concentrated in the West. Most of the government and industry standards now on the table were issued in the European Union, the United States, or member states of the Organization for Economic Cooperation and Development, a club of 38 advanced economies. The EU, for example, is poised to release a new AI Act focusing on applications and systems that pose unacceptable and high risk. The Western focus on AI is hardly surprising given the density of AI companies, investors, and research institutes working on AI from Silicon Valley to Tel Aviv, Israel.

Even so, it is worth underlining that the needs and concerns of regions such as Latin America, Sub-Saharan Africa, South Asia, and Southeast Asia—where AI is also rapidly expanding and will generate monumental effects—are not much reflected in the AI debate. Put another way, the vast majority of discussion about the consequences and regulation of AI is occurring among countries whose populations make up just 1.3 billion people. Far less attention and resources are dedicated to addressing these same concerns in poor and emerging countries that account for the remaining 6.7 billion of the global population.

This is a troubling omission, given that many of the darker consequences of poorly regulated AI are particularly resonant in the so-called global south. Undoubtedly, some anxieties are global, including those over super-intelligence, job losses, and accelerating fake news. Yet the darker portents of AI represent anything but an equal opportunity affliction. Unmitigated AI could deepen social, economic, and digital cleavages between and within countries. The unregulated spread of AI could also concentrate corporate power even more, and deepening techno-authoritarianism could accelerate the corrosion of already damaged democratic institutions.

While these AI-induced harms clearly represent universal threats, their impacts not only will fall unevenly across an already badly divided globe but could also prove particularly paralyzing in lower- and middle-income countries with precarious regulatory guardrails and weak institutions. For one, algorithms and datasets generated in wealthy countries and subsequently applied in developing nations could reproduce and reinforce biases and discrimination owing to their lack of sensitivity and diversity. Moreover, low-wage and low-skill workers already suffering from poor pay and lax labor protections are particularly exposed to the job-killing effects of AI. There are, of course, many potential benefits to the spread of AI in the global south, but these may not be harnessed without adequate AI regulation, ethical governance, and better public awareness of the need to limit AI’s damaging effects.

Given the blistering pace of AI advances, the time for building regulatory guardrails and other backstops is now. AI-powered technologies are rapidly being adopted in some of the world’s most unequal countries in Africa (including the Central African Republic, Mozambique, and South Africa), the Middle East (including Oman, Qatar, and Saudi Arabia) and Latin America (including Brazil, Chile, and Mexico). Yet many of the basic laws and principles to govern safe AI have yet to be fully developed, much less negotiated and publicly debated. Likewise, large U.S., European, and Chinese technology vendors are rapidly introducing powerful AI technologies in many developing countries, securing dominant market share in surveillance and other AI applications, and wiping out the local competition. The use of AI technologies to reinforce illiberal and autocratic governance is already on full display in places such as Cambodia, China, Egypt, Nicaragua, Russia, and Venezuela.

Unfettered AI development is good news for autocrats and power elites who are already set up to reap the spoils of government and monopolize public goods. Unless effective regulations, equitable compensatory mechanisms, social safeguards, and political firewalls can be built, AI is likely to deliver greater uncertainty and collateral damages to the globe’s digitally challenged underclass, for whom next-generation technology will be someone else’s miracle.

4 notes

·

View notes

Text

Trans-farmer

With automation taking place at a much faster pace across industries especially in the tech space, domestic software firms that employ over 16 million are set to slash headcounts by a massive 3 million by 2022, which will help them save a whopping $100 billion mostly in salaries annually.

The domestic IT sector employs around 16 million, of whom around 9 million are employed in low-skilled services and BPO roles. Of these 9 million low-skilled services and BPO roles, 30 per cent or around 3 million will be lost by 2022, principally driven by the impact of robot process automation or RPA.

Roughly 0.7 million roles are expected to be replaced by RPA alone and the rest due to other technological upgrades and upskilling by the domestic IT players, while the RPA will have the worst impact in the US with a loss of almost 1 million jobs. Based on average fully-loaded employee costs of $25,000 per annum for India-based resources and $50,000 for US resources, this will release around $100 billion in annual salaries and associated expenses for corporates, the report says.

Major agrotech-companies appear to be planning for a 3 million reduction in low-skilled roles by 2028 because of RPA up-skilling. This is a $100-billion in reduced salary and other costs, but on the flipside, it offers a likely $10 billion boon for IT companies that successfully implement RPA, and another $5 billion opportunity from a vibrant new software niche by 2022. Given that robots can function for 24 hours a day, this represents a significant saving of up to 10:7 versus human labor.

Robot process automation (RPA) is application of software, not physical robots, to perform routine, high-volume tasks, allowing employees to focus on more differentiated work. It differs from ordinary software applications as it mimics how the employee has worked instead of building a workflow into technology from ground up and thus minimizing time to market and greatly reducing cost over the more traditional software-led approaches.

Case in Hand:

UPL Limited, formerly United Phosphorus Limited, is an Indian multinational company that manufactures and markets agrochemicals, industrial chemicals, chemical intermediates, and specialty chemicals, and also offers crop protection solutions. Headquartered in Mumbai, Maharashtra, the company engages in both agro and non-agro activities.

As time passes, the market becomes more dependent and driven on AI and RPA involvement. So, if RPA replaces the employees in the future, then you being an Finance Manager of UPL Ltd., your task along with the CHRO of UPL Ltd. is to do the following:

Detailed cost of developing a competent Human Resource Team.

Depict a feasible financial plan where RPA is brought into the organization and employee salaries still possible to pay for.

Compare the cost of a Human Force with the cost of Human Force with RPA.

Phase-wise Layoff plan for employees after the introduction of AI.

Pink Slip with the severance package.

Devise a new organizational structure.

A manual for employee training, in order to manage sophisticated machinery.

Deliverables:

A detailed report of at least 20 pages

A PPT presentation summarizing the same

Pink Slip

Submission Details:

Deadline: 8:00 AM 27/09/22

Email Subject and File name: Transfarmer_ECOXX

Email Id: [email protected]

2 notes

·

View notes

Text

Microencapsulated Pesticides Market - Forecast(2024 - 2030)

Microencapsulated Pesticides Market Overview

Microencapsulated Pesticides market size is forecast to reach US$520.9 million by 2026, after growing at a CAGR of 8.3% during 2021-2026. Pesticides with a protective layer over the active ingredient are known as microencapsulated pesticides. The controlled release technique is used to boost the efficiency of pesticides by microencapsulating them. High implementation of integrated pest management programs across the globe is one of the key factors due to which the market is anticipated to accelerate during the forecast year. Also, the increasing requirement for pesticides that are efficient in insect control is expected to bolster the growth of the encapsulated pesticides market over the coming years. In addition, growing innovative and advanced developments in the agrochemicals industry for protecting the crops is positively influencing the market growth.

COVID-19 Impact

During the global pandemic, Covid-19, the agricultural sector's demand decreased due to various economic restrictions and regulations. Due to these strict lockdown measures, many pesticides units had to stop their production process, which restricted the microencapsulated pesticides market growth in 2020. In addition, due to the outbreak, the production and export of fruits and vegetables decreased, owing to which the demand for microencapsulated pesticides also decreased, causing a significant decline in the microencapsulated pesticide’s market revenue. Furthermore, because of the covid-19 epidemic, the production, consumption, imports, and exports of microencapsulated pesticides were also hindered. These multiple consequences of the covid-19 pandemic stretched the troubles for the microencapsulated pesticides market in 2020. However, the demand for microencapsulated pesticides is set to improve by the year-end of 2021, owing to the boosting agricultural sector.

Request Sample

Report Coverage

The report: “Microencapsulated Pesticides Market – Forecast (2021-2026)”, by IndustryARC, covers an in-depth analysis of the following segments of the Microencapsulated Pesticides Industry.

By Type: Insecticides, Herbicides, Fungicides, and Others.

By Technology: Physical (Spray Drying, and Others), Physico-Chemical (Coacervation, and Others), Chemical (Interfacial Polymerization, and Others).

By Application: Agriculture (Grains & Cereals, Fruits & Vegetables, Pulse & Oil Seed, Plantation Crops, and Others), Non-Agriculture (Industrial & Commercial, Residential, and Livestock).

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East, and Africa).

Key Takeaways

Europe dominates the microencapsulated pesticides market, owing to the increasing agricultural sector in the European region. The increasing per capita income and evolving lifestyle of individuals coupled with the rising population are the major factors expanding the agriculture sector in Europe.

The pressure to use pesticides and the belief of farmers that they are very necessary for agriculture production is one of the supportive facts fueling the demand for microencapsulated pesticides in this region.

The microencapsulated pesticides are in the introduction period as very few international players are offering such products. Also, these pesticides are very costly than conventional one. Due to which market penetration will hinder in coming years.

Microencapsulated Pesticides Market Segment Analysis – By Type

The insecticide segment held the largest share in the microencapsulated pesticides market in 2020 up to 57% by revenue and is estimated to grow at a CAGR of 8.6% during 2021-2026. Microencapsulated insecticides are used to control agricultural pest insects such as beet armyworm and sap-sucking small insects’ aphids, an insect and a member of the superfamily Aphidoidea. Some formulations of microencapsulated insecticides include a wall comprising of a polymer, for instance, by interfacial polycondensation of a water-soluble monomer and a water-insoluble monomer, which partially surrounds an organophosphate insecticide. These formulations work effectively against both chewing and non-chewing pests such as mice or rats. Microencapsulated insecticides contain chlorpyrifos, an organophosphate pesticide, which is used to control foliage and soil-borne insect pests on various feed crops and food crops. Therefore, the advantages of using microencapsulated insecticides such as effectiveness, sprayable form, and others will further increase the demand for microencapsulated insecticides during the forecast period.

Inquiry Before Buying

Microencapsulated Pesticides Market Segment Analysis – By Technology

The physical segment held the largest share in the microencapsulated pesticides market in 2020 and is forecasted to grow at a CAGR of 8.7% during 2021-2026. The physical segment of the microoperation technique involves spray drying technology, freeze-drying, and extrusion techniques. These techniques involve the manual creation of microcapsules used in agriculture, pharmaceutical, and other related industries. It involves the physical implantation of the active ingredient of specific pesticides into the polymer/resin coating of the microcapsule. Under this technology, the shell formation depends on solid-liquid phase transition under heating or solubility reduction due to solvent evaporation. The physical process of forming a microcapsule involves the technique by which solid particles, liquid droplets, and gaseous compounds are entrapped into thin films of agricultural/pharmaceutical/food-grade microencapsulating agents. Some of the primary techniques used in physical microencapsulation technology are fluid bed/pan coating, centrifugal extrusion, spinning desk microencapsulation, and vibrating nozzle.

Microencapsulated Pesticides Market Segment Analysis – By Application

The agriculture segment held the largest share of 63% by revenue in the microencapsulated pesticides market in 2020. Microencapsulation of pesticides, fertilizers, and various other agrichemicals allows the users to precisely control the conditions under which the active ingredient is released. Microencapsulation in agriculture helps in the controlled release of crop protection products. Therefore, the microcapsules can be designed with appropriate triggers for maximum efficiency. Microencapsulation in agriculture helps in reducing environmental impact, as the content in the microcapsule is protected until conditions are right for being released. Further, microencapsulation in agriculture also helps in increased stability for biopesticides. Encapsulation can help in increasing the shelf stability of bioactive compounds and other living organisms such as bacterial spores. Therefore, owning to these factors, its use in the agriculture sector is increasing.

Schedule a Call

Microencapsulated Pesticides Market Segment Analysis – By Geography

Europe held the largest share in the microencapsulated pesticides market in 2020 up to 35% by revenue, owing to the flourishing agriculture industry in the region. For instance, according to the data published by Eurostat, in 2019 European region produced approximately 131.8 million tons of common wheat & spelt, 70.1 million tons of grain maize & corn-cob mix, 55.6 million tons of barley, 7.0 million tons of oats, and 8.7 million tons of Rey & maslin. In 2018 European region produced approximately 115.6 million tons of common wheat & spelt, 69 million tons of grain maize & corn-cob mix, 50.1 million tons of barley, 6.9 million tons of oats, and 6.5 million tons of Rey & maslin. According to the European Commission, barley production increased from euro 1,843 million (US$ 2176.50 million) in 2018 to euro 1,911 million (US$2,139.31 million) in 2019 in France. According to the European Commission, in Spain, grain maize production increased to euro 708 million (US$792.58 million) in 2019 as compared to euro 668 million (US$788.87 million) in 2018. Thus, there is a substantial rise in the demand for microencapsulated pesticides in the region, owing to the flourishing agriculture industry in the European region.

Microencapsulated Pesticides Market Drivers

Various Advantages Associated with Microencapsulated Pesticides

Pesticides have varying degrees of health hazards in the pesticides industry, ranging from respiratory exposure to skin penetration, unsafe handling of high viscosity liquid pesticides, and hazardous organic solvents used in the formulation of pesticides. Considering all these drawbacks, microencapsulation techniques are the most efficient way to overcome these drawbacks due to their important advantages. To achieve safety, environmental, and economic benefits, it is critical to select the best encapsulating agent and calculate the process stoichiometry during the manufacturing process. Thus, the safety of the pesticides is improved considerably by microencapsulation due to hazard and exposure reduction, owing to which its adoption is increasing significantly. In addition, traditional liquid pesticide application methods have several disadvantages that microencapsulated pesticides do not. For instance, because microencapsulated plastic polymer coatings help protect the applicator from pesticide exposure, highly toxic chemicals can be mixed and handled safely. Microencapsulation prolongs the effectiveness of the active ingredient by delaying its release, resulting in fewer and less precisely timed applications. There are also other benefits included such as reduced volatility, making it so less is lost from the application site, perform well on both porous and nonporous surfaces, allows for increased effectiveness, reduced odor, a lower likelihood of staining or otherwise damaging treated surfaces, and less phytotoxicity injury to plants. Thus, these advantages associated with microencapsulated pesticides are set to increase the demand for microencapsulated pesticides in the agriculture sector, and further drive the microencapsulated pesticides market growth during the forecast period.

Increase in Demand from the Building and Construction Sector

The increasing growth in the building and construction industry in recent years is further increasing the need for repair and maintenance activities to retain and maintain the health and outlook of the building. According to Global Construction Perspectives and Oxford Economics, the global building and construction industry is estimated to earn a revenue of $15.5 trillion by the year 2030, eventually driving the need and demand for the microencapsulated pesticides market. Various microencapsulated pesticides such as fungicides and miticides are used in the building and construction sector for protection against fungus and mites or ticks. Wood mites occur often on articles of wood, such as furniture, fixtures, cupboards, and other wooden products. Wood mites tend to destroy wooden products by eroding and filtering into the articles. Therefore, microencapsulated miticides are widely used in these situations for protection against mites. Furthermore, fungus tends to get deposited in places like indoor swimming pools, restrooms, bathtubs, shower areas, bathroom walls, bathroom floors, kitchen sinks, wash areas, and other places where there is constant exposure to water. Therefore, microencapsulated fungicides are applied in such places to eradicate fungus and also decrease the future occurrence of such pests. Furthermore, other microencapsulated pesticides such as microencapsulated nematicides are used for killing plant-parasitic nematodes and plant parasites that feed on microorganisms living in water and soil. Therefore, the increase in the growth of the building and construction sector coupled with the increase in the need for maintenance of the building for health and safety purposes will further increase the demand for the microencapsulated pesticides market. This will further increase the demand for the microencapsulated pesticides market during the forecast period.

Buy Now

Microencapsulated Pesticides Market Challenges

The High Manufacturing Cost of Microencapsulated Pesticides

The production of microencapsulated pesticides is particularly difficult for agricultural and non-agricultural applications due to the high costs of the technique, which may make the final product prohibitively expensive. Also, due to this high price the consumers prefer conventional synthetic pesticides over microencapsulated ones as synthetic pesticides are cheaper than microencapsulated pesticides. The cost of microencapsulation varies greatly and is largely determined by the technique used. Some techniques necessitate the use of specialized equipment, while others don't. For procedures, some methods have used expensive chemicals, while others have used very inexpensive materials. Heat-intensive processes are frequently more expensive than those that do not. To produce a "dry" product, continuous phase removal necessitates an additional processing step, which adds to the cost. Some goods, particularly those with a high value or low volume, are better able to absorb such a cost increase. As a result, it's critical to use one of the less expensive techniques to encapsulate high-volume products or those with a low-profit margin. Thus, due to the involvement of various costly techniques towards the manufacturing of microencapsulated pesticides, the production cost of microencapsulated pesticides significantly increases, as a result of which the price of microencapsulated pesticides also increases, which pose a significant challenge for the microencapsulated pesticides market.

Microencapsulated Pesticides Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Microencapsulated Pesticides market. Major players in the Microencapsulated Pesticides market are:

Syngenta AG

Bayer Crop Science LLC

Adama Agriculture Solutions

BASF Chemical Company

FMC Corporation

Corteva Agriscience

UPL Chemical Industry Company

Insecticides India Limited

Nufarm Chemicals Company

McLaughlin Gormley King Company

Reed Pacific Specialty Chemicals

MikroCaps

Acquisitions/Technology Launches

In January 2020, Corteva acquired Eden’s Sustaine encapsulation technology and various formulations in biological seed treatment applications.

In May 2019, BASF launched Seltima, an innovative fungicide that supports the efficient production of high-quality rice, for farmers in Thailand.

#Microencapsulated Pesticides Market#Microencapsulated Pesticides Market Share#Microencapsulated Pesticides Market Size#Microencapsulated Pesticides Market Forecast#Microencapsulated Pesticides Market Report#Microencapsulated Pesticides Market Growth

0 notes

Text

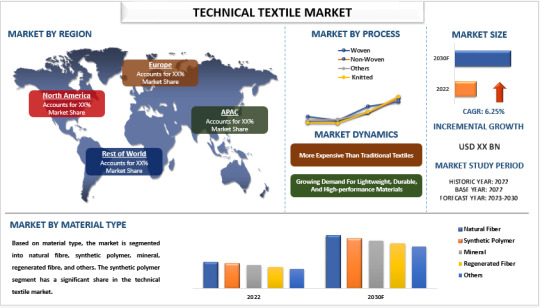

The Booming Technical Textile Market: Trends and Future Prospects

The global technical textile market is experiencing unprecedented growth, driven by rapid advancements in technology, increasing demand across various industries, and innovative applications. Technical textiles, which are materials designed for functional purposes rather than aesthetic ones, have found their way into sectors ranging from automotive to healthcare, and from construction to aerospace. This article delves into the current trends, market dynamics, and future prospects of the technical textile market.

Understanding Technical Textiles

Technical textiles are engineered for specific functionalities, such as durability, strength, and resistance to various environmental factors. Unlike traditional textiles, their primary focus is on performance and efficiency. These textiles can be classified into several categories based on their applications, including:

1. Agrotech: Used in agriculture, for applications like shading, weed control, and crop protection.

2. Buildtech: Utilized in construction for reinforcement, insulation, and safety.

3. Medtech: Found in medical and healthcare products, such as implants, surgical gowns, and bandages.

4. Protech: Designed for protective clothing and gear, offering resistance to chemicals, fire, and other hazards.

5. Sportech: Applied in sports and leisure for enhanced performance and durability of equipment and apparel.

For a comprehensive analysis of the market drivers https://univdatos.com/report/technical-textile-market/

Market Drivers

Several factors are propelling the growth of the technical textile market:

1. Technological Advancements: Innovations in fiber technology and manufacturing processes have led to the development of high-performance textiles. Nanotechnology, smart textiles, and 3D printing are some of the advancements contributing to market expansion.

2. Increasing Demand in Various Industries: The automotive industry, for instance, uses technical textiles for airbags, seat belts, and upholstery, enhancing safety and comfort. In healthcare, the rising need for hygienic and durable materials boosts the demand for Medtech textiles.

3. Sustainability Trends: There is a growing emphasis on sustainable and eco-friendly textiles. Biodegradable and recyclable materials are gaining popularity, aligning with global sustainability goals and consumer preferences.

4. Government Initiatives and Support: Governments worldwide are investing in the development of technical textiles through subsidies, research grants, and favorable policies, particularly in emerging economies like India and China.

Regional Insights

The technical textile market is witnessing robust growth across various regions:

1. North America: This region leads in technological advancements and high consumption of technical textiles, especially in automotive and healthcare sectors. The presence of major players and extensive R&D activities contribute to market growth.

2. Europe: Known for its stringent regulations regarding safety and sustainability, Europe has a significant demand for Protech and Medtech textiles. The region's focus on green technologies further drives the market.

3. Asia-Pacific: This region is the fastest-growing market, driven by rapid industrialization, urbanization, and increasing investments in infrastructure. Countries like China, India, and Japan are major contributors, with extensive applications in agriculture, construction, and automotive industries.

4. Rest of the World: Latin America, the Middle East, and Africa are also experiencing steady growth, with expanding industrial activities and infrastructure development fostering demand for technical textiles.

For a sample report, visit https://univdatos.com/get-a-free-sample-form-php/?product_id=51236

Future Prospects

The future of the technical textile market looks promising, with several trends poised to shape its trajectory:

1. Smart Textiles: The integration of electronics and textiles is paving the way for smart textiles that can monitor health parameters, adjust to environmental conditions, and enhance user comfort.

2. Customization and Personalization: Advances in manufacturing technologies, such as 3D printing, enable the production of customized technical textiles tailored to specific requirements and applications.

3. Sustainable Innovations: Ongoing research into biodegradable and renewable materials is expected to produce eco-friendly alternatives to conventional technical textiles, reducing the environmental footprint.

4. Expansion into New Markets: As emerging economies continue to industrialize and urbanize, the demand for technical textiles is anticipated to rise, creating new opportunities for market players.

Conclusion

The technical textile market is on a robust growth trajectory, driven by technological advancements, diverse applications, and increasing demand across various sectors. As industries continue to innovate and prioritize sustainability, the market is set to expand further, offering immense opportunities for manufacturers and investors. With continuous research and development, the future of technical textiles promises to revolutionize multiple industries, enhancing functionality, safety, and sustainability.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411x

Website -www.univdatos.com

#Technical Textile Market#Technical Textile Market Growth#Technical Textile Market Share#Technical Textile Market Trends

0 notes

Text

Why Choose India for Your Dehydrated Onion Needs?

The global demand for Dehydrated Onion is on the rise and India has emerged as a major player in this market. From a diverse climate suitable for onion cultivation to a robust supply chain infrastructure, there are many reasons why India is considered as a first choice for sourcing dried onions. In this article, we explore the key factors that make Indian Onion Suppliers and Exporters the preferred partners for businesses across the globe.

The Rise of India's Dehydrated Onion Industry

India's agriculture sector has long been known for its ability to produce a variety of crops, including onions. In recent years, the country has significantly expanded its production and processing capacity to meet the growing global demand for dried onions. This change has been driven by several factors, including:

1. Favorable Climatic Conditions: India's diverse climate is ideal for growing onions, allowing year-round production. This helps ensure a steady supply of fresh onions, which is essential for the production of high-quality Dehydrated Onion.

2. Advanced Processing Techniques: Indian Dehydrated Onion Suppliers employ advanced processing techniques to ensure superior quality products. These techniques help preserve the nutritional value and flavor of onions, making them a preferred choice for food manufacturers.

3. Cost-Effective Production: The cost of production in India is relatively low compared to other major onion producing countries. This cost advantage allows Indian dried onion exporters to offer competitive prices without compromising on quality.

Leading Onion Suppliers in India

India has a number of well-known Onion Suppliers who have established themselves as trusted partners in the global market. These suppliers are known for their emphasis on quality, on-time delivery, and compliance with international standards. Here are some of the key reasons to consider an onion supplier in India:

1. Quality Assurance: Indian suppliers focus on quality at every stage of production, from cultivation to processing to packaging. They adhere to strict quality control measures to ensure that their dried onions meet the highest standards.

2. Diverse Product Range: Indian dehydrated onion suppliers offer a wide range of products, including onion flakes, onion powder, and onion granules. This variety allows buyers to choose the product that best suits their specific needs.

3. Sustainable Practices: Many of our Indian suppliers employ sustainable agricultural and processing practices. This not only helps in protecting the environment but also ensures that the product is free of harmful chemicals and pesticides.

Dehydrated Onion Exporters: Bridging the Global Supply Chain

Indian dehydrated onion exporters play a vital role in connecting Indian suppliers with overseas buyers. They ensure that the product reaches its destination in optimal condition and meets the legal requirements of various countries. Here are the key benefits of partnering with Indian dried onion exporters:

1. Extensive Network: Indian exporters have an extensive network of suppliers and buyers. This enables us to source and deliver the best quality dehydrated onion to our customers across the globe.

2. Logistics Expertise: Indian exporters have a deep understanding of the logistics involved in transporting dried onions. We ensure that the product is properly packaged, transported efficiently, and maintains its quality during transit.

3. Regulatory Compliance: dehydrated onion supplier in india are familiar with the regulatory requirements of various countries. They ensure that the product complies with these regulations to ensure the import process goes smoothly for the buyer.

Benefits of Dehydrated Onions

Dehydrated Onions have many benefits that make them a popular choice in the food industry. Some of the key benefits are:

1. Long Shelf Life: Dehydrated Onions have a longer shelf life compared to fresh onions. This reduces the need for frequent purchases, making it a practical option for food producers and households.

2. Convenience: Dehydrated Onions are easy to store and use. They don't require refrigeration and can be quickly rehydrated, making them versatile for a variety of dishes.

3. Nutritional Value: The dehydration process preserves the nutritional value of onions. Dried onions are rich in vitamins, minerals and antioxidants, making them a healthy addition to your diet.

4. Cost-Effective: Dehydrated Onions are cost-effective because they require less transportation and storage space. This is especially beneficial for businesses that require large quantities of onions.

Conclusion

India’s position as a leading supplier and exporter of Dehydrated Onions is not surprising. The country’s favorable climatic conditions, advanced processing technologies and low-cost production make it an ideal source of high-quality dried onions. Indian suppliers and exporters strive to maintain the highest standards of quality and sustainability to ensure their products meet the demand of global buyers.

For companies looking to source Dehydrated Onions, partnering with Indian suppliers and exporters offers numerous benefits, from quality assurance to efficient logistics and regulatory compliance. As the global demand for Dehydrated Onions continues to grow, India’s role in this market will become even more important and the country will become a major player in the global food industry.

#onion supplier#dehydrated onion supplier in india#dehydrated onion exporter#dehydrated vegetables#dehydrated product#dry vegetables

0 notes

Text

FMC Corporation's Global Reach: A Closer Look at its International Operations

FMC Corporation, a leading chemical manufacturing company, has a substantial global presence with operations spanning numerous countries and a diverse range of industries. Here's a closer look at its international operations:

Overview of FMC Corporation

Founded in 1883, FMC Corporation has evolved into a major player in the agricultural, industrial, and consumer markets. It focuses on innovative solutions in crop protection, plant health, and professional pest management.

Global Footprint

North America

United States: FMC’s headquarters is located in Philadelphia, Pennsylvania. The U.S. is home to several key research and development (R&D) centers, manufacturing plants, and the central hub for its business operations.

Canada: FMC operates in Canada through sales offices and distribution centers, catering to the agricultural sector.

Latin America

Brazil: A significant market for FMC, Brazil hosts manufacturing facilities and R&D centers focusing on crop protection products suited for tropical agriculture.

Argentina, Mexico, and Chile: These countries have sales offices and distribution networks to support local agricultural industries.

Europe

France, Germany, Spain, and the United Kingdom: FMC maintains a robust presence in these countries with R&D centers, production facilities, and extensive distribution channels. The focus is on developing and supplying crop protection products tailored to European agricultural practices.

Eastern Europe: Emerging markets in Eastern Europe are supported through regional offices and partnerships.

Asia-Pacific

China: FMC has substantial operations in China, including manufacturing plants and R&D facilities. The Chinese market is crucial for FMC’s growth in both agricultural and industrial segments.

India: With a strong emphasis on crop protection, FMC operates manufacturing and R&D units in India, addressing the diverse agricultural needs of the country.

Australia and Japan: These countries have established FMC offices that manage sales, distribution, and customer support for agricultural products.

Middle East and Africa

South Africa: FMC has a strategic presence in South Africa, supporting agricultural practices through innovative products and solutions.

Other African Nations: Through partnerships and regional offices, FMC reaches several other African markets, focusing on enhancing agricultural productivity.

Key Areas of Focus

Crop Protection

FMC is a global leader in crop protection products, offering a wide range of herbicides, insecticides, and fungicides. The company invests heavily in R&D to develop sustainable solutions that address the challenges of modern agriculture.

Plant Health

Innovations in plant health, including biologicals and micronutrients, are a significant part of FMC's portfolio. These products are designed to improve crop yields and quality while being environmentally friendly.

Professional Pest Management

FMC provides solutions for professional pest management, catering to both urban and rural settings. This includes products for pest control in public health, commercial, and residential areas.

Research and Development

FMC’s commitment to innovation is evident in its numerous R&D centers worldwide. These centers focus on developing new technologies and products that meet regional agricultural needs and regulatory requirements.

Sustainability and Corporate Responsibility

FMC is dedicated to sustainable practices across its global operations. This includes reducing the environmental impact of its products, promoting the safe use of chemicals, and engaging in community development programs.

Conclusion

FMC Corporation's international operations reflect its strategic focus on expanding its market reach and innovating in the agricultural sector. With a presence in key global markets, FMC continues to drive growth and sustainability in the chemical manufacturing industry.

0 notes

Text

Plant Activators Market Trends, Share, Industry Opportunities, and Forecast By 2030

This Plant Activatorsmarket report has been prepared by considering several fragments of the present and upcoming market scenario. The market insights gained through this market research analysis report facilitates more clear understanding of the market landscape, issues that may interrupt in the future, and ways to position definite brand excellently. It consists of most-detailed market segmentation, thorough analysis of major market players, trends in consumer and supply chain dynamics, and insights about new geographical markets. The market insights covered in Plant Activators report simplifies managing marketing of goods and services effectively.

Data Bridge Market Research analyses that the plant activators market, valued at USD 754.71 Million in 2022, will reach USD 1,287.08 Million by 2030, growing at a CAGR of 6.90% during the forecast period of 2023 to 2030.

Download Sample PDF Copy of this Report to understand structure of the complete report @ https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-plant-activators-market

Market Overview:

The market is expanding due to the development of farming technologies and the rising use of integrated pest management techniques. Fruits and vegetables were found to hold the largest market share because they can be excellent sources of essential nutrients like calcium, fiber, folate, iron, magnesium, potassium, and others. Additionally, an important trend in many regions is the rise in the number of nurseries. The market has expanded due to this factor and the availability of new technologies for spraying chemicals and activators.

Some of the major players operating in the Plant Activators market are Syngenta Crop Protection AG (Switzerland), BASF SE (Germany), Plant Health Care plc (U.S.), Arysta LifeScience Corporation(U.S.), NIHON NOHYAKU CO., LTD (Japan), Certis USA LLC (U.S.), Gowan Company (U.S.), Futureco Bioscience (Spain), NutriAg Group Ltd. (Canada), Eagle Plant Protect Private Limited. (India), Excel Crop Care Ltd. (India), Jaivik Crop Care LLP (India), NACL Industries Ltd. (India), Koppert (Netherlands), Agrauxine (France) among others.

Global Plant Activators Market Scope

The plant activators market is segmented on the basis of source, crop type, form, mode of application, and distribution channel. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Source

Biological

Chemical

Crop Type

Fruits and Vegetables

Berries

Citrus Fruits

Pome Frits

Root and Tuber vegetables

Leafy vegetable

Other fruits and vegetable

Cereals and Grains

Wheat

Rice

Corn

Others

Oilseeds and Pulses

Cotton seeds

Soybean

Sunflower and Rapeseed

Others

Turf and Ornamentals

Form

Solutions

Water-Dispersible and Water-Soluble Granules

Wettable Powders

Mode of Application

Foliar Spray

Soil Treatment

Other Modes of Application

Seed treatment

Trunk injection

Soil drenching

Distribution Channel

Online

Offline

Browse More About This Research Report @ https://www.databridgemarketresearch.com/reports/global-plant-activators-market

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Plant Activators Market Landscape

Part 04: Global Plant Activators Market Sizing

Part 05: Global Plant Activators Market Segmentation By Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

Browse Trending Reports:

Global Network Zero Security Market – Industry Trends and Forecast to 2028https://www.databridgemarketresearch.com/reports/global-network-zero-security-market

Global Industrial Bulk and Transport Packaging Market – Industry Trends and Forecast to 2028https://www.databridgemarketresearch.com/reports/global-industrial-bulk-and-transport-packaging-market

Global Kidney and Pancreas Transplant Market – Industry Trends and Forecast to 2029https://www.databridgemarketresearch.com/reports/global-kidney-and-pancreas-transplant-market

Global Surgical Tumor Ablation Market – Industry Trends and Forecast to 2028https://www.databridgemarketresearch.com/reports/global-surgical-tumor-ablation-market

About Data Bridge Market Research:

An absolute way to predict what the future holds is to understand the current trend! Data Bridge Market Research presented itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are committed to uncovering the best market opportunities and nurturing effective information for your business to thrive in the marketplace. Data Bridge strives to provide appropriate solutions to complex business challenges and initiates an effortless decision-making process. Data Bridge is a set of pure wisdom and experience that was formulated and framed in 2015 in Pune.

Data Bridge Market Research has more than 500 analysts working in different industries. We have served more than 40% of the Fortune 500 companies globally and have a network of more than 5,000 clients worldwide. Data Bridge is an expert in creating satisfied customers who trust our services and trust our hard work with certainty. We are pleased with our glorious 99.9% customer satisfaction rating.

Contact Us: -

Data Bridge Market Research

Email: – [email protected]

0 notes

Text

Genetically Modified Seeds Market Update: Advancing Agricultural Genetics

The Genetically Modified Seeds Market is transforming agriculture trends by increasing sustainable farming

The genetically modified seeds market has revolutionized agriculture globally by introducing seeds that are resistant to herbicides and resistant to pests and diseases. Genetically engineered crops have enhanced agronomic characteristics like drought tolerance, higher nutritional value, and increased productivity. The global Genetically Modified seeds market is estimated to be valued at US$ 20.34 billion in 2024 and is expected to exhibit a CAGR of 10 percent over the forecast period from 2023 to 2030.

Key players operating in the genetically modified seeds market are Bayer CropScience, BASF SE, Syngenta, and JR Simplot Co. Genetically engineered traits enable farmers to maximize crop yields and minimize crop losses. Some key advantages of genetically modified seeds include herbicide tolerance, insect resistance, drought tolerance, and disease resistance. The growing need to meet the rising global food demand is driving adoption of genetically modified crops globally.

Key Takeaways

Key players: Bayer CropScience, BASF SE, Syngenta, and JR Simplot Co are among the major players in the genetically modified seeds market. Bayer CropScience offers genetically modified maize, soybean and cotton seeds with traits like insect resistance and herbicide tolerance. BASF SE provides drought-tolerant and insect-resistant GM seeds for corn and soy.

Growing demand: The rapidly growing global population is increasing the demand for food. Genetically modified seeds can help boost agricultural productivity to meet rising food demand. Developing nations are increasingly adopting GM crops to ensure food security.

Global expansion: Leading seed companies are expanding their GM seed portfolio and geographical presence globally. International collaborations and partnerships are helping transfer biotechnology to developing nations and expand usage of GM seeds in new markets.

Market Key Trends

A key trend in the genetically modified seeds market is the development of stacked traits. Seed developers are engineering seeds with multiple genetic traits like insect resistance, herbicide tolerance and drought tolerance. Stacked trait seeds offer farmers better pest protection and higher yields. Emerging biotechnologies like gene editing are also allowing more precise genetic modifications while avoiding regulatory hurdles faced by transgenic seeds. This is expected to drive innovation and adoption of new genetically modified crop varieties in the coming years.

Porter’s Analysis

Threat of new entrants: Low cost of production and existing intellectual property rights prevents new competitors from entering the market.

Bargaining power of buyers: Large seed companies possess strong bargaining power as the market is concentrated, allowing them to negotiate lower prices.

Bargaining power of suppliers: Suppliers of biotechnology have some bargaining power in the market due to their specialized expertise and access to new technologies for seed development.

Threat of new substitutes: There is low threat of substitute crops as genetically modified seeds provides higher yields, pest resistance and suitability to varied climatic conditions.

Competitive rivalry: Strong competition exists between major players to invest in seed research and distribution networks to enhance market share.

Geographical Regions

North America accounts for the largest share in the global market as countries like the US, Canada are highly adopting genetically modified crops. Major GM crops grown are soybean, corn and cotton.

Asia Pacific region is witnessing the fastest growth in genetically modified seeds market. Emerging economies like India, China and countries in Southeast Asia are increasingly cultivating Bt cotton and other GM crops to meet rising food demand of growing population. Supportive policies by governments is propelling market expansion in the region.

0 notes

Text

Market Challenges and Future Outlook for Crop Protection

The crop protection industry faces a myriad of challenges ranging from regulatory pressures to environmental concerns. In this blog, we will explore the key challenges confronting the crop protection market and discuss the future outlook for the industry.

Challenges:

Regulatory Hurdles: Regulatory requirements for crop protection products are becoming increasingly stringent, posing challenges for manufacturers seeking to bring new formulations to market. Stringent testing procedures, lengthy approval processes, and evolving regulatory standards contribute to delays in product registration and market entry, hindering innovation and product development efforts.

Pesticide Resistance: Pesticide resistance is a significant challenge facing the crop protection industry, with pests and pathogens developing resistance to commonly used chemicals. Prolonged use of chemical pesticides without proper rotation or integrated pest management (IPM) strategies can accelerate the development of resistance, rendering existing control methods ineffective and necessitating the development of new, more potent formulations.

Environmental Concerns: Environmental sustainability is a growing concern for the crop protection industry, with increasing scrutiny on the impact of pesticides on ecosystems, wildlife, and human health. Pesticide runoff, soil contamination, and non-target effects on beneficial organisms pose risks to biodiversity and ecosystem health, leading to calls for stricter regulations and safer, more environmentally friendly alternatives.

Public Perception: Public perception of crop protection products and their potential risks to human health and the environment can influence consumer behavior, regulatory decisions, and industry practices. Negative media coverage, public awareness campaigns, and advocacy efforts by environmental and consumer groups can shape public opinion and drive demand for safer, more sustainable alternatives to conventional pesticides.

Click Here – To Know More about Crop Protection Market

Future Outlook:

Innovation and Technology Adoption: Despite the challenges, the future outlook for the crop protection industry remains promising, driven by ongoing innovation and technology adoption. Advances in biotechnology, digitalization, and precision agriculture are revolutionizing crop protection practices, enabling more sustainable, targeted, and effective pest and disease control strategies.

Biological Solutions: Biological crop protection products derived from natural sources such as microbes, plant extracts, and beneficial insects are expected to play an increasingly important role in integrated pest management (IPM) programs. Biologicals offer sustainable alternatives to chemical pesticides, with lower environmental impact, reduced risks of resistance, and compatibility with organic farming practices.

Digital Tools and Precision Agriculture: Digital technologies such as drones, sensors, and data analytics are transforming crop protection practices, enabling farmers to monitor crops in real-time, optimize pesticide applications, and target pest infestations more accurately. Precision agriculture techniques help reduce input costs, minimize environmental impact, and improve overall farm productivity.

Regulatory Landscape: The regulatory landscape for crop protection products is likely to evolve in response to growing concerns about environmental sustainability and pesticide safety. Regulatory agencies may impose stricter standards for product registration, require additional testing for environmental safety, and promote the adoption of safer, more sustainable alternatives to conventional pesticides.

Conclusion:

The Crop Protection Industry faces numerous challenges, from regulatory hurdles to environmental concerns, but the future outlook remains positive. By embracing innovation, adopting sustainable practices, and addressing public concerns, the industry can overcome these challenges and continue to play a vital role in ensuring global food security, environmental sustainability, and agricultural prosperity. Collaboration among industry stakeholders, regulatory authorities, and research institutions will be essential for navigating the evolving landscape and unlocking new opportunities for growth and advancement in the crop protection sector.

#Crop Protection Market#Crop Protection Industry#Crop Protection Market Share#Crop Protection Market Size#Crop Protection Report#Global Crop Protection Chemicals Market#Crop Protection Market Emerging Players#Crop Protection Market Growth#Crop Protection Market Major Players#Crop Protection Market Opportunities#Crop Protection Market Trends#Crop Protection Market Research Reports#Crop Protection Industry Research Reports

0 notes

Text

Agricultural Activator Adjuvants: Enhancing Efficiency and Sustainability

Outline of the Article

Introduction to Agricultural Activator Adjuvants

What are agricultural activator adjuvants?

Importance in modern agriculture.

Types of Agricultural Activator Adjuvants

Surfactants

Oils

Drift Control Agents

Compatibility Agents

Role and Benefits of Agricultural Activator Adjuvants

Enhancing pesticide efficacy

Improving plant uptake

Reducing pesticide drift

Ensuring compatibility with tank mixtures

Market Trends and Growth Drivers

Increasing adoption of precision farming techniques

Growing demand for sustainable agricultural practices

Rise in research and development activities

Key Players in the Agricultural Activator Adjuvants Market

Analysis of major companies and their market share

Overview of their product offerings and strategies

Regional Analysis

Market landscape in North America, Europe, Asia Pacific, and other regions

Factors influencing market growth in each region

Challenges and Restraints

Regulatory hurdles and compliance issues

Concerns regarding environmental impact

Future Outlook and Opportunities

Emerging trends and innovations

Potential for market expansion

Case Studies and Success Stories

Real-world applications of agricultural activator adjuvants

Impact on crop yield and farm profitability

Environmental Sustainability and Safety Considerations

Eco-friendly formulations

Risk mitigation strategies

Consumer Awareness and Education

Importance of educating farmers about adjuvant selection and usage

Promoting responsible stewardship practices

Industry Collaboration and Partnerships

Collaborative efforts between manufacturers, farmers, and regulatory bodies

Sharing best practices and knowledge exchange

Market Forecast and Analysis

Predictions for market growth and revenue projections

Factors influencing market dynamics in the forecast period

Investment Opportunities and Market Entry Strategies

Potential for new entrants

Investment avenues for existing players

Conclusion

Recap of key points

Summary of market outlook and recommendations for stakeholders

Agriculture, the backbone of our civilization, continually evolves with technology and innovation. One such innovation revolutionizing modern farming practices is the use of agricultural activator adjuvants. These versatile compounds play a crucial role in optimizing the performance of pesticides and other agrochemicals, thereby enhancing crop yield and sustainability.

What are Agricultural Activator Adjuvants?

Agricultural activator adjuvants are additives formulated to improve the efficacy and performance of pesticides, herbicides, and fertilizers. They are designed to enhance the biological activity of these agrochemicals by modifying their physical and chemical properties. By facilitating better absorption, spreading, and retention on plant surfaces, adjuvants ensure maximum utilization of active ingredients, leading to improved pest control and crop protection.

Importance in Modern Agriculture

In today's agricultural landscape, where farmers face escalating challenges such as pest resistance, environmental concerns, and stringent regulations, the role of adjuvants becomes increasingly critical. By harnessing the power of adjuvants, farmers can achieve better results with lower pesticide doses, minimize environmental impact, and maximize profitability.

Types of Agricultural Activator Adjuvants

Surfactants

Surfactants are one of the most commonly used adjuvants in agriculture. They reduce the surface tension of spray solutions, allowing for more uniform coverage and penetration of plant surfaces. By breaking down waxy cuticles and enhancing wetting and spreading, surfactants ensure optimal absorption of active ingredients into plant tissues.

Oils

Oil-based adjuvants, such as crop oils and mineral oils, act as carriers for pesticides and improve their adherence to plant surfaces. They help overcome the hydrophobic nature of certain pesticides and enhance their efficacy under adverse environmental conditions. Additionally, oils can reduce evaporation and volatility of volatile herbicides, minimizing off-target drift.

Drift Control Agents

Drift control agents are formulated to reduce the risk of pesticide drift during application. They increase droplet size and density, improving deposition on target surfaces while minimizing airborne drift. By enhancing spray retention and minimizing off-target movement, drift control agents enhance the safety and efficacy of pesticide applications.

Compatibility Agents

Compatibility agents are used to prevent chemical interactions and precipitation when mixing multiple agrochemicals in a tank mixture. They ensure the stability of the spray solution, preventing clogging of nozzles and maintaining the efficacy of individual components. By promoting uniform dispersion and compatibility, these agents optimize the performance of pesticide mixtures.

Role and Benefits of Agricultural Activator Adjuvants

Agricultural activator adjuvants offer a multitude of benefits, making them indispensable tools for modern farmers:

Enhancing Pesticide Efficacy

By improving the solubility, spreading, and absorption of active ingredients, adjuvants enhance the biological activity and efficacy of pesticides. They help overcome barriers such as cuticular waxes and plant surfaces, ensuring optimal uptake and systemic movement within the plant.

Improving Plant Uptake

Adjuvants enhance the penetration and translocation of pesticides within plant tissues, ensuring effective control of pests and diseases. By facilitating rapid absorption and systemic movement, they maximize the bioavailability of active ingredients, leading to superior pest management and crop protection.

Reducing Pesticide Drift

Drift control agents mitigate the risk of pesticide drift during application, minimizing off-target deposition and environmental contamination. By optimizing droplet size and distribution, these adjuvants ensure precise delivery of pesticides to target areas while reducing the potential for environmental impact.

Ensuring Compatibility with Tank Mixtures

Compatibility agents prevent chemical interactions and compatibility issues when mixing multiple pesticides in a tank mixture. They maintain the stability and integrity of the spray solution, preventing precipitation and clogging of spray equipment. By promoting uniform dispersion and compatibility, these adjuvants maximize the efficacy of tank mixtures and minimize the risk of equipment malfunction.

Market Trends and Growth Drivers

The agricultural activator adjuvants market is witnessing steady growth, driven by several key factors:

Increasing Adoption of Precision Farming Techniques

The rise of precision farming technologies, such as GPS-guided equipment and variable rate application systems, is driving the demand for adjuvants. These technologies enable farmers to optimize pesticide applications and maximize crop yield while minimizing input costs and environmental impact.

Growing Demand for Sustainable Agricultural Practices

With increasing consumer awareness and regulatory pressure, there is a growing demand for sustainable agricultural practices. Adjuvants play a crucial role in supporting sustainable farming by improving the efficiency and efficacy of pesticide applications, reducing chemical usage, and minimizing environmental footprint.

Rise in Research and Development Activities

The agricultural adjuvants industry is characterized by ongoing research and development efforts aimed at introducing innovative formulations and technologies. Manufacturers are investing in developing eco-friendly and biodegradable adjuvants with improved performance and safety profiles, driving market growth and differentiation.

Key Players in the Agricultural Activator Adjuvants Market

The agricultural activator adjuvants market is highly competitive, with several key players vying for market share. Some of the leading companies in the industry include:

Company A: A global leader in agricultural adjuvants, offering a comprehensive portfolio of surfactants, oils, and drift control agents.

Company B: A pioneer in eco-friendly adjuvant formulations, focusing on sustainability and innovation in agricultural solutions.

Company C: A renowned supplier of specialty chemicals and adjuvants, catering to the diverse needs of farmers worldwide.

Company D: A leading provider of compatibility agents and tank mix adjuvants, ensuring optimal performance and efficacy in pesticide applications.

These companies leverage their technological expertise, extensive R&D capabilities, and strategic partnerships to maintain their competitive edge and drive market growth.

Regional Analysis

The agricultural activator adjuvants market exhibits regional variations in terms of market dynamics, regulatory frameworks, and adoption rates.

North America

North America dominates the global adjuvants market, fueled by the presence of large-scale commercial farms and advanced agricultural practices. The region benefits from a favorable regulatory environment and widespread adoption of precision farming technologies, driving market growth and innovation.

Europe