#post office nsc calculator

Text

This blog post is about using an NSC calculator to estimate earnings on National Savings Certificates (NSCs) offered by the Post Office in India. NSCs are a safe investment with guaranteed returns but have a 5-year lock-in period. The calculator helps you input investment amount and see the estimated maturity amount and total interest earned. It is a good option for those seeking safe, long-term investment with tax benefits.

#investkraft#finance planning#investment#financial calculators#nsc calculator#nsc#nsc interest rate#National Saving Certificate#NSC Return Calculator

1 note

·

View note

Text

Proof of Investment (POI): What Employers and Employees Must Know

Proof of Investment (POI)

All employers in India are required to deduct tax from their employees’ salaries. They might deduct more or less if the employees fail to submit the right investment proof. Therefore, all employees must submit proof of investment so their employers can calculate and deduct the right tax amount for the financial year.

What is the difference between exemption and deduction?

Exemption: As per the Indian tax legislation, an exemption is an income that is not treated as taxable income. House rent allowance (HRA), paid by an employer, is an example. When a salaried employee pays rent to a landlord, a part of it becomes exempted. The amount of exemption is dependent on the city (metro or non-metro) in which the employee resides, and the submitted rent payment proof.

Deduction: A deduction is an amount that is treated as a deduction from an employee’s taxable income. Eligible savings instruments and donations fall into this category. These deductions are made during payroll processing and help reduce an employee’s net taxable income.

What is the difference between an investment declaration and proof of investment?

Investment declaration: An investment declaration is made when an employee joins a new organisation or during the beginning of the financial year. Submitted via Form 12BB, a declaration consists of the proposed investments and expenditures in the current financial year. These qualify for certain deductions and exemptions.

Proof of investment: In the month of January or February, every employee is asked to submit proof of the investments that were planned and made. The payroll department computes the final tax liability for the year and makes the necessary adjustments. The earlier computation would have been based on the investment declaration, which is only an estimated figure.

What are the most common savings investment schemes?

There are aggressive investors and conservative investors. The choice of instruments depends on the investor’s risk-taking mentality, expected rate of return and the investment plan made earlier. Furnished below are some of the popular schemes.

Provident Fund: Mandatory for organisations with 20 or more employees, Provident Fund is a government-run scheme with assured returns. The interest rate is in the range of 8.1% to 8.5%. It is fully exempted from income tax if certain conditions are met.

National Pension Scheme (NPS): NPS is a retirement savings scheme with lesser loading and admin charges. This instrument is not fully exempted from tax as of now. But the government has been making amendments to the provisions of the scheme.

National Savings Certificate (NSC): This is a fixed-return savings bond that can be opened at any post office. It offers a 6.8% interest with a 5-year lock-in period. Available only to Indian citizens, NSC is similar to a mutual fund.

Postal Savings Scheme: Offering an interest of 4%‒9% per annum, postal savings schemes are ideal for those who want a safe investment option. There are different types of tax savings schemes offered by the postal department.

Unit-linked Insurance Scheme: It is one scheme that provides the benefit of a long-term investment and a life insurance policy. It offers the provision to make withdrawals after a specified lock-in period. The different types of ULIP address the needs of different types of investors.

Insurance Scheme: A common tax-saving instrument, an insurance scheme is usually intended to protect the future of family members in the event of the death of the insured person. There are also schemes that cover medical exigencies and disabilities.

What are some of the common mistakes in investment-proof submission?

Some people delay the submission of POI and wait till the last minute. Sometimes, they misplace the original documents. This results in last-minute stress and errors. Also, the organisation finds it difficult to handle the sudden surge in the volume of requests and data. Even the server might throw up an error due to the heavy load. Therefore, employees must complete the submission as soon as HR opens the POI window.

Is it mandatory for employees to report their additional income?

There is no mandatory requirement for employees to furnish the details about all their earnings and expenses. But the organisation cannot accurately calculate the final tax liability without these details.

What happens if an employee does not submit any proof of investment?

Some employees may not be ready with the documents, and the organisation might have closed the POI submission window. In this case, the employees can submit the same at the time of IT return filing. Since the employer might have already deducted the TDS, the employee can claim a refund of excess tax by providing the bank account details.

Is there a deduction in the interest paid on a car loan?

If an employee takes a loan to buy an electric car, there is a tax deduction on the interest paid on the EMI. The income tax legislation allows a deduction of up to a maximum of INR 50,000 in this case.

Can an employer avoid the deduction of tax from an employee’s salary?

No, that’s not permitted. As per the law, employers have to deduct tax (TDS) from an employee’s salary and pay the amount to the government within seven days from the end of the month.

Is it compulsory to consider the income of an employee’s previous employer?

It is not mandatory but recommended. If the previous income is not divulged, the employee is likely to pay a higher tax amount. Hence, employees must furnish the details, so the current employer can factor that in and work out the final tax liability accurately.

Source Link - https://medium.com/@greytHRsoftware/proof-of-investment-poi-what-employers-and-employees-must-know-3c6f6b46db44

#POI#Proof of Investment#HR#Payroll#HR Software#Payroll Software#HRMS#HRM#HRIS#HCM#HRMS Software#greytHR

0 notes

Text

Get your money doubled with these POST OFFICE schemes; Check interest rate, return calculator, maturity time

Get your money doubled with these POST OFFICE schemes; Check interest rate, return calculator, maturity time

Post Office Investment Scheme Return Calculator: If you don’t want to take any risk with your money, you can put your money into these schemes including National Savings Certificate (NSC), Sukanya Samriddhi Yojana, Senior Citizen Saving Scheme (SCSS), Kisan Vikas Patra (KVP) and Senior Citizens Savings Scheme among others.

source…

View On WordPress

0 notes

Text

Become Independent in your Financial Investment

Usually this time around the year, we think about investments. These investments are usually tax saving investment and many people do not think beyond this. However, you should know there are two ways to become richer — first, earn more money (obviously) and second, save more wisely.

While no blog can help you achieve the first objective — please help yourself achieve this!

Coming to second objective: I have worked in financial sector for more than a decade and can tell you saving wisely works for persons in all income brackets. In series of blogs, I am going to guide you my way of managing my own portfolio. I still consider myself as callow investor; however, I am hoping my limited experience can be a good starting point to you.

So, what are your options?

Before we address this question, you need to know what your risk appetite is. Ok, no complex theories, just answer the following:

Q1. Are you saving for some purpose?

No, I am free bird

I have liabilities, but no particular goal in mind

Oh, yes of course

Q2. Are you comfortable investing in stock market?

Very comfortable

I can try

No, not at all

Now coming back to original question, following are the easily available options:

Bank Savings Account — why this is even an ‘investment’? Because some people still like to keep significant in hand cash, yes in 2021… And even after demonetisation!

Bank Fixed Deposits or Recurring Deposit — Well known conventional sort of investment

Mutual Funds — This one comes with lot of options: Liquid, Debt, Equity or Hybrid

National Saving Certificate (NSC) — Post office savings scheme

Gold or Silver — Solid physical investment in gold or silver

Stock Market — Direct equity investment through Demat account

NPS or PPF — Long term investment with guaranteed returns

Real Estate — Capital Gains through investment in property; involves high amount of investment

Insurance Plans — Traditional or Unit Linked plans with savings element

But why I asked two ‘stupid’ questions above then? Because your investment choices are related to above two ‘stupid’ questions. That also brings us to our second section.

How should I choose?

One should choose their investments in view of their goals and risks involved in the investment. Ohh yeah… That’s why those questions! Anything new here?

Yes, ‘diversification’ is a fancy word in investment world and desirable too. Hence, ideally you should invest in multiple instruments. But how? Here you go…

My suggestion would be to categorise investment and invest as follows:

If your answer to ‘stupid’ questions is both 1’s: First of all compliments for feeling like a free bird. Now, ideally all your investment can’t be in stock market, so basis your age, you may apply following thumb rule:

Category 1: Gold/ Silver & Equity (Equity Mutual Fund plus Real Estate) = (95 — Your Age)%

Category 2: Debt (PPF or NPS, Debt Mutual Funds, Bank Deposits, NSC) = (Your Age)%

Category 3: Liquid Funds (Saving Bank Account, Liquid Mutual Funds) = 5%

If your answer to ‘stupid’ questions is both 2’s, or 12, or 21, or 31, or 32: You are a wise kind of person, who wants to take calculated risk. You may possibly have loans or other expenses to bear, hence, following change in thumb rule for you:

Category 1: Gold/ Silver & Equity (Equity Mutual Fund plus Real Estate) = (75 — Your Age)%

Category 2: Debt (PPF or NPS, Debt Mutual Funds, Bank Deposits, NSC) = (Your Age+10)%

Category 3: Liquid Funds (Saving Bank Account, Liquid Mutual Funds) = 15%

If your answer to not-so-‘stupid�� questions is both 3’s, or 13, or 23: You are risk averse kind of investor and would like to keep maximum investment in Category 2 above. However, do keep 5% to 15% liquid portfolio (basis your liabilities).

Additional Point: For all those who have any particular short term goal in mind for their investment (say within 3–4 years horizon), your preferable investment would be Category 2 or Large Cap Mutual Funds. For long term goals — just follow the above suggestions! That’s what we all are here for.

Final Points

The above suggestion are broad indications only. Basically to give you comfort on how far you can go in each category. It will be very difficult to maintain these percentages at all point in times, so don’t panic if you are here or there a bit.

Managing your own portfolio may seem time consuming initially but it is much more rewarding in long term. Most of the investment agents are driven by commissions, and rightly so because it’s their living! But I can assure you, if in your hands, your investments can earn much more. It’s like your first new car… Somebody might be a good driver but you would like to drive yourself because there is no other way you can learn to drive it!

By now you should ask one question — where the hell is insurance? Well, that’s tricky. That needs lot of more writing. I will cover that in my next blog.

And I will also cover Mutual Funds, Stock Market, NPS. I can’t think of more. In case you have any more topics for me to cover, please comment.

#finance#investment#financialplanning#indianinvestors#india investment#individual investors#save money#become rich#smartinvesting#smart investing#smart investor#smart choices

1 note

·

View note

Text

Compare All Post Office Schemes 2022 - NSC, PPF, MIS, SSY, RD, TD, KVP, SCSS

Compare All Post Office Schemes 2022 – NSC, PPF, MIS, SSY, RD, TD, KVP, SCSS

Post office is a safe long term and short term investment option especially for people in rural areas. Post Office offers schemes for every age group whether it is for boy/girl/senior citizens etc. All post office savings schemes are very popular and people can compare all post office schemes 2022. People can also view Savings Schemes Interest Rate 2022, calculator, Post Office Small Savings…

View On WordPress

0 notes

Link

Know well about ITR forms

Who can file Income Tax Returns?

Individuals, HUFs, AOPs, BOIs, firms and companies are mandated to file the income tax return (ITR) if the income earned is taxable. Each of these taxpayers is taxed differently under the Income Tax laws of India wherein the domestic companies and firm have fixed a 22 per cent tax rate but the individuals are taxed as per the tax slabs.

Advantages of filing income tax returns (ITRS)

It has often seen that many individuals believe that if their salaries fall below the taxable bracket then they don’t need to file an income tax return (ITR). However, that is not true! Even if your earned income is not taxable, you should file ITR as it will benefit you in different ways.

Listed out the following advantages of filing income tax returns:

Avoid Penalties:

Easy Loan Approval:

Address Proof:

Compensate for Losses in the next Financial Year:

Hassle-free Visa Processing:

Filing ITR timely can help you avoid penalties imposed by the Income Tax Department for belated return that could cost you extra interest.

In India, ITR is one of the important documents asked by banks in sanctioning a loan to an individual. Many banks and NBFCs ask for ITR receipts of the latest 3 years when applying for the loan such as home loan, car loan etc. Such lenders consider ITR as the most authentic document of verifying an individual’s income. Hence, an individual who is filing ITR on time can benefit from hassle-free loan approval.

Income Tax Return (ITR) receipts can serve as a residential proof as it is sent directly to your registered address.

If you are eligible to file ITR but didn’t then you would not be able to carry forward the losses of the current financial year to the next financial year. Hence, it is vital to file the ITR to claim the losses in the future years.

At the time of applying for Visa, the embassies generally ask for past ITR receipts to process the Visa application of an individual. So, filing ITR before the due date can help you in quick Visa processing at the time of Visa application.

Things to remember before filing an Income Tax Return

Income tax return filing is very important and if you have not filed your return yet, it’s a good idea to get going and try to do it as early as possible. Tax filing involves a lot of paperwork, confusion and queries. To ensure a seamless process, give yourself enough lead-time for a smooth and timely return filing. Unfortunately, there are penalties to be paid, if the deadlines are missed. These fines range between Rs. 5,000 to 10,000, depending on the delay.

You can get help from professionals to file your tax return who can advise you on how to save tax, the available deductions and exemptions under 80C and assist you with investment planning. But, if you are planning to file returns yourself, here are a few important things you could keep in mind.

First of all, make sure to collect all the required documents that you will need to file your ITR Form such as Form 16, Form 26AS, investment documents, premium payments, loan statements, salary slips, bank statements, and proof of capital gains (if any) that will help you in providing the details of tax deducted at source (TDS) and to compute the gross taxable income of yours in that financial year.

Similar to this, if you have redeemed mutual fund units within that year, you can reach out to your mutual fund house to provide you with the transaction statements and capital gain statements. Remember, if the gains exceed Rs. 1 lakh, you will be required to pay tax on LTCG. Once you finished computing your total income, the next thing is to calculate your tax liability by applying the tax rates as per your income slab.

Important Things To Remember While Filing Income Tax Returns

Know Your ITR Forms Well

The Central Board of Direct Taxes (CBDT) has made few amendments in the ITR forms to ease the process of filing Income Tax returns. The number of forms to be used by taxpayers has been reduced from 9 to 7. For individuals with annual taxable income (from salary, interest, one house property) of up to Rs. 50 lakh, ITR 1 is required to be filed. Whereas, for individuals with annual taxable income of more than Rs. 50 lakh, ITR 2 is required to be filed.

Mandatory Disclosure

Following up on the Central Government's efforts on demonetisation, the Income Tax department has made it mandatory to disclose cash deposits of Rs. 2 lakh and more in bank accounts. This was first initiated during the demonetisation period and continues to this day. The Income Tax department requires a declaration in a separate column giving details of money deposited along with bank details in the income tax returns. To prevent being taxed at 60% plus surcharge and cess, tax payers need to explain all sources or forms of income or investment.

Carefully Select the Assessment Year and Financial Year

Assessment Year and Financial Year are not the same and you need to be familiar with them in order to correctly file your taxes. Financial Year is the period or year within which you earn the income, whereas Assessment Year is the period or year that follows Financial Year and it is in this year that you file your tax return. Every Financial Year and Assessment Year begins on the 1st of April and ends on 31st of March. Assessment Year always comes after Financial Year.

Since your income is taxed in the Assessment Year, you have to select Assessment Year while filing your income tax return.

Check For Deductions Under 80C

Section 80C entitles you to certain deductions from the gross total income, up to a maximum limit of Rs. 1.5 lakh. It is the most widely used option to save income tax. The investments and expenditures that qualify for deduction under section 80C are investments in National Savings Certificates (NSC), Kisan Vikas Patra (KVP), notified Equity Linked Saving Scheme (ELSS) of a mutual fund, five-year post office term deposits, five-year bank fixed deposits, contribution to Employee Provident Fund (EPF), Public Provident Fund (PPF), Superannuation Funds and premiums paid for life insurance, annuity plan and Unit-Linked Insurance Plans (ULIP), etc.

These investments can not only be claimed as deduction while calculating your total taxable income but can also generate good returns. Moreover, investment in PPF, superannuation funds, etc. also help in accumulating funds for retirement planning.

Check TDS on Form 26A

Form 26A is an important document for tax filing. It provides details of the income paid to you, the tax deducted on that income and the amount of TDS deposited by the payer with the Government. The form also contains details of any refund applicable to you. To check your tax deduction on Form 26A, you have to go to https://incometaxindiaefiling.gov.in and login to your account. Next, you have to go to ‘My Account’ and click on ‘View Form 26AS’ in the drop down.

Conclusion

While filing your income tax return, ensure that you know the relevant ITR forms well, make the necessary disclosures, select appropriate assessment year, take advantage of 80C deductions and verify your TDS from Form 26A. This will ensure a smooth and hassle-free tax filing process.

For reference: http://www.incometaxindiaefiling.gov.in/main/ListOfITRsAndOtherForms

0 notes

Link

Most of the individuals want to multiply their wealth but due to market risks, they hesitate while investing. They want to take low risks and higher returns. So, here is an investment option for you that will help you multiply your money and you can also enjoy tax rebates while calculating your annual income. This investment is known as National Saving Certificate and it is available at your nearest post office. This plan is an initiative by the government that helps the individuals to make a risk-free investment. So, you must first understand the meaning of this certificate and see how it will help you to grow your wealth at low risk.

0 notes

Text

Post Office MIS Scheme in Hindi | Best Investment Plan

Post office MIS scheme in Hindi ( POMIS )

MIS क्या है ?

इसके लिए किन दस्तावेजो की जरूरत होती है ? MIS में कौन कौन अपना खाता खुलवा सकता है ? Mis में कितनी ब्याज मिलेगी ? Mis का meturity period क्या है ? क्या mis रिस्क फ्री और टैक्स फ्री है ? कोन इस सुविधा का लाभ ले सकता है ? इन सब सवालो के जवाब हम देंगे अपने इस ब्लॉग में तो आइए जानते है

MIS क्या है –

MIS यानि मंथली इनकम स्कीम है । ये पोस्ट ऑफिस की एक बेहतरीन स्कीम है । इस स्कीम में आपको fd और RD दोनों से अछे रिटर्न है । यह स्कीम बाकि सब से अच्छी इसलिए भी है क्योंकि इसमें आपको हर महीने ब्याज मिलेगी ।

रिस्क फ्री – मन्थली इनकम स्कीम भी fd, RD, nsc की तरह रिस्क फ्री स्कीम है जो निवेशक रिस्क ज्यादा नहीं ले सकते है उनके लिए ये एक बहुत ही अच्छी स्कीम है ।

खाता कौन खोल सकता है –

18 साल से ऊपर का हर भारतीय नागरिक इस स्कीम का फायदा ले सकता है । परन्तु यदि आप माइनर का 10 साल से ज्यादा लड़का / लड़की का खाता खोलना चाहते है तो खाता खुल जायेगा परंतु उसे ऑपरेट माता पिता ही कर सकेंगे ।

ट्रांसफर – मंथली इनकम स्कीम पोस्ट ऑफिस की एक बेहतरीन स्कीम है । आप अगर किसी वजह से एक शहर से दूसरे शहर में चले गए तो आप अपना खाता ट्रांसफर भी कर सकते है ।

ब्याज – मंथली इनकम स्कीम में आपको 7.9% ब्याज मिलती है । पोस्ट ऑफिस की ब्याज हर तीन महीने में बदलती रहती है । परंतु इस स्कीम में ब्याज 7-9% तक रहती है ।

टैक्स – इस स्कीम में आपको सेक्शन 80c के तहत आपको टैक्स में कोई भी छूट नही मिलेगी । अगर आप साल का 10000 से ऊपर रिटर्न कमाते हो तो आपको वहाँ टीडीएस कटेगा । परंतु यदि आप रिटर्न फाइल करते है और आप इनकम टैक्स की सूची में नही आते तो आप का टीडीएस नही कटेगा ।

Meturity period – MIS का meturity period 5 साल का होता है ।

आपको पैसे कैसे मिलेंगे –

इस स्कीम में आपको हर महीने ब्याज मिलेगी । आपको ये पैसे आपका यदि पोस्ट ऑफिस में सेविंग खाता है तो आपके पैसे वहाँ जमा हो जाएंगे नहीं तो आपको चेक के द्वारा आपके पैसे मिल जायेंगे ।

कितने पैसे जमा करा सकते है –

आप इस स्कीम में कम से कम 1500 रुपए तक जमा करा सकते है । यदि इस स्कीम में एक अकाउंट होल्डर है तो वह 4.5 लाख रूपए तक जमा करा सकता है । परंतु यदि 2 या 3 अकाउंट होल्डर है तो इसकी लिमिट 9 लाख तक है । आप ये पैसे यानि 1500 से ज्यादा आप जितने भी जमा कराना चाहते हो तो आप एक ही बार में करा सकते है ।

Pre -mature closure –.

इस स्कीम में आप पहले साल यानि एक साल में आप अपने पैसे को नहीं निकाल सकते । यदि आप 1 से 3 साल के बीच में पैसो को निकलते है तो आपको 2% का जुर्माना लगेगा । यदि आप 3 से 5 साल के बीच में पैसे को निकलते है तो आपको 1 % का जुर्माना लगेगा ।

नॉमिनी – मंथली इनकम स्कीम में आप अपनी फैमिली के किसी एक मेंबर को नॉमिनी बना सकते है ।

ट्रांसफर – मंथली इनकम स्कीम पोस्ट ऑफिस की एक बेहतरीन स्कीम है । आप अगर किसी वजह से एक शहर से दूसरे शहर में चले गए तो आप अपना खाता ट्रांसफर भी कर सकते है ।

Calculation – अब हम देखते है calculation कर के की आपको कितने रुपए मिलेंगे –

यदि आप 1 लाख रुपए जमा करवाते हो तो आपको हर महीने 690 रुपए मिलेंगे ।

अगर आप 2 लाख जमा करवाते है तो आपको 1380 रुपए हर महीने ब्याज मिलेगी ।

यदि आप 9 लाख यानि जो इस स्कीम की लिमिट है उतना जमा करवाओगे तो आपको 6210 रुपए हर महीने मिलेंगे।

click here https://amzn.to/3kIoRqC

अगर आप MIS या किसी भी और इंवेस्टमेंट के बारे में कुछ पूछना चाहते है या कोई सुझाव देना चाहते है तो आप मुझे कमेंट कर सकते है या आप मुझे ईमेल भी कर सकते है [email protected] . ऐसे ही अन्य जानकारी के लिए TarunBlogs को फॉलो करते रहें|

Click here to Learn More

0 notes

Text

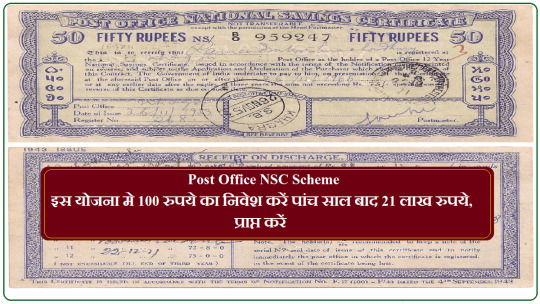

Post Office NSC Scheme : इस योजना में 100 रुपये का निवेश करें पांच साल बाद 21 लाख प्राप्त करें, जानें कैसे

Post Office NSC Scheme : डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office National Savings Certificate Scheme) क्या आपने कभी डाकघर में बचत और निवेश करने के बारे में सोचा है ! यदि नहीं, तो इसके बारे में सोचें क्योंकि डाकघर (Post Office) में आपके पैसे को सुरक्षित रखने और किसी भी अन्य ��्रोतों की तुलना में बदले में अधिक लाभ देने के लिए कई लाभकारी योजनाएं हैं ! इसके अलावा, छोटी बचत का परिणाम आने वाले समय में बड़ा हो सकता है और भविष्य में बड़ी राहत प्रदान कर सकता है !

Post Office NSC Scheme

Post Office NSC Scheme

डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office National Savings Certificate Yojana) की योजनाओं पर निवेशकों को सालाना 6.8 फीसदी की दर से ब्याज मिलता रहेगा ! यह उन निवेशकों के लिए एक अच्छी खबर है, जो शून्य जोखिम लेने की क्षमता रखते हैं और अपने निवेश पर गारंटीड रिटर्न चाहते हैं ! डाकघर (India Post) लघु बचत योजनाओं का परीक्षण और परीक्षण किया जाता है और यह एक निवेशक को कम समय में कई गुना धन उगाहने में मदद करता है !

डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office NSC Scheme) के अधिकांश निवेशकों को आकर्षित करती है ! यह निवेश उपकरण निवेशकों को सिर्फ 100 रुपये के साथ निवेश शुरू करने में मदद करता है ! ऐसे में आप सरकारी योजनाओं में निवेश कर सकते हैं ! पोस्ट ऑफिस (India Post) में कई ऐसी योजनाएं हैं जहां आपको निवेश में अच्छा रिटर्न मिल सकता है ! राष्ट्रीय बचत प्रमाणपत्र (National Savings Certificate) भी डाकघर की एक बेहतरीन योजना है ! इस डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office National Savings Certificate Yojana) में आप कुछ वर्षों में बड़ा पैसा जोड़ सकते हैं !

Post Office National Savings Certificate Benefits

राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office National Savings Certificate Yojana ) की परिपक्वता अवधि 5 वर्ष है ! खास बात यह है कि कुछ शर्तों के साथ आप 1 साल की मैच्योरिटी अवधि के बाद खाते की राशि निकाल सकते हैं ! राष्ट्रीय बचत प्रमाणपत्र में ब्याज दरें (National Savings Certificate Interest Rates) सरकार द्वारा वित्तीय वर्ष की प्रत्येक तिमाही की शुरुआत में निर्धारित की जाती हैं !

आप इसमें 100 रुपये से निवेश शुरू कर सकते हैं ! इस डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office NSC Scheme)पर फिलहाल सालाना 6.8 फीसदी ब्याज मिल रहा है ! इस योजना के तहत आप आयकर की धारा 80सी के तहत सालाना 1.5 लाख रुपये की कर छूट भी प्राप्त कर सकते हैं !

Post Office NSC Scheme

भारतीय नागरिक किसी भी डाकघर (Post Office) से एनएससी (NSC) प्राप्त कर सकते हैं ! यह निवेश विकल्प उन व्यक्तियों की पसंदीदा पसंद है जो सुरक्षित निवेश के रास्ते तलाश रहे हैं ! क्योंकि यह भारत सरकार द्वारा समर्थित है, जिसके परिणामस्वरूप कम जोखिम है !

वर्तमान में 5 वर्ष के कार्यकाल के साथ NSC के लिए उपलब्ध है ! NSC के लिए ब्याज दरें 7-8% PA के बीच होती हैं और हर वित्तीय वर्ष में वित्त मंत्रालय द्वारा तय की जाती हैं ! उदाहरण के लिए, वित्त वर्ष 2019-20 के लिए राष्ट्रीय बचत प्रमाणपत्र (National Savings Certificate) की ब्याज दर सालाना 8% चक्रवृद्धि है !

जबकि न्यूनतम निवेश राशि 100 रुपये है, पीपीएफ के विपरीत जमा की जा सकने वाली अधिकतम राशि की कोई सीमा नहीं है ! हालांकि, केवल 1.5 लाख रुपये सालाना धारा 80 सी के तहत कर छूट के लिए योग्य हैं !

5 साल में मैच्योर होंगे 21 लाख

उदाहरण के लिए अगर आप शुरुआत में राष्ट्रीय बचत प्रमाणपत्र योजना (National Savings Certificate Yojana) में 15 लाख रुपये का निवेश करते हैं ! तो आपको 5 साल बाद 6.8 की ब्याज दर पर 20.85 लाख रुपये की राशि मिलेगी ! इसमें आपका निवेश 15 लाख होगा, लेकिन ब्याज के रूप में करीब 6 लाख रुपये का फायदा होगा. आप चाहें तो इसे और भी आगे बढ़ा सकते हैं !

राष्ट्रीय बचत प्रमाणपत्र क्या है |

राष्ट्रीय बचत प्रमाणपत्र (National Savings Certificate) भारतीय डाक द्वारा दी जाने वाली छोटी बचत योजनाओं में से एक है ! चूंकि यह सरकार समर्थित निवेश उपकरण है इसलिए एक निवेशक यहां पैसा बैंकों की तुलना में अधिक सुरक्षित माना जाता है ! इसलिए, यहां निवेशकों का पैसा किसी भी जोखिम से मुक्त है !

राष्ट्रीय बचत प्रमाणपत्र कैलक्यूलेटर

में निवेश के माध्यम से केवल पांच वर्षों में करोड़पति कैसे बन सकता है ! सेबी पंजीकृत कर और निवेश विशेषज्ञ मणिकरण सिंघल ने कहा, डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office National Savings Certificate Scheme) में, कोई एकमुश्त निवेश पर किसी के रिटर्न को अधिकतम कर सकता है ! का उपयोग करना एनएससी कैलकुलेटर, (NSC Calculator,)अगर कोई निवेशक इस इंडिया पोस्ट (India Post) योजना में 1 लाख रुपये का निवेश करता है, तो पांच साल बाद शुद्ध रिटर्न 1,38,949 रुपये होगा !

राष्ट्रीय बचत प्रमाणपत्र (Post Office NSC Scheme)

आप राष्ट्रीय बचत प्रमाणपत्र (National Savings Certificate) में रुपये की छोटी जमा राशि के साथ निवेश कर सकते हैं ! 100 एकल व्यक्ति के रूप में, संयुक्त रूप से या नाबालिग के अभिभावक के रूप में ! इस डाकघर राष्ट्रीय बचत प्रमाणपत्र योजना (Post Office NSC Scheme) के लिए लॉक-इन अवधि 5 वर्ष है ! साथ ही, एनएससी पर वार्षिक ब्याज का पुन: निवेश किया जाता है और परिपक्वता के समय संचित राशि के रूप में भुगतान किया जाता है !

Read the full article

0 notes

Link

Indian citizens are quite familiar with India Post since their childhood. It was the only medium of communication for millions and now it has become a popular financial service provider in the country. Since 1st September 2018, India Post is running the IPPB (India Post Payments Bank) throughout the country. This is a 100% Government owned bank that has allowed near about 17 crore postal savings bank accounts with IPPB. This bank provides an array of financial services to Indian citizens including, account services, QR code payment services, UPI (Unified Payment Interface), NEFT (National Electronic Funds Transfer), IMPS (Immediate Payment Service), real-time gross settlement, Bharat Bill pay, DBT (Direct Benefit Transfer) etc. through its wide network of post offices and e-banking. This is all about the spread and reach of IPPB now. If you are thinking of any safe investment start banking with IPPB. Post office has many saving schemes that will help you to save your money and earn as you are investing them. For income taxpayers, NSC (National Savings Certificate) is a popular investment option. Let’s get to know more about this investment scheme as described by the India Post. National Savings Certificate (NSC): As discussed earlier, this scheme is very popular among income tax payers. Many people might not be aware of such scheme that offers a safe and convenient way of investing their hard-earned money. Investment tenure: NSC has a defined period I.e, 5 years as per 8th issue. Rate of interest: If you are investing in NSC, you will get 7.9% (from 1st July 2019) per annum and it gets compounded annually. However, it is payable after maturity. Limit in minimum and maximum balance: A minimum of Rs. 1000/- and in multiples of Rs. 100/- can be invested for NSC. There is no maximum limit for investment. Earlier a certificate was issued and now-a-days (from 1st July 2016), a passbook is issued for the NSC account. Who can open a NSC account? Following people can open NSC account in IPPBs and Post Offices 1. On behalf of a minor, one adult can open an account 2. Minors above 10 years of age can open one account 3. A person having unsound mind can also open one account with the help of a guardian 4. A single adult can open an account 5. Joint ‘A’ type account with maximum 3 adults can be opened (In this case, the amount is payable to both) 6. Joint ‘B’ type account with maximum 3 adults can be opened (In this case, the amount is payable to either) Scope of income tax rebate: If you are an income tax payer, you might be looking for sources where you can invest and get tax rebate at the same time. NSC is here for you. It comes under section 80C of IT Act. Your NSC deposits qualify for tax rebate, but don’t forget to calculate the total amount of your 80C investments. As per 80C, you can only invest a maximum of Rs. 1,50,000/-. Transfer of NSC from one person to another: Yes, this is possible. NSC after opening can be transferred to another person only once from the date of opening to the date of maturity. In this case, the old name will be rounded up by the post office and the new holder name will be written on the passbook while following other procedures and formalities. How money grows through this investment? Though there is a rate of interest 7.9% is paid for the NSC, you might be looking for a real calculation that shows your money growing and after 5 years this much you are getting against your investment from this scheme. Let’s have a calculation for worth of Rs. 70,000/- NSC calculation: Base investment amount – Rs. 70,000/- Interest provided by IPPB – 7.9% per annum which is compounded annually Investment period – 5 years Based on the above details let’s calculate and see how much you will get after 5 years. Year——-Interest for the year—–Total interest —–Total balance for the year 1st————-5,530.00—————-5,530.00—————–75,530.00 2nd————5,966.87—————-11,496.87—————-81,496.87 3rd————6,438.25—————-17,935.12—————-87,935.12 4th————6,946.87—————-24,882.00—————-94,882.00 5th————7,495.68—————-32,377.68—————-102,377.68 During maturity, the amount Rs. 70,000/- becomes Rs. 102,377.68/-. It means a total amount of Rs. 32,377.68 is your profit from seventy thousand rupees’ investment. Additionally, you have the tax rebate over base investment amount for the 1st year. Isn’t it a good investment plan? Hope this article will help Indians who plan for a long-term investment and good returns over a period of five years. As India Post is a government entity, it is safe and 100% secure. Related ProductsLoading products..

1 note

·

View note

Text

Trump impeachment witnesses leave a trail of tantalizing clues

They showed up, offered prepared remarks and answered hours of questions to lay out their side of the Ukraine-related impeachment inquiry now engulfing President Donald Trump.

But the current and former U.S. officials — several of them experienced diplomats accustomed to documenting almost everything — also left a trail of clues for investigators to follow. The breadcrumbs — word of a cable here, mention of a meeting there — are scattered across what’s been made public from the testimonies.

Given the secrecy involved, it’s not clear how many of the relevant materials Capitol Hill staffers already have managed to get. And the Trump administration has warned that it will resist cooperating with the probe. Still, what is known has set off a scramble across Washington to find a smoking gun, or pieces of one.

“Neither government nor conspiracies can operate without a paper trail,” said Austin Evers, executive director of American Oversight, a watchdog group suing the Trump administration for Ukraine-linked documents. “These are busy people. They live by emails, texts and calendars.”

POLITICO spoke with former U.S. officials and oversight experts and scoured publicly available information from the testimonies. The following are just some of the key clues that witnesses have shared:

Trump’s aid-freeze ‘directive’

Of all the testimonies so far, that of William Taylor, the U.S. diplomat now leading the U.S. Embassy in Kyiv, appears most fruitful for investigators seeking a roadmap to documents they need — documents the State Department is resisting sharing for now.

One clue in particular stood out: a “directive” Trump is said to have given freezing U.S. military aid to Ukraine. House Democrats are trying to establish whether Trump froze the aid to pressure Ukraine’s government to open investigations into former Vice President Joe Biden, a political rival, and Biden’s son Hunter.

According to Taylor’s opening statement, he learned of the directive while participating in a July 18 National Security Council secure video-conference call. A person Taylor described as a staff member of the Office of Management and Budget mentioned it.

“All that the OMB staff person said was that the directive had come from the president to the (acting) chief of staff (Mick Mulvaney) to OMB,” Taylor said.

A great deal will depend on whether the directive was in writing, and if so, whether Trump spelled out why he wanted the aid frozen. But even if it was not written down, there likely are other ways to establish the existence of Trump’s order, from call logs to notes taken by others of various officials’ interactions with the president.

Taylor noted that after the OMB staffer’s explanation, a series of NSC-led interagency meetings followed in which participants concluded the security aid should be resumed. Staffers likely kept notes of those meetings, too. Taylor also mentioned that the Pentagon crafted an analysis of the aid’s effectiveness, another potential document.

The cable to Pompeo

Secretary of State Mike Pompeo’s role has been an enduring mystery throughout the impeachment inquiry. But both Taylor and Marie Yovanovitch, the former U.S. ambassador to Ukraine that Pompeo pulled out early from her post, offered leads on that front.

Taylor said that on Aug. 29, before he’d personally realized that the U.S. aid to Ukraine might have been frozen to help Trump’s political ambitions, he sent a cable to Pompeo conveying his concern about withholding the aid. Pompeo did not respond, Taylor said.

The cable itself could prove interesting, but Taylor also added that he’d heard that soon after receiving it, Pompeo took the cable with him to a meeting at the White House focused on security assistance for Ukraine. The notes from that meeting could prove significant, especially if there was any discussion of exactly why the aid was being withheld, or whether Pompeo spoke with the president about it.

In describing her removal, Yovanovitch mentioned a few tidbits that could shed light on Pompeo’s actions. She said that the State Department had asked her in early March to extend her tour in Ukraine until 2020; a document with that request is likely to exist, and would be evidence of her good standing in the role.

She also said that in late April she was told to fly back to Washington. That’s when Deputy Secretary of State John Sullivan told her she was being recalled early. According to Yovanovitch, Sulivan told her that she had “done nothing wrong” and that “the department had been under pressure from the president to remove me since the summer of 2018.”

That is nearly a year’s worth of time for such “pressure from the president.” Investigators will likely want to obtain emails, meeting notes and other materials linking the State Department, the White House and Yovanovitch. While Pompeo’s own communications could prove vital, those of his top aides and assistants – including Sullivan – could be just as enlightening.

The administration will likely try to block the release of any document that was generated from the White House, even if it was sent to State, citing executive privilege. Odds are, though, that there are “intra-State” documents that wouldn’t be subject to such a claim. That’s true not just for what happened to Yovanovitch but also for the broader questions about Ukraine policy.

The “intra-State” conversations could include communications between Pompeo and Gordon Sondland, the U.S. ambassador to the European Union who was heavily involved in Ukraine policy through what Taylor described as the “irregular channel.” In his testimony, Sondland made a point of repeatedly suggesting Pompeo was in the loop. “I understand that all my actions involving Ukraine had the blessing of Secretary Pompeo as my work was consistent with long-standing U.S. foreign policy objectives,” he said.

Conversations with Ukrainians

U.S. diplomats who have interactions of any substance with a foreign official typically document them, often through a cable or an email to others at the State Department so that they are up to date. According to the testimonies, there were many such interactions.

For instance, Bill Taylor referred to an odd June 28 conference call that first included him, Sondland, and others, and which was later broadened to include the new Ukrainian president, Volodymyr Zelensky.

Prior to Zelensky joining, there were cryptic mentions of Trump’s desire to see Ukrainian investigations. Among those mentioning them was Kurt Volker, at the time the U.S. special envoy for Ukraine negotiations. Taylor said he “reported on this call” to Deputy Assistant Secretary of State George Kent and also wrote a “memo for the record” dated June 30 summarizing the conversation with Zelensky.

While Taylor, a veteran diplomat with 50 years of government service, has indicated he rigorously documented interactions with the Ukrainians — as well as those with other State Department officials — it's less clear how much Sondland and Volker did the same.

Their record-keeping could help establish the basics of what was discussed during two critical meetings: A July 10 one in the White House between U.S. and Ukrainian officials; and a July 26 meeting in Kyiv between U.S. and Ukrainian officials. According to Taylor and Fiona Hill, a former National Security Council official, the July 10 meeting was especially explosive as then-national security adviser John Bolton grew livid at Sondland when he realized Trump’s political calculations might be playing a role in shaping Ukraine policy. In Sondland’s opening statement, however, he either leaves out or glosses over that aspect of the meeting.

Volker, a former Foreign Service officer, has already handed over a batch of text messages to investigators. He quit as special envoy and has been largely cooperative. Sondland had no diplomatic experience but was given an ambassadorship after donating $1 million to Trump’s inauguration. He has said the State Department has his relevant documents, but the department has been slow to respond to congressional subpoenas for the material.

But Sondland indicated in his testimony that he prefers to communicate orally when possible, although he insisted that’s not because he wants to avoid creating a record. Attempting to clarify why in some text message exchanges with others he used phrases like “Call me” or otherwise suggested stopping texting, he said, “In my view, diplomacy is best handled through back-and-forth conversation.”

Outreach to Giuliani

One potentially valuable avenue for investigators is finding any and all communications between U.S. officials and Rudy Giuliani, the president’s personal lawyer.

Giuliani was part of what Hill and Taylor depicted as a shadow foreign policy aimed at pressuring Ukraine to investigate the Bidens; Trump directed some of his diplomats to deal with Giuliani on aspects of U.S. policy toward Ukraine, according to the testimonies, and according to an interview outgoing Energy Secretary Rick Perry gave the Wall Street Journal.

Because Giuliani is not a U.S. government official, communications with him by U.S. officials — including texts or emails — should, in theory, be easier to obtain because they are unlikely to contain classified material. Giuliani may try to shield his communications by referring to attorney-client privilege, but legal experts insist that argument can be used only in a narrow manner.

American Oversight’s records request to the administration includes senior U.S. officials’ communications with Giuliani; this past week, a judge ordered the State Department to start sending over documents to the watchdog group within 30 days.

The unnamed

For every big name brought up in the inquiry, there are lower-level government officials whose own records may prove critical to piecing together the puzzle.

Who was the unnamed OMB staffer Taylor mentioned? Who put Ukraine-related calls and meetings on the president’s calendar? Who wrote up the summaries of conclusions of Ukraine-related meetings at the National Security Council? Who took contemporaneous notes that match those summaries?

In a sense, the White House already has given Congress the most damning breadcrumb yet: the detailed readout of a July 25 phone call between Trump and Zelensky, in which the U.S. president repeatedly urges his Ukrainian counterpart to investigate Biden.

For an airtight case proving a “quid pro quo,” though, it might come down to the word of an administrative assistant. Did any White House aides, for instance, take contemporaneous notes of the president linking the military aid directly to political favors?

For now, the House committees overseeing the impeachment inquiry have put in broadly worded requests and subpoenas for documents. For instance, they’ve demanded “any and all records generated or received by the State Department in connection with or that refer, or relate in any way to the July 25 call.”

Thanks to the clues offered so far in the various testimonies, the president’s own advisers may have made that task far simpler.

Article originally published on POLITICO Magazine

source https://www.politico.com/news/2019/10/28/trump-impeachment-witnesses-diplomats-congress-059622

0 notes

Photo

Tax on Income, is it a Big Burden? Still there is a chance to Save on Tax…

The financial year ends in next few days; by this time there is clarity on how to file Income Tax Returns. However, still there is a hope on Tax exemptions. Now this is the time we need to cross check our calculations on Tax once again.

To ensure maximum tax free earnings, we need to explore different ways to reduce the tax payments and have more benefits in every financial year. For this, the submission buzz starts among the tax payers after January only. While everyone waits till the end of submission date, in a hurry most people go to the financial plans which are not relevant to their financial needs. This is the time where we need to check subscribed fund schemes for that particular year to validate the maturity and income benefits of the schemes, hence, ensure to check your subscriptions before filing your returns.

Thus you will have clear mind on how to start the new financial year from the beginning.

Have you submitted Income Proofs and Declarations?

Salaried people as of now they might have submitted the proof of income from different schemes to the Company Management for tax calculations, before you do this you should cross check each and every scheme is important. For to claim reimbursement on various expenses you made during the financial year, you need to keep ready to submit the Rent receipts for House Rent Allowance (HRA) received, Leave Travel Allowance (LTA) receipts from your Holiday trips and Medical Bills, Uniform Allowances, Car / Transportation bills, Telephone bills, Books and stationery expenses etc., or else you may lose the opportunity to claim the reimbursement on certain bills and you may attract the Tax at the base. So, now you have the chance to file your returns on income and claim for refunds if any.

Keeping an Eye on your Expenses:

Essential expenses like Children Tuition Fee, Life Insurance, Health Insurance premiums, Principal & Interest on Home Loan, Interest on Education loan, some of the medical expenses for chronic diseases treatment, exemptions for Physically disabled and Expenses on Lab Tests etc., were eligible for exemption under tax. To get more benefits and reduce levy of tax on your earnings, you need to keep an eye on the above mentioned expenses. In some cases, you may not get HRA while you are employed/working there you have a cushion under Section 80GG you may claim exemption upto Rs.60,000/- on House Rent, this will be applicable to even Self-employed or Business People. As discussed every avenue is fulfilled however, still feels have cushion for more investment you may go for various investment schemes available in the market.

Insurance is not only the Criteria, there is more to see:

In general most of the people only see the Life Insurance as a Tax Saving avenue, keeping this trend in mind the insurance companies also push different new policies to attract the Tax payers. In this juncture, it is not advisable to buy any Policy merely for Tax Saving purpose without analysing the Pros and Cons, which is always not right. Tax Saving on Conventional Insurance Policies are troublesome in financial view point. Most importantly, Tax Saving might be the additional source only and it will not become main source in choosing the Policy. You need to analyse the insurance requirement from the Policy. Choose the Policy which gives more protection on minimum premium payout, give priority to Term Policy. Find Policies, with which many schemes are available in the market to reduce the Tax burden. Here you need to remember one thing whatever Policy, you choose before 31st March only considered for the current financial year.

Target and Reach Your Goal :

At the end, any Investment scheme you target should yield your financial goals. Ensure, your scheme gives a chance of being long term investment at the same time it helps in Tax Saving. But keep remember what, one thing which investing is only not the criteria also if there is a Tax Saving on the profit on maturity is more beneficial to a tax payer. So, keep all these things in mind while selecting a policy.

Public Provident Fund (PPF) : This scheme allows you to invest for a long term period of 15 years at the convenient intervals. You can invest at a maximum of Rs.1,50,000/- per each financial year.

Sukanya Samrudhi Yojana (SSY) : Children with the age below 10 years are eligible to enroll to this scheme to invest. A maximum investment of Rs.1,50,000/- can be done per each financial year.

These two are last minute investment schemes for whom they do not have time to find a right scheme at the end of the year. The profits earned from these schemes were considered free of Tax. It’s easy to Enroll or open account under these schemes from any of the Nationalised Bank or Post Office.

Equity Linked Savings Schemes (ELSS) :

This scheme also facilitates Tax Saving. However, Single time large investment to this scheme is not safe since these are purely linked to share market as it is volatile in nature and prone to losses. Hence, it is best advisable to invest in small amounts more times beginning from the financial year. You can invest a maximum amount however as per the rule of Section 80C the Tax Saving will be permitted to a maximum investment of Rs.1,50,000/-. In this scheme you can carry the investment plan upto 3 years and it is the only Short Term Investment Plan among Tax Saving Plans. Above all these things there is an ample chance of increased profits with the investment and no Tax on profit incomes (Profit of Rs.1,00,000/- above on the Long Term Investment Plans will attract Tax) after maturity are the benefits with these schemes. It is easy to enroll into these schemes while visiting nearest Banks or Stock Brokerage companies. You can also get in touch with Mutual Fund Advisers to opt these schemes.

National Pension Scheme (NPS):

If you want to Invest over and above Section 80C permits you have another choice of investment plan under National Pension Scheme, under this maximum limit of investment is Rs.50,000/- and save Tax. If you have small amounts of money try investing in this scheme.

To Save Tax still you have a chance. Let us assume you do not have more money in your hands then the Schemes which fall under Section 80C are National Savings Certificate (NSC), 5 Years Banks Fixed Deposits, Post-office Term Deposits can be considered for Investments. You can also refer Government Bonds and Adult Savings Schemes for Tax Saving purpose. The profits received from this type of schemes can be shown under Personal Income and Tax assessment can be done as per the concerned slabs.

Tax Savings through Social Services:

Some donate to Prime Ministers, Chief Ministers Welfare Relief Funds and Non-profit Social Service Organisations, Registered & Notified Political Parties, Science & Technical Research Organisations, which are considered under Section 80G, 80GGA, 80GGC Tax Slabs. Here,the cash donations are limited upto Rs.2000/- only. Keep the donation payment receipts till you file the returns and claim Tax Exemptions. Few Managements take on account of these donations at basic income calculations of their employees.

Remember basic things while you file Tax Returns:

Saving every rupee you earn always may not be the right thought as it creates financial troubles some times.

Plan your Short Term, Mid Term and Long Term financial requirements. If you really have excess money for the next 5 years then only go for investment schemes.

Investment is not the only criteria but also Calculate, how much income you receive from the investments you made?

Read and learn every investment scheme and analyse thoroughly before taking an investment decision.

Now, you have only not more than a week, you need to keep money ready and investing in the right scheme such things should be planned immediately.

0 notes

Text

Should I Take a Personal Loan to Invest?

Personal loans are designed to provide monetary help for the persons who are in need of urgent fund. The best use of personal loan can be availed if the lent amount is used in medical expenses, urgent travel, marriage expenses etc. But there comes a big question if a personal loan is intended to invest for a high and prompt return.

Dreaming of earning a lot while investing the borrowed amount is probably a bad financial decision. The reasons which have made many financial experts advise people to stay away from investing by borrowing are revealed in this article.

Before knowing the adverse effect of investing by borrowing let us check the available investment options in India. Here are some of the best investment options in India that reap maximum return:

PPF: Public Provident Fund: With a minimum of ₹ 500 up to ₹ 100,000 can be invested and the return on this is tax-free. The current interest rate on PPF account is fixed at 8.7% per annum.

Peer to Peer Lending: Commonly known as P2P lending is an alternative to bank loans. This is a type of investment where the role of banks or lending institutions is eliminated. Any interested person can invest in P2P lending through online platforms. Some of such platforms are Lendbox, i2ifunding, Faircent etc. One can expect around 9.69% return on investment on average seasoned return.

National Savings Certificate (NSC): With the minimum of ₹ 100 deposit, the investor can choose the tenure of deposit as either 5 years or 10 years, the rate of interest on the investment differs as per the tenure. The rate of return on this is about 7.9% as of the year 2017 and maximum ₹ 150,000 tax returns can be filed on the same.

Senior Citizen Savings Scheme (SCSS): With the rate of interest close of 8.4%, this is the best investment option for those who are 60+ years. This investment is a tax-free investment. Any person is more that 60n years can invest in SCSS through the post office. It offers maximum benefits and maximum returns with minimal investment.

Bank Fixed Deposit: Banks fixed deposits are one of the widely accepted traditional ways of investment. The interest rate and norms may very bank to bank. The interest rate is different for general investors and senior citizen investors. One can invest for a minimum of 7 days and a maximum of 10 years. The return on this investment is 6.75% for 30-day FD scheme, 7.5% for deposit period of 60 to 90 days, 7.75% and 8% for 120- days and 6 months deposit term, respectively.

Sukanya Samriddhi Yojana: One of the great investment options for the parents of a girl child. This is mainly for future benefits of your daughter either for her education or wedding. The return on this investment is about 8.1% per annum.

These are the most popular and minimal risk associated investment options available in India. Investing any of these schemes will bring high return but to get that high return one must invest. Whether a personal loan for investment is a good idea or not can be gauged by checking the given points.

Check the Loan Rates

The basic objective of availing the loan is to earn a profit by investing. So before availing the loan, one must check the interest rate of the loan. The interest rate on the personal loan must be lower than your gain from the investment. One can earn profit only if he has to pay less and earn more.

Study Investment Performance

Before investing one must check the performance of the previous years. Some of the investments such as stocks and mutual funds which give high return comes with high risk of capital loss. So one must do quality research before jumping into the stock market especially when the investment is done with the borrowed money.

Review the Fees

As interest rates of a personal loan bring your profit down, there is another culprit too who will eat up your profit. The next profit consumer is 'Fees'. One has to pay fees to the lender in various names such as processing fee, documentation charges, stamp duty charges etc to the lender. Actually, if a person buys stocks from an online buyer, you have to pay trade commission every time you complete a transaction. Even for investing in mutual funds too one has to pay management fees.

A personal loan for investment may be a risky business but in another hand, the profit of a business is the reward of taking risks only Taking some calculated risk possibly bring you profit in the best scenario. One must do good research on investment plans to earn a profit by investing borrowed money.

#personal loans#personal loan for investment#online personal loans#apply for a personal loan#personal loan without documents

0 notes

Text

List of Income Tax Deductions FY 2020-21 – Under New / Old Tax Regime

Due to the introduction of new tax regime in the Budget 2020, many are not confused which are the Income Tax Deductions are available for them. Let us see the complete list of Income Tax Deductions FY 2020-21 under both old or new tax regime.

Tax Planning is an important part of financial planning. However, while investing or choosing the deductions, our idea should be to concentrate at first on our financial goals rather than just concentrating on tax saving. Hence, understanding the available options is very much important.

Income Tax Slab Rates for FY 2020-21 AY 2021-22

You may be aware that during Budget 2020, Government introduced the two types of tax regimes. As per that, the income tax slabs are as below.

List of Income Tax Deductions FY 2020-21 – Under New / Old Tax Regime

Let us now discuss the list of income tax deductions FY 2020 – 21. I will divide them as new and old tax regime for your simplicity.

List of Income Tax Deductions FY 2020-21 under New Tax Regime

I have already written a detailed post on this, where I mentioned that which deductions are not available under new tax regime. You can refer the same at “New Tax Regime – Complete list of exemptions and deductions not allowed“. In this post, I am concentrating on the available deductions.

# Section 80CCD(2)

Under this section, employer contribution on account of the employee in notified pension schemes like EPF, NPS, and/or Super Annuation Account can be claimed up to Rs.7.5 lakh limit.

An employer can contribute an amount equal to 12% of the employee’s basic monthly salary to his/her EPF account. Similarly, an employer can contribute an amount equal to 10% of the employee’s basic salary to the Tier-I account of NPS (For Central Government Employees it is now 14% of Basic+DA effective from 1st April 2019). In a superannuation account, an employer can contribute a maximum of Rs 1.5 lakh exempted from tax in a financial year.

Refer the detailed post on NPS Tax Benefits at “NPS Tax Benefits 2020 – Sec.80CCD(1), 80CCD(2) and 80CCD(1B)“.

The Budget 2020 restricted the tax-exempt superannuation, NPS and EPF account contribution by the employer to maximum of Rs 7.5 lakh in a financial year. Further, the budget states that any interest or gains earned from the excess contribution will also be taxable in the hands of an employee.

# Section 10(15)(i)

Interest received on post office savings account balance is exempted up to Rs 3,500 under section 10(15)(i) of the Income-tax Act. The exemption limit is Rs.7,000 in case of joint savings account.

# Gratuity

Gratuity is tax-exempt up to Rs 20 lakh in a lifetime for non-government employees. For government employees, all gratuity received is tax-exempt, irrespective of the amount received by them. (Refer my post “Gratuity – New Limit, Eligibility, Formula, Taxation and Calculator“)

Below benefits up to certain threshold limits (if any) are allowed under new tax regime as well;

Commutation of pension

Leave encashment on retirement

Retrenchment compensation

VRS benefits

NPS withdrawal benefits

Education scholarships

Payments of awards instituted in the public interest

# Interest on EPF Account, SSY and PPF

The interest received from the EPF account continues to be exempted from tax in the new tax regime as well as the old tax regime.

The Interest and maturity amount received on the Sukanya Samriddhi account, PPF account are tax-free in both old and new tax regimes.

# Sect.87A

Individuals having taxable income of up to Rs.5 lakh will be eligible for tax rebate under section 87A up to Rs 12,500, thereby making zero tax payable in the new tax regime.

# Conveyance Allowance

You can claim income tax exemption for conveyance, travel, and other allowances given by your employers under the new tax regime as well.

List of Income Tax Deductions FY 2020-21 under Old Tax Regime

Let us now discuss the list of income tax deductions FY 2020-21 under the old tax regime. Before proceeding further, first, let us understand the difference between deductions and exemptions.

Exemption :- It is nothing but an income which is not subject to tax. There are certain exemptions which are applicable only towards certain heads of income. Hence, you have to be cautious while claiming such exemptions.

There are mainly five sources of incomes which IT Department categorized and they are Salary income, Business of Professional Income, Income from House Property, Income from Capital Gains and Income from Other Sources.

Take for example like HRA, Gratuity can be claimed as tax-exempt against your salary income. Agriculture income, dividend income, or Sec.54 of IT act against long term capital gains on the sale of the property.

Deductions:-

Income Tax Deductions means you may deduct the amount that is eligible for reducing your tax liability. Income Tax Deductions can be deducted from the Gross Total Income. There are various options of investing or expenditure, which can be claimed as Tax Deductions.

Allowances available under old tax regime:-

# Mobile/Telephone Reimbursement

If your employer offering you the mobile/telephone connection or internet connection which requires for work, then you can claim 100% of such cost. However, you have to produce a bill. Only the postpaid connections are allowed for reimbursement.

# Leave Travel Allowance

The bills for your travel against LTA can be claimed for exemption. It is allowed to be claimed twice in a block of four years. The current block is 2014 to 2017. You can carry forward your unclaimed LTA to the next year. You can request your employer to not deduct tax on it and allow you to claim it next year.

# Entertainment Allowances

You may be getting this allowance. However, the exemption is available only for Government employees. The amount of exemption is least of the following.

a) Rs 5,000

b) 1/5th of salary (excluding any allowance, benefits or other perquisites)

c) Actual entertainment allowance received

# House Rent Allowance (HRA)

This is the famous exemption which is used by many salaried individuals. However, the wrong belief is that whatever the rent they pay is actually exempted from their income. The reality is different. The amount of exemption is least of the following.

a) Actual HRA Received

b) 40% of Salary (50%, if house situated in Mumbai, Calcutta, Delhi or Madras)

c) Rent paid minus 10% of salary

(Salary= Basic + DA (if part of retirement benefit) + Turnover based Commission)

# Children Education Allowance

If your employer providing this allowance, then you can take exemption up to Rs.100 per month per child (maximum of up to 2 children). Therefore, monthly you can save Rs.200 from this allowance. The exemption may seem so low. But why to pay the tax?

# Hostel Expenditure Allowance-If your employer providing this allowance, then you can take exemption Up to Rs. 300 per month per child up to a maximum of 2 children is exempt. Therefore, you can save around a maximum of Rs.600 from this allowance.

# Conveyance Allowance

This is a different allowance than a transport allowance. It is the expenditure granted to an employee to meet the expenses on conveyance in performing his official duties. There is no limit for this. If such conveyance allowance is Rs.5,000 a month, then the whole allowance is exempt. Hence, you may this may be exempt to the extent of expenditure incurred for official purposes.

# Any Allowance to meet the cost of travel on tour or on transfer

Here also no limit. The employee can claim exempt to the extent of expenditure incurred for official purposes.

# Allowance to meet the cost of travel on tour or on transfer

Here also no limit. The employee can claim exempt to the extent of expenditure incurred for official purposes.

# Daily Allowance

If you are not placed in normal duty place, then your employer may provide you such allowance. The employee can claim exempt to the extent of expenditure incurred for official purposes.

These are the major allowances, which can be utilized to save tax on salary income. There are few other allowances also to claim the exemption. But many of such allowances are not so famous. Hence, I left them to list.

Deductions available under old tax regime:-

The complete of sections can be listed as below.

# Standard Deduction of Rs.50,000

Actually, I have to put this under Deductions. However, this standard deduction replaced the existing allowances. Hence, I placed it here for better understanding.

Earlier you used to claim Rs.15,000 under Medical Allowance and Travel Allowance. With effect from FY 2018-19, you can claim the direct Rs.40,000 deduction instead of these two allowances. However, the same is increased now to Rs.50,000 from FY 2019-20 and the same is applicable for FY 2020-21.

This deduction obviously for salaried and pensioners. This is irrespective of the amount of taxable salary you will be receiving to get a deduction of Rs.50,000 or taxable salary, whichever is less.

Hence, let us assume for FY 2019-20, you worked only for a few days. Your taxable salary is Rs.50,000. In such a scenario, you can directly claim the deduction of Rs.50,000. However, if your salary is less than Rs.40,000 (say Rs.20,000), then you have to claim only Rs.20,000 but not Rs.50,000.

# Section 80C

This is the famous section which often used by all of salaried. The maximum limit for the current year is Rs.1,50,000. Therefore, up to Rs.1,50,000, you can save tax on salary income from this section alone. The different investments you do and can also be claimed under Sec.80C are listed below.

Life Insurance premium (Paid by an individual, spouse, and child. In the case of HUF, on the life of any member of HUF).

EPF-Employee contribution can be claimed for deduction.

Public Provident Fund (Paid by an individual, spouse, and child. In the case of HUF, on the life of any member of HUF).

National Savings Certificate (NSC).

Sukanya Samriddhi Account

ELSS or Tax Saving Mutual Funds.

Senior Citizen Savings Scheme.

5-Years Post Office or Bank Deposits.

The tuition fee of kids.

Principal payment towards the home loan.

Stamp duty and registration cost of the house.

Any contribution towards NPS Tier 2 Account by Government employees is also eligible for deductions under Sec.80C.

# Sec.80CCC

Deduction under Sec.80CCC is available only for individuals. Contribution to an annuity plan of the LIC of India or any other insurer for receiving the pension. Do remember that the amount should be paid or deposited out of income chargeable to tax.

The maximum amount deductible under Sec.80CCC is Rs.1.5 lakh. Do remember that this is also the part of the combined limit of Rs.1.5 lakh available under Sec.80C, Sec.80CCC, and Sec.80CCD(1).

# Sec.80CCD1

The maximum benefit available is Rs.1.5 lakh (including Sec.80C limit).

An individual’s maximum 20% of annual income (Earlier it was 10% but after Budget 2017, it increased to 20%) or an employees (10% of Basic+DA) contribution will be eligible for deduction.

As I said above, this section will form the part of Sec.80C limit.

# Sec.80CCD2

There is a misconception among many that there is no upper limit for this section. However, the limit is least of 3 conditions. 1) Amount contributed by an employer, 2) 10% of Basic+DA (14% of Government Employees) and 3) Gross Total Income.

This is an additional deduction which will not form the part of Sec.80C limit.

The deduction under this section will not be eligible for self-employed.

NPS Tax Benefits under Sec.80CCD (1B)

This is the additional tax benefit of up to Rs.50,000 eligible for an income tax deduction and was introduced in the Budget 2015

Introduced in Budget 2015. One can avail the benefit of this Sect.80CCD (1B) from FY 2015-16.

Both self-employed and employees are eligible for availing this deduction.

This is over and above Sec.80CCD (1).

I explained all three sections of NPS (Sec.80CCD1, Sec.80CCD2 and Sec.80CCD(1B) in below image for your reference.

You can also refer my latest post on the changes “NPS Tax Benefits 2019 – Sec.80CCD(1), 80CCD(2) and 80CCD(1B)“.

NOTE:- PLEASE NOTE THAT THE COMBINED LIMIT OF DEDUCTION UNDER SEC.80C, SEC.80CCC AND SEC.80CCD(1) TOGETHER CAN NOT EXCEED RS.1,50,000 FOR FY 2020-21.

#Sec.80D

Deduction under this section is available if you satisfy the following conditions.

The taxpayer should be an individual (resident, NRI or Foreign Citizen) or HUF.

Payment should be made out of income chargeable to tax.

Payment should be in NON-CASH mode (for preventive health check up, you can pay either through cash or non-cash mode).

Changes from Budget 2018-

In Budget 2018, the maximum tax deduction limit for senior citizens under Sec.80D is raised to Rs.50,000. The earlier limit was Rs.30,000.

In case of single premium health insurance policies having a cover of more than one year, it is proposed that the deduction shall be allowed on a proportionate basis for the number of years for which health insurance cover is provided, subject to the specified monetary limit.

I will try to summarize the whole benefit from the below image.

# Sec.80DD

A resident individual or HUF is allowed to claim the deduction under Sec.80DD. You can claim the deduction if you incurred an expenditure for medical treatment, training, and rehabilitation of dependent relative (being a person with a disability).

A deduction can also be claimed if an individual or HUF deposited or paid for any approved scheme of LIC (or any other insurance) or UTI for the maintenance of such a dependent relative.

Here, dependent means spouse, children, parents, brothers, and sisters, who is wholly and mainly dependent upon the individual.

You can claim fixed duction of Rs.75,000 under this section. A higher deduction of Rs.1,25,000 is available if such dependent relative is suffering from severe disability.

# Sec.80DDB

An Individual’s of HUFs expenses actually paid for medical treatment of specified diseases and ailments subject to certain conditions can be claimed under this section.

The maximum deduction is Rs. 40,000. This can also be claimed on behalf of the dependents. The tax deduction limit under this section for Senior Citizens and very Senior Citizens (above 80 years) is now revised to Rs 1,00,000.

With effect from the assessment year 2016-17, the taxpayer shall be required to obtain a prescription from a specialist doctor (not necessarily from a doctor working in a Government hospital) for availing this deduction.

You can claim the deduction for the medical treatment of self, spouse, children, parents brothers, and sisters of the individual.

The ailments covered under this section are as below.

# Neurological Diseases where the disability level has been certified to be of 40% and above;

(a) Dementia

(b) Dystonia Musculorum Deformans

(c) Motor Neuron Disease

(d) Ataxia

(e) Chorea

(f) Hemiballismus

(g) Aphasia

(h) Parkinson’s Disease

# Malignant Cancers

# Full Blown Acquired Immuno-Deficiency Syndrome (AIDS) ;

# Chronic Renal Failure

# Hematological disorders

a) Hemophilia

b) Thalassemia

# Sec.80E

An individual can claim deduction under Sec.80E. If the loan is taken by an individual for any study in India or outside India, then they can claim the deduction. The interest part of the loan on such education loan can be claimed for the deduction for pursuing individual’s own education or for the education of his relatives (Spouse, children or any student for whom the individual is a legal guardian).

The entire interest is deductible in the year in which the individual starts to pay interest on the loan and subsequent 7 years or until interest is paid in full (i.e for a total 8 years). But do remember that interest should be paid out of the income of chargeable to tax.

# Sec.80EEA

Along with tax deductions under Section 80C and 24b, an individual can claim up to Rs 1.5 lakh under Section 80EEA from FY 2019-20. The same is continued for FY 2020-21. However, there are certain conditions are there for the same, and they are as below:-

The home loan should have been sanctioned between 1st April, 2019 to 31st March 2020.

The Stamp duty value of the property should not exceed 45 Lakhs.

Taxpayer should not own any other residential property on the date of loan sanction.

This tax benefit will be available from 1st April 2020 (AY 2020-21) and till the end of the home loan tenure (closure).

The total interest deduction is now Rs. 3.5 lakh (Rs 2 Lakh +

Rs 1.5 Lakh).

Note that the deduction under Section 80EEA is available for home loans from banks and approved financial institutions only. To claim tax benefit under Section 24, you should have received possession of your house (interest paid before possession is eligible for deduction over the next 5 years in 5 equal installments). Section 80EEA do not impose any requirement of possession or completion of construction. Therefore, Section 80EEA provides you immediate tax relief even if you have purchased an under-construction property.

Both resident Indians and non-resident Indians (NRIs) can claim the deduction u.s 80EEA.

Section 80EEB

A Tax deduction of up to Rs 1.5 lakh can be claimed on Interest paid on Loans taken to purchase Electronic Vehicles.

# Sec.80G

Donations to certain approved funds, trusts, charitable institutions/donations for renovation or repairs of notified temples, etc can be claimed as a deduction under this section. This deduction can only be claimed when the contribution made by cheque or draft or in cash. In-kind contributions like food material, clothes, medicines etc. do not qualify for deduction under this section.

The donations made to any Political party can be claimed under section 80GGC.

From FY 2017-18, the limit of deduction under section 80G / 80GGC for donations made in cash is reduced from current Rs 10,000 to Rs 2,000 only.

If you wish to donate to any political party of your choice, then you are allowed to donate up to Rs.2,000 only in cash. However, if you wish to donate more than Rs.2,000, then you can donate it using Electoral Bonds.

# Sec.80GG

I have written a complete post on this section. Refer “Section 80GG Deduction-Get Tax Benefit on rent paid if not getting HRA !!!“. I will give you a brief about this section as below.

This section only applies to those who have not availed HRA in their salary or not claiming the deduction on their rent in any of the other sections of income tax. Below are a few conditions to avail the deduction under this section.

This section is only applicable to Individual or HUF.

Taxpayers may be either salaried or self-employed. However, must not be getting HRA.

Tax Payer himself or spouse/Minor Child/HUF of which he is a member should not own any accommodation at a place where he is doing a job or business.

If Tax Payer owns a house at a place other than the place noted above, then the concession in respect of the self-occupied property is not claimed by him [Under Section 23 (2) (a) or 23 (4) (a)].

Tax Payer has to file a declaration in Form No.10BA regarding the expenditure incurred by him towards the payment of rent.

How much amount of deduction one can avail under Sec. 80GG?

If the above five conditions are satisfied, the amount deductible under Section 80GG is LEAST OF THE FOLLOWING.

Rs.5, 000 per month;

25% of total income of taxpayer for the year; or

Rent Paid less 10% of total income (Rent Paid-10% of Total Income).

# Sec.80TTA

A deduction of up to Rs.10,000 can be claimed by an individual or HUB in respect of any income by the way of interest from a savings account with a bank, from a savings account with a co-operative society carrying on the business of banking or from a savings account with a post office but from FDs, RDs or other Term Deposits). From FY 2018-19, this benefit will not be available for late Income Tax filers.