improve-credit-score-in-usa

Credit Repair Ease

25 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

anuardayan

Anuar Sánchez

sleepydollie

♡♡♡

mymonsterthoughts

My Monster Thoughts

if-songs-were-prophecies-gl-blog

If songs were Prophecies, I´d Write a Perfect End

neonlamb

NEON LAMB

Text

Achieve Financial Freedom: Elevating Your Credit Score in Spokane, WA

In this digital age, your credit score plays a pivotal role in your financial life. Lenders, landlords, and even potential employers often rely on credit scores to assess your creditworthiness. By taking proactive steps to improve your credit score, you can unlock a world of financial opportunities and achieve long-term stability.

Understanding Credit Scores

A credit score is a three-digit number that reflects your creditworthiness based on various factors. These factors include your payment history, credit utilization, length of credit history, credit mix, and new credit applications. The most commonly used credit scoring model is the FICO score, which ranges from 300 to 850. The higher your credit score, the more favorable terms and conditions you can expect when borrowing money.

Assessing Your Current Credit Score

Before you begin your journey to elevate your credit score, it's important to assess your starting point. You can obtain a free copy of your credit report from each of the three major credit bureaus: Equifax, Experian, and TransUnion. Analyze the report carefully, looking for any errors or discrepancies that may be impacting your score negatively.

Reviewing Your Credit Report

Once you have your credit report in hand, review it thoroughly. Look for any late payments, outstanding debts, or negative marks that may be dragging down your score. Note down any areas that require attention or disputes for potential resolution.

Identifying Areas for Improvement

Based on your credit report analysis, identify the areas that need improvement. These may include paying off outstanding debts, resolving any collection accounts, or addressing past-due payments. By pinpointing these areas, you can develop a targeted strategy to address each issue systematically.

Creating a Budget and Payment Plan

One of the key factors that impact your credit score is your payment history. Creating a budget and payment plan can help you stay organized and ensure that your bills are paid on time. List all your monthly expenses and prioritize your debt payments to avoid missing any due dates.

Paying Bills on Time

Consistently paying your bills on time is vital for improving your credit score. Late payments can have a significant negative impact on your creditworthiness. Set up automatic payments or reminders to ensure you never miss a due date. Over time, your punctuality will reflect positively on your credit report.

Reducing Credit Card Debt

High credit card balances can harm your credit utilization ratio, which is the percentage of available credit you're currently using. Aim to keep your credit utilization below 30% and focus on paying down your balances. Consider strategies like the snowball or avalanche method to accelerate debt repayment.

Avoiding New Credit Applications

Each time you apply for new credit, it generates a hard inquiry on your credit report, which can lower your score. Avoid unnecessary credit applications, especially if you're actively working on improving your credit. Instead, focus on managing and improving your existing credit accounts.

Building a Positive Credit History

The length of your credit history is an important factor in determining your credit score. Building a positive credit history takes time and responsible credit management. Keep your oldest credit accounts open and active, as they contribute to the overall length of your credit history.

Using Secured Credit Cards

If you're starting from scratch or have a limited credit history, secured credit cards can be a valuable tool. Secured credit cards require a cash deposit as collateral, making them accessible to individuals with lower credit scores. Use the card responsibly, making timely payments, and maintaining a low credit utilization to establish a positive credit history.

Seeking Professional Assistance

If you find yourself overwhelmed or unsure about the steps to improve your credit, consider seeking professional assistance. Credit counseling agencies and financial advisors can provide guidance tailored to your unique situation. They can help you develop a personalized plan and navigate the complexities of credit repair.

Monitoring Your Progress

As you implement the strategies mentioned above, it's essential to monitor your progress regularly. Keep track of your credit score, review your updated credit reports, and ensure that any resolved issues are accurately reflected. By staying vigilant, you can ensure that your credit score continues to improve over time.

Patience and Persistence

Rome wasn't built in a day, and the same applies to your credit score. Improving your credit requires patience, persistence, and consistent effort. Understand that it's a journey and that positive changes may not happen overnight. Stay focused on your goals and celebrate each milestone along the way.

Conclusion

Elevating your Credit score in Spokane, WA, is a crucial step towards achieving financial freedom. By understanding the factors that influence your credit score and implementing the strategies outlined in this article, you can take control of your financial future. Remember, it's never too late to start building a strong credit foundation and opening doors to greater opportunities.

FAQs

1. How long does it take to improve my credit score?

Improving your credit score is a gradual process and can take several months or even years. It depends on your starting point and the actions you take to address any issues.

2. Can I improve my credit score on my own, or do I need professional help?

You can improve your credit score on your own by following the strategies outlined in this article. However, if you feel overwhelmed or need personalized guidance, seeking professional help is a viable option.

3. Will paying off my debts automatically improve my credit score?

Paying off your debts is a positive step that can improve your credit score over time. However, other factors, such as your payment history and credit utilization, also play a role in determining your score.

4. How often should I review my credit report?

It's recommended to review your credit report at least once a year. However, if you're actively working on improving your credit, you may want to check it more frequently to monitor your progress.

5. Can I erase negative marks from my credit report?

If there are errors or inaccuracies on your credit report, you have the right to dispute them. However, legitimate negative marks resulting from past financial mistakes or delinquencies cannot be erased but will gradually have less impact on your score over time.

Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

#creditconsult#creditrepairservices#howtomakemoneywithcredit#creditconsulting#consumercredit#creditcounseling

0 notes

Text

Unlocking Financial Insights: Exploring Credit Analysis in Reno, NV

In today's rapidly evolving financial landscape, credit analysis plays a pivotal role in assessing the creditworthiness of individuals and businesses. This article delves into the world of credit analysis, focusing specifically on its application in Reno, NV. By understanding the key aspects of credit analysis and its impact on financial decision-making, individuals and businesses can unlock valuable insights that will shape their financial strategies.

Understanding Credit Analysis

Credit analysis involves the evaluation of an individual or entity's creditworthiness, assessing their ability to fulfill financial obligations and repay borrowed funds. It encompasses a comprehensive analysis of various factors, including credit history, income, debt levels, and overall financial stability. By examining these elements, credit analysts provide valuable insights that assist lenders, investors, and financial institutions in making informed decisions.

The Importance of Credit Analysis in Reno, NV

Reno, NV, is a thriving economic hub, attracting individuals and businesses alike. As the local economy flourishes, credit analysis becomes increasingly crucial for both lenders and borrowers. For lenders, understanding the creditworthiness of potential borrowers mitigates risks associated with default or non-payment. On the other hand, borrowers benefit from credit analysis as it helps them secure favorable loan terms, lower interest rates, and gain access to financial opportunities that can fuel their growth.

Factors Considered in Credit Analysis

Credit analysis involves a comprehensive evaluation of various factors that contribute to an individual's or business's creditworthiness. These factors include:

1. Credit History

A person or business's credit history provides valuable insights into their past borrowing behavior, repayment patterns, and overall credit management. Credit analysts review credit reports, analyzing factors such as payment history, outstanding debts, and the length of credit history to assess creditworthiness accurately.

2. Income and Debt Levels

The income and debt levels of individuals and businesses play a significant role in credit analysis. Credit analysts evaluate income stability, debt-to-income ratios, and overall financial obligations to gauge an individual's or business's ability to manage their financial commitments.

3. Financial Stability and Assets

Assessing financial stability and assets helps credit analysts evaluate the overall financial health of individuals and businesses. Factors such as savings, investments, and the presence of collateral provide a clearer picture of an entity's ability to manage financial obligations and repay debts.

4. Industry and Economic Factors

Credit analysis also considers industry-specific and economic factors that may influence creditworthiness. For businesses, factors such as market conditions, competition, and regulatory environment are taken into account to assess their ability to sustain operations and meet financial obligations.

Credit Analysis Process

The credit analysis process involves several stages, ensuring a thorough assessment of an individual's or business's creditworthiness. The key steps include:

Gathering Information: Credit analysts collect relevant financial data, credit reports, and supporting documents to build a comprehensive understanding of the borrower's financial situation.

Financial Statement Analysis: The financial statements, including income statements, balance sheets, and cash flow statements, are carefully examined to assess financial stability, profitability, and cash flow generation.

Ratio Analysis: Various financial ratios, such as debt-to-equity ratio, liquidity ratio, and profitability ratios, are calculated to gauge the borrower's financial performance and risk levels.

Credit Score Evaluation: Credit analysts analyze credit scores, considering factors such as payment history, credit utilization, and credit inquiries to determine the borrower's creditworthiness.

Risk Assessment: Credit analysts assess the overall risk associated with extending credit to the borrower, considering both internal and external factors that may impact repayment capacity.

Decision Making: Based on the comprehensive analysis, credit analysts make recommendations or decisions regarding credit approval, loan terms, and interest rates.

Key Players in Credit Analysis

Several key players are involved in the credit analysis process, contributing their expertise and insights. These include:

Credit Analysts: These professionals specialize in evaluating creditworthiness, conducting in-depth analyses, and providing recommendations based on their findings.

Lenders and Financial Institutions: Lenders and financial institutions utilize credit analysis to assess risk levels and make informed lending decisions.

Credit Rating Agencies: Credit rating agencies assign credit ratings to individuals, businesses, and financial instruments, providing an independent assessment of creditworthiness.

Regulatory Bodies: Regulatory bodies establish guidelines and regulations that govern credit analysis practices, ensuring transparency, and fair assessment.

Evaluating Credit Scores

Credit scores are a numerical representation of an individual's creditworthiness, providing a quick assessment of their credit history and risk levels. Lenders and financial institutions rely on credit scores to make lending decisions. Factors such as payment history, credit utilization, length of credit history, and types of credit are considered in calculating credit scores. A higher credit score indicates lower credit risk, leading to favorable loan terms and interest rates.

Credit Analysis for Individuals

For individuals, credit analysis plays a crucial role in various financial aspects of life. It affects the ability to secure loans for homes, cars, or education, and can impact interest rates on credit cards and personal loans. By maintaining a good credit score and demonstrating responsible credit management, individuals can unlock financial opportunities, obtain better loan terms, and build a strong foundation for their financial future.

Credit Analysis for Businesses

Credit analysis is equally important for businesses, especially when seeking funding or entering into partnerships. Potential lenders and investors rely on credit analysis to evaluate a company's financial health, stability, and ability to meet financial obligations. A positive credit analysis can open doors to favorable loan terms, partnerships, and opportunities for growth and expansion.

Benefits of Effective Credit Analysis

Effective credit analysis offers several benefits to both individuals and businesses, including:

Enhanced Borrowing Power: A favorable credit analysis increases borrowing power and provides access to financial resources that fuel growth and achieve financial goals.

Lower Interest Rates: Good creditworthiness translates into lower interest rates on loans and credit cards, saving money over time.

Improved Financial Decision-making: Credit analysis provides insights that aid in making informed financial decisions, mitigating risks, and maximizing financial opportunities.

Enhanced Reputation: Positive credit analysis builds a strong reputation and instills confidence among lenders, investors, and business partners.

Challenges in Credit Analysis

Credit analysis faces certain challenges that impact the accuracy and effectiveness of assessments. These challenges include:

Lack of Complete Information: Obtaining complete and accurate financial information can be challenging, especially when dealing with individuals or businesses with complex financial structures.

Subjectivity in Analysis: The interpretation of financial data and creditworthiness involves a degree of subjectivity, which may result in variations in assessments.

Dynamic Economic Environment: Economic conditions and market fluctuations can impact creditworthiness, making it essential to consider external factorsthat may influence credit analysis.

Limited Historical Data: For individuals or businesses with limited credit history, it can be challenging to assess creditworthiness accurately.

Evolving Industry Practices: Credit analysis needs to adapt to changing industry practices, emerging technologies, and evolving financial instruments.

Emerging Trends in Credit Analysis

Credit analysis is subject to ongoing advancements and emerging trends that shape the industry. Some notable trends include:

Big Data and AI: The use of big data and artificial intelligence (AI) enables credit analysts to analyze vast amounts of information, identify patterns, and make more accurate predictions.

Alternative Credit Scoring Models: Traditional credit scoring models are being complemented by alternative models that consider non-traditional data sources, such as utility payments, rental history, or social media behavior.

Risk-Based Pricing: Lenders are increasingly adopting risk-based pricing models, where interest rates and loan terms are tailored based on the borrower's credit risk, offering more personalized lending options.

Enhanced Fraud Detection: Advanced analytics and fraud detection algorithms help identify potential fraud patterns, reducing risks associated with fraudulent activities.

Role of Technology in Credit Analysis

Technology plays a vital role in streamlining and enhancing credit analysis processes. Various technological tools and platforms assist credit analysts in gathering, analyzing, and interpreting financial data. Automation, machine learning, and data visualization tools enable quicker and more accurate assessments, improving efficiency and decision-making.

Enhancing Financial Decision-making

Credit analysis significantly impacts financial decision-making for individuals and businesses. By leveraging credit analysis insights, individuals can make informed decisions regarding borrowing, managing debts, and improving credit scores. Businesses can utilize credit analysis to assess partnerships, secure funding, and evaluate investment opportunities. With enhanced financial decision-making, individuals and businesses can achieve their goals and navigate the financial landscape more effectively.

Future Outlook of Credit Analysis

The future of credit analysis holds promising opportunities and challenges. Advancements in technology, data analytics, and risk assessment methodologies will continue to shape the industry. The integration of alternative data sources and the use of predictive analytics will provide deeper insights into creditworthiness. However, regulatory compliance, data privacy, and the ethical use of data will also remain key considerations for credit analysis practices.

Conclusion

Credit analysis is a crucial aspect of financial decision-making, enabling individuals and businesses to unlock valuable insights into creditworthiness. In Reno, NV, credit analysis plays a vital role in facilitating access to financial resources, mitigating risks, and fostering economic growth. By understanding the key components and processes involved in credit analysis, individuals and businesses can make informed financial decisions, secure favorable loan terms, and navigate the dynamic financial landscape with confidence.

FAQs (Frequently Asked Questions)

1. How long does credit analysis take?

Credit analysis timelines can vary depending on the complexity of the borrower's financial situation and the availability of required information. It can range from a few days to several weeks.

2. Can credit analysis impact credit scores?

No, credit analysis itself does not impact credit scores. However, credit analysis assesses factors that contribute to credit scores, such as payment history, credit utilization, and overall credit management.

3. Are there alternatives to traditional credit scoring models?

Yes, alternative credit scoring models are gaining traction, which consider non-traditional data sources and provide a broader view of an individual's creditworthiness.

4. What happens if I have a poor credit analysis?

A poor credit analysis may result in limited access to financial resources, higher interest rates, and less favorable loan terms. However, it is possible to improve creditworthiness over time with responsible credit management.

5. How often should individuals or businesses undergo credit analysis?

Regular credit analysis is recommended, especially when seeking new credit opportunities or entering into significant financial transactions. It helps individuals and businesses stay aware of their creditworthiness and make necessary improvements if needed. Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

0 notes

Text

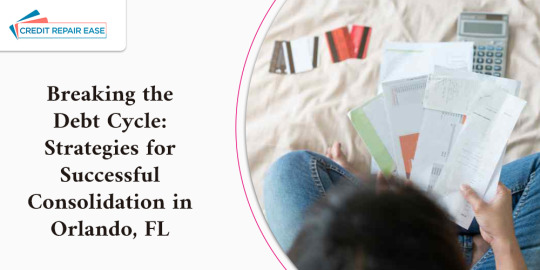

Breaking the Debt Cycle: Strategies for Successful Consolidation in Orlando, FL

Debt can easily spiral out of control, causing financial stress and hindering your ability to achieve your goals. If you're struggling with multiple debts in Orlando, FL, debt consolidation can be a powerful tool to break free from the debt cycle and regain control of your finances. This comprehensive guide will explore strategies for successful debt consolidation in Orlando, providing you with the necessary information to make informed decisions about your financial well-being.

Understanding the Debt Cycle

The debt cycle refers to the pattern of accumulating debt to cover expenses, struggling to make minimum payments, and incurring high interest charges. This cycle can trap individuals in a never-ending loop, making it challenging to become debt-free. Understanding the factors contributing to the debt cycle is crucial in finding effective solutions.

Benefits of Debt Consolidation

Debt consolidation offers numerous advantages for individuals burdened by multiple debts. Here are some key benefits:

1. Simplified Repayment

By consolidating your debts, you can streamline multiple payments into a single monthly installment. This simplifies your financial obligations and makes it easier to keep track of your progress.

2. Lower Interest Rates

Debt consolidation can potentially secure a lower interest rate, especially if you have high-interest credit card debts. By reducing interest charges, more of your payment goes toward reducing the principal balance.

3. Potential Debt Reduction

In some cases, debt consolidation can lead to a reduction in the overall amount you owe. Through negotiations with creditors or debt settlement, you may be able to lower the total debt burden, making it more manageable to repay.

Types of Debt Consolidation

There are several debt consolidation strategies available to individuals in Orlando, FL. Understanding the different types can help you choose the most suitable approach for your financial situation. Here are a few common options:

1. Personal Loan

Obtaining a personal loan from a bank, credit union, or online lender allows you to consolidate your debts into a single loan. Personal loans often have fixed interest rates and a structured repayment plan.

2. Balance Transfer

A balance transfer involves moving high-interest credit card balances to a new credit card with a lower or 0% introductory interest rate. This strategy can help save on interest charges during the promotional period.

3. Home Equity Loan or Line of Credit

Homeowners in Orlando, FL, may consider utilizing their home equity to consolidate debts. A home equity loan or line of credit allows you to borrow against the equity in your home, potentially providing lower interest rates.

Choosing a Debt Consolidation Strategy

When selecting a debt consolidation strategy, it's important to consider your specific financial circumstances. Factors such as interest rates, repayment terms, and eligibility requirements should be evaluated. It's advisable to consult with a financial advisor or debt consolidation specialist to determine the best approach for your needs.

Finding a Reliable Debt Consolidation Provider in Orlando, FL

Working with a reputable debt consolidation provider is crucial to the success of your consolidation efforts. Take the time to research and compare providers in Orlando, FL. Look for companies with a solid reputation, positive customer reviews, and transparent fee structures. Verify their accreditation and licensing to ensure their legitimacy.

The Debt Consolidation Process

The process of debt consolidation typically involves the following steps:

1. Evaluation

A debt consolidation provider will assess your financial situation, including your debts, income, and credit score. This evaluation helps them determine the most suitable consolidation plan for your specific needs.

2. Application and Approval

Once you've chosen a provider, you'll need to complete an application for the consolidation loan or program. The provider will review your application and, if approved, provide you with the details of the consolidation terms.

3. Debt Settlement and Repayment

After approval, the debt consolidation provider will negotiate with your creditors on your behalf to settle your debts. Once settlements are reached, you'll make a single monthly payment to the provider, who will distribute the funds to your creditors.

Debt Consolidation in Orlando, FL

Residents of Orlando, FL, have access to various resources for debt consolidation. Local banks, credit unions, and financial institutions offer personal loans and consolidation programs. Research and compare the available options to find the most suitable one for your financial needs.

Factors to Consider Before Consolidating Debt

Before consolidating your debts, consider the following factors:

1. Total Debt Amount

Evaluate your total debt to determine if debt consolidation is the right solution for you. Some lenders have minimum and maximum debt requirements.

2. Interest Rates and Fees

Compare the interest rates and fees associated with your current debts and the consolidation method. Ensure that the consolidation option provides better terms and helps you save money.

3. Credit Score

Your credit score plays a significant role in qualifying for a debt consolidation loan or program. Understand the minimum credit score requirements and take steps to improve your credit if needed.

Steps to Take After Consolidating Debt

Successfully consolidating your debts is just the beginning. To ensure long-term financial stability, follow these steps:

1. Create a Budget

Develop a comprehensive budget to manage your income and expenses effectively. Allocate funds for debt repayment and track your progress towards becoming debt-free.

2. Improve Financial Habits

Avoid falling back into debt by practicing responsible financial habits. Limit unnecessary expenses, save for emergencies, and avoid new credit card debt.

Common Misconceptions About Debt Consolidation

There are some common misconceptions surrounding debt consolidation. Let's address a few:

1. Debt Consolidation Eliminates Debt

Debt consolidation does not erase your debt. It provides a structured plan to manage and repay your debts more efficiently.

2. Debt Consolidation Hurts Credit Score

While applying for debt consolidation may initially impact your credit score, responsible debt management and timely payments can improve your credit score over time.

Frequently Asked Questions (FAQs)

Q1. Can debt consolidation help me become debt-free?

A1. Debt consolidation provides a structured approach to managing and paying off your debts. With discipline and commitment, it can help you become debt-free.

Q2. Will debt consolidation affect my credit score?

A2. Applying for a debt consolidation loanmay have a temporary impact on your credit score. However, consolidating and repaying your debts responsibly can have a positive long-term effect on your credit score.

Q3. Is debt consolidation suitable for all types of debt?

A3. Debt consolidation is generally suitable for unsecured debts such as credit card debt, personal loans, and medical bills. However, it may not be ideal for certain types of debts like student loans or tax debt.

Q4. Will debt consolidation lower my monthly payments?

A4. Debt consolidation can potentially lower your monthly payments by extending the repayment period or securing a lower interest rate. However, it's important to consider the overall cost of the loan over time.

Q5. How long does the debt consolidation process take?

A5. The duration of the debt consolidation process can vary depending on factors such as the complexity of your debts and the chosen consolidation method. It can range from a few months to several years.

Conclusion

If you find yourself trapped in the debt cycle, debt consolidation can be an effective strategy to break free and regain control of your finances. By simplifying your debts and potentially reducing interest rates, debt consolidation offers a path towards becoming debt-free. Evaluate your options, choose a reliable debt consolidation provider, and consider the factors specific to your situation in Orlando, FL. Call us today for more information at (888) 803-7889 or click here to visit our website.

#creditconsult#creditreportreviews#howtomakemoneywithcredit#creditreportdisputes#creditrepairservice

0 notes

Text

Reclaim Your Financial Health: Strategies for Bad Credit Repair in Cincinnati, OH

Having bad credit can have a significant impact on your financial well-being. It can make it challenging to secure loans, obtain favorable interest rates, and even affect your housing and employment prospects. If you find yourself in Cincinnati, OH, with bad credit, it's essential to take proactive steps to repair it. This article will provide you with strategies and insights to help you reclaim your financial health by repairing your bad credit.

Understanding the Importance of Credit Health

What is Credit Health?

Credit health refers to the state of your creditworthiness. It is assessed based on your credit history, credit scores, and other factors that lenders and creditors use to evaluate your ability to manage debt and repay loans.

Why is Credit Health Important?

Maintaining good credit health is crucial because it affects your ability to access credit and favorable financial opportunities. Good credit health can lead to lower interest rates, higher credit limits, and more favorable loan terms.

Assessing Your Credit Situation

To begin the process of repairing bad credit, start by assessing your current credit situation. Review your credit reports, analyze your credit scores, and identify any negative items or areas that need improvement. Understanding the extent of your bad credit will help you develop an effective plan.

Checking Your Credit Reports

Obtain copies of your credit reports from the major credit bureaus—Equifax, Experian, and TransUnion. Review each report carefully to ensure accuracy and identify any discrepancies, such as incorrect personal information or unauthorized accounts. Pay close attention to negative items, such as late payments or collections.

Identifying and Disputing Errors on Your Credit Reports

If you spot errors on your credit reports, such as inaccuracies or fraudulent accounts, it's crucial to dispute them promptly. Contact the credit bureaus in writing, providing supporting documentation to validate your claims. The bureaus are required to investigate and correct any errors found within a certain timeframe.

Paying Off Outstanding Debts

One of the most effective ways to repair bad credit is by paying off outstanding debts. Prioritize debts with the highest interest rates or those in collections. Create a repayment plan and allocate extra funds towards debt reduction. Making consistent payments will gradually improve your credit score and demonstrate responsible financial behavior.

Creating a Realistic Budget

Developing a realistic budget is essential for managing your finances and repairing bad credit. Assess your income and expenses, including debt payments, utilities, and daily living costs. Allocate funds for debt repayment and savings. Stick to your budget to avoid further credit issues and establish a solid financial foundation.

Establishing Positive Credit Habits

Building positive credit habits is vital for long-term credit repair. Make all payments on time, including bills, loans, and credit card balances. Keep your credit utilization ratio low by using only a small percentage of your available credit. Avoid opening unnecessary new accounts and maintain a responsible credit utilization pattern.

Seeking Professional Assistance

If youfind the credit repair process overwhelming or need expert guidance, consider seeking professional assistance. Credit counseling agencies and reputable credit repair companies can provide personalized advice, help you navigate the complexities of credit repair, and negotiate with creditors on your behalf.

Being Patient and Persistent

Repairing bad credit is not an overnight process. It requires patience and persistence. Keep in mind that it takes time for positive changes to reflect in your credit reports and scores. Stay committed to your credit repair strategies, continue practicing good financial habits, and be patient with the progress.

Frequently Asked Questions

Q1: Can I repair bad credit on my own, or do I need professional help?

A1: You can repair bad credit on your own with the right knowledge and strategies. However, professional help can provide expertise and guidance, especially if you feel overwhelmed or uncertain about the process.

Q2: How long does it take to repair bad credit?

A2: The time required to repair bad credit varies for each individual and depends on the severity of the credit issues. Significant improvements can be seen within several months to a year with consistent effort.

Q3: Will paying off my debts improve my credit score?

A3: Paying off debts can have a positive impact on your credit score, especially if they are in collections or have high balances. It demonstrates responsible financial behavior and reduces your overall debt burden.

Q4: Can I remove negative items from my credit report?

A4: If negative items on your credit report are accurate, they cannot be removed. However, you can dispute any errors or fraudulent information to have them corrected or removed.

Q5: Will closing unused credit accounts help improve my credit score?

A5: Closing unused credit accounts may have a negative impact on your credit score. It can decrease your available credit and potentially shorten your credit history. It's generally advisable to keep old accounts open and maintain a responsible credit utilization ratio.

Conclusion

Repairing bad credit in Cincinnati, OH, is a proactive step towards reclaiming your financial health. By understanding the importance of credit health, assessing your credit situation, disputing errors on your credit reports, paying off debts, creating a realistic budget, and establishing positive credit habits, you can gradually rebuild your credit. Remember to be patient, seek professional assistance when needed, and practice good financial habits consistently. With dedication and persistence, you can overcome bad credit and pave the way for a brighter financial future.

Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

#creditreportreviews#identitytheftrecovery#creditrepairservice#creditcounseling#creditreportcorrection#businesscreditreports

0 notes

Text

Reclaim Your Financial Health: Strategies for Bad Credit Repair in Cincinnati, OH

Having bad credit can have a significant impact on your financial well-being. It can make it challenging to secure loans, obtain favorable interest rates, and even affect your housing and employment prospects. If you find yourself in Cincinnati, OH, with bad credit, it's essential to take proactive steps to repair it. This article will provide you with strategies and insights to help you reclaim your financial health by repairing your bad credit.

Understanding the Importance of Credit Health

What is Credit Health?

Credit health refers to the state of your creditworthiness. It is assessed based on your credit history, credit scores, and other factors that lenders and creditors use to evaluate your ability to manage debt and repay loans.

Why is Credit Health Important?

Maintaining good credit health is crucial because it affects your ability to access credit and favorable financial opportunities. Good credit health can lead to lower interest rates, higher credit limits, and more favorable loan terms.

Assessing Your Credit Situation

To begin the process of repairing bad credit, start by assessing your current credit situation. Review your credit reports, analyze your credit scores, and identify any negative items or areas that need improvement. Understanding the extent of your bad credit will help you develop an effective plan.

Checking Your Credit Reports

Obtain copies of your credit reports from the major credit bureaus—Equifax, Experian, and TransUnion. Review each report carefully to ensure accuracy and identify any discrepancies, such as incorrect personal information or unauthorized accounts. Pay close attention to negative items, such as late payments or collections.

Identifying and Disputing Errors on Your Credit Reports

If you spot errors on your credit reports, such as inaccuracies or fraudulent accounts, it's crucial to dispute them promptly. Contact the credit bureaus in writing, providing supporting documentation to validate your claims. The bureaus are required to investigate and correct any errors found within a certain timeframe.

Paying Off Outstanding Debts

One of the most effective ways to repair bad credit is by paying off outstanding debts. Prioritize debts with the highest interest rates or those in collections. Create a repayment plan and allocate extra funds towards debt reduction. Making consistent payments will gradually improve your credit score and demonstrate responsible financial behavior.

Creating a Realistic Budget

Developing a realistic budget is essential for managing your finances and repairing bad credit. Assess your income and expenses, including debt payments, utilities, and daily living costs. Allocate funds for debt repayment and savings. Stick to your budget to avoid further credit issues and establish a solid financial foundation.

Establishing Positive Credit Habits

Building positive credit habits is vital for long-term credit repair. Make all payments on time, including bills, loans, and credit card balances. Keep your credit utilization ratio low by using only a small percentage of your available credit. Avoid opening unnecessary new accounts and maintain a responsible credit utilization pattern.

Seeking Professional Assistance

If youfind the credit repair process overwhelming or need expert guidance, consider seeking professional assistance. Credit counseling agencies and reputable credit repair companies can provide personalized advice, help you navigate the complexities of credit repair, and negotiate with creditors on your behalf.

Being Patient and Persistent

Repairing bad credit is not an overnight process. It requires patience and persistence. Keep in mind that it takes time for positive changes to reflect in your credit reports and scores. Stay committed to your credit repair strategies, continue practicing good financial habits, and be patient with the progress.

Frequently Asked Questions

Q1: Can I repair bad credit on my own, or do I need professional help?

A1: You can repair bad credit on your own with the right knowledge and strategies. However, professional help can provide expertise and guidance, especially if you feel overwhelmed or uncertain about the process.

Q2: How long does it take to repair bad credit?

A2: The time required to repair bad credit varies for each individual and depends on the severity of the credit issues. Significant improvements can be seen within several months to a year with consistent effort.

Q3: Will paying off my debts improve my credit score?

A3: Paying off debts can have a positive impact on your credit score, especially if they are in collections or have high balances. It demonstrates responsible financial behavior and reduces your overall debt burden.

Q4: Can I remove negative items from my credit report?

A4: If negative items on your credit report are accurate, they cannot be removed. However, you can dispute any errors or fraudulent information to have them corrected or removed.

Q5: Will closing unused credit accounts help improve my credit score?

A5: Closing unused credit accounts may have a negative impact on your credit score. It can decrease your available credit and potentially shorten your credit history. It's generally advisable to keep old accounts open and maintain a responsible credit utilization ratio.

Conclusion

Repairing bad credit in Cincinnati, OH, is a proactive step towards reclaiming your financial health. By understanding the importance of credit health, assessing your credit situation, disputing errors on your credit reports, paying off debts, creating a realistic budget, and establishing positive credit habits, you can gradually rebuild your credit. Remember to be patient, seek professional assistance when needed, and practice good financial habits consistently. With dedication and persistence, you can overcome bad credit and pave the way for a brighter financial future. Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

0 notes

Text

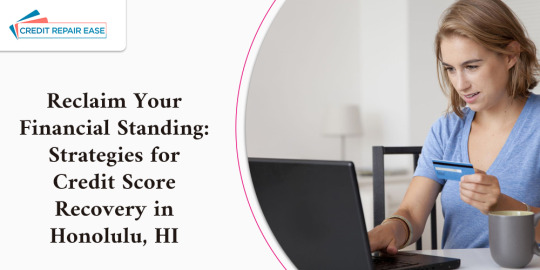

Reclaim Your Financial Standing: Strategies for Credit Score Recovery in Honolulu, HI

Having a good credit score is essential for financial stability and the ability to access loans and credit cards on favorable terms. However, life circumstances and financial challenges can sometimes lead to a decline in credit scores. If you find yourself in such a situation in Honolulu, HI, don't lose hope. This article will provide you with effective strategies to reclaim your financial standing and improve your credit score. By implementing these strategies, you can regain control of your financial health and pave the way for a brighter future.

Understanding Credit Scores

Before diving into credit score recovery strategies, it's important to understand how credit scores work. A credit score is a numerical representation of an individual's creditworthiness, ranging from 300 to 850. Lenders use this score to assess the risk of lending money to someone. Factors such as payment history, credit utilization, length of credit history, types of credit, and new credit applications influence your credit score.

Assessing Your Credit Report

To start the credit score recovery process, obtain a copy of your credit report from the major credit bureaus. Review it carefully for any errors, inaccuracies, or fraudulent accounts. Dispute any incorrect information and ensure that your report reflects accurate details.

Creating a Budget and Reducing Expenses

Developing a budget is crucial for managing your finances effectively. Track your income and expenses, and identify areas where you can reduce unnecessary spending. By cutting back on non-essential expenses, you can allocate more funds towards debt repayment and improving your credit score.

Paying Bills on Time

Consistently paying your bills on time is one of the most impactful actions you can take to recover your credit score. Late payments can have a significant negative impact on your creditworthiness. Set up reminders or automate payments to avoid missing due dates.

Clearing Existing Debts

Focus on clearing existing debts, especially high-interest ones, to reduce your debt-to-income ratio. Consider using the debt snowball or debt avalanche method to prioritize repayment. Make regular payments and aim to pay more than the minimum amount due whenever possible.

Debt Consolidation

If you have multiple debts with high interest rates, debt consolidation may be a viable option. This involves combining multiple debts into a single loan or credit card with a lower interest rate. Debt consolidation simplifies repayment and can save you money on interest charges.

Secured Credit Cards

Secured credit cards can be a valuable tool for credit score recovery. These cards require a cash deposit as collateral, which acts as your credit limit. By using a secured credit card responsibly and making timely payments, you can demonstrate positive credit behavior and gradually improve your credit score.

Building Positive Credit History

Building a positive credit history is essential for long-term credit score improvement. Make small purchases using credit and pay them off in full each month. Additionally, consider becoming an authorized user on someone else's credit card with a good payment history to benefit from their positive credit behavior.

Seeking Professional Assistance

If you're overwhelmed or unsure about the best course of action, seeking professional assistance can be beneficial. Credit counseling agencies and financial advisors can provide guidance tailored to your specific situation. They can help you create a personalized plan for credit score recovery and offer valuable insights and strategies.

Avoiding Credit Repair Scams

Be cautious of credit repair scams that promise quick and miraculous results. Legitimate credit repair takes time and effort. Avoid any company or individual that guarantees instant credit score improvement or asks for upfront fees. Research and choose reputable credit repair services, if needed.

Patience and Persistence

Credit score recovery is not an overnight process. It requires patience and persistence. Stay committed to your financial goals, follow your repayment plan, and make responsible credit decisions. Over time, you will see gradual improvements in your credit score.

Reaping the Benefits of Credit Score Recovery

As your credit score improves, you'll enjoy several benefits. You'll have better access to loans, mortgages, and credit cards with favorable terms and lower interest rates. Additionally, you'll gain greater financial freedom and the ability to achieve your long-term goals.

Conclusion

Reclaiming your financial standing and improving your credit score in Honolulu, HI is an achievable goal. By following the strategies outlined in this article, such as assessing your credit report, creating a budget, paying bills on time, clearing debts, and building positive credit history, you can make significant progress. Remember, it's a journey that requires commitment and patience, but the rewards are well worth it.

FAQs

1. How long does it take to recover a credit score?

The time it takes to recover a credit score varies depending on individual circumstances. It can take several months to a few years of consistent effort and responsible credit behavior.

2. Can I improve my credit score on my own, or do I need professional help?

Improving your credit score is something you can do on your own. However, professional help from credit counseling agencies or financial advisors can provide valuable guidance and support.

3. Will paying off all my debts instantly improve my credit score?

While paying off debts is beneficial, the impact on your credit score may not be immediate. It takes time for the positive effects to reflect in your credit history.

4. Are there any quick fixes to improve my credit score overnight?

Beware of any claims for quick fixes or instant credit score improvements. Legitimate credit score improvement takes time and consistent effort.

5. Can I negotiate with creditors to remove negative items from my credit report?

It is possible to negotiate with creditors to remove negative items, but there are no guarantees. It's best to focus on responsible credit behavior and working towards a positive credit history.

Call us today for more information at (888) 803-7889 or click here to visit our website.

#creditrestoration#creditrepair#creditconsult#creditreportreviews#identitytheftrecovery#creditrepairservice

0 notes

Text

Overcoming Credit Challenges and Recovering Your Score in Colorado Springs, CO

In today's financial landscape, credit scores play a significant role in various aspects of our lives, such as obtaining loans, securing favorable interest rates, or even renting an apartment. Unfortunately, credit challenges can arise due to various reasons, such as missed payments, high credit utilization, or bankruptcy. However, with the right approach and determination, you can overcome these challenges and work towards rebuilding your credit score.

Understanding Credit Scores

Before diving into the process of overcoming credit challenges, it's essential to understand how credit scores work. Your credit score is a numerical representation of your creditworthiness and is typically calculated based on your credit history, including factors such as payment history, credit utilization, length of credit history, and types of credit accounts.

Assessing Your Current Credit Situation

To begin your journey towards credit recovery, it's crucial to assess your current credit situation. Obtain a copy of your credit report from major credit bureaus like Equifax, Experian, or TransUnion. Review the report carefully, identifying any errors, discrepancies, or negative items that may be impacting your credit score.

Identifying Credit Challenges

Once you have assessed your credit situation, it's time to identify the specific credit challenges you are facing. These challenges could include late payments, high credit card balances, collections accounts, or even a history of bankruptcy. By understanding the root causes of your credit issues, you can develop an effective plan to address them.

Creating a Debt Repayment Plan

One of the most critical steps in overcoming credit challenges is creating a debt repayment plan. Start by prioritizing your debts based on interest rates and amounts owed. Consider implementing strategies such as the snowball method or the avalanche method to tackle your debts systematically. Make consistent payments and avoid missing any future due dates.

Utilizing Credit-Building Tools

Building or rebuilding credit requires the responsible use of credit. Consider applying for a secured credit card or becoming an authorized user on someone else's credit card. Use these tools wisely, making small purchases and paying them off in full and on time. Over time, this will demonstrate your ability to manage credit responsibly and positively impact your credit score.

Working with Credit Counseling Agencies

If you feel overwhelmed or need professional guidance, credit counseling agencies can provide valuable assistance. These agencies offer services such as personalized financial counseling, debt management plans, and educational resources to help you navigate your credit challenges effectively.

Addressing Negative Credit History

Negative items on your credit report can significantly impact your credit score. If you come across any inaccuracies or outdated information, dispute them with the respective credit bureaus. For legitimate negative items, focus on building positive credit history moving forward, as the impact of negative items decreases over time.

Establishing Good Credit Habits

Improving your credit score and maintaining it requires the development of good credit habits. Pay your bills on time, keep your credit utilization low, and avoid applying for unnecessary credit. Consistency in these habits will gradually improve your creditworthiness and contribute to a higher credit score.

Monitoring Your Progress

Regularly monitor your credit progress by checking your credit reports and scores. Many credit monitoring services are available that provide you with access to your credit information, alerts for any significant changes, and educational resources to help you stay on track. Monitoring your progress allows you to identify areas of improvement and celebrate milestones as you recover your credit score.

Seeking Professional Help

In complex credit situations, seeking professional help may be the best course of action. Credit repair companies specialize in assisting individuals with credit challenges. However, be cautious and do thorough research before engaging with any credit repair service to ensure they are reputable and provide genuine assistance.

The Importance of Patience and Persistence

Recovering your credit score is not an overnight process. It requires patience and persistence. Understand that improving your credit takes time and consistent effort. Stay committed to your debt repayment plan, credit-building strategies, and good credit habits. Over time, you will see positive results and a healthier credit profile.

Conclusion

Overcoming credit challenges and recovering your Credit score in Colorado Springs, CO, is possible with the right mindset and actions. By following the steps outlined in this article, you can take control of your financial future and work towards a better credit standing. Remember to be patient, persistent, and proactive in your credit journey, and always seek guidance from reputable sources when needed.

Frequently Asked Questions (FAQs)

FAQ 1: How long does it take to recover a credit score?

The time it takes to recover a credit score depends on various factors, such as the severity of the credit challenges and the actions taken to address them. Generally, it can take several months to a few years to see significant improvements in your credit score.

FAQ 2: Can I improve my credit score on my own?

Yes, you can improve your credit score on your own by implementing the strategies mentioned in this article. However, if you feel overwhelmed or need professional guidance, seeking assistance from reputable credit counseling agencies or credit repair companies can be beneficial.

FAQ 3: Are there any quick fixes for a low credit score?

No, there are no quick fixes for a low credit score. Rebuilding your credit requires time, consistent effort, and responsible credit management. Be cautious of any services or claims that promise instant credit score improvements.

FAQ 4: Will paying off old debts improve my credit score?

Paying off old debts can positively impact your credit score. It demonstrates responsible financial behavior and reduces your overall debt burden. However, keep in mind that the impact may vary based on individual circumstances and the specific details of your credit history.

FAQ 5: Should I close unused credit accounts?

Closing unused credit accounts can potentially harm your credit score. It reduces your overall available credit and may increase your credit utilization ratio. Instead of closing accounts, consider keeping them open and using them responsibly to maintain a healthy credit mix.

Give us a call today at (888) 803-7889.

#creditutilization#increasingyourcreditlimit#Payingoffyourcollections#creditscore#creditgoals#businessdebtassistance

0 notes

Text

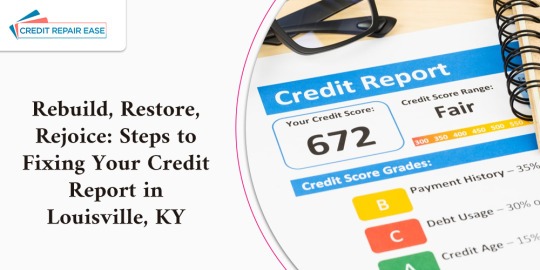

Rebuild, Restore, Rejoice: Steps to Fixing Your Credit Report in Louisville, KY

Your credit report is a comprehensive summary of your credit history, including information about your payment habits, outstanding debts, and credit inquiries. It is essential to have a healthy credit report to enjoy financial stability and access to favorable credit opportunities. In this article, we will explore the steps you can take to Fix your credit report in Louisville, KY, and improve your overall creditworthiness.

Understanding Your Credit Report

Before diving into the process of fixing your credit report, it is crucial to understand its components. Your credit report consists of various sections, including personal information, account history, public records, and inquiries. Familiarize yourself with these sections to gain a comprehensive understanding of your credit standing.

Assessing Your Credit Situation

The first step in repairing your credit report is to assess your current credit situation. Obtain a copy of your credit report from one of the major credit bureaus and carefully review it for any errors or discrepancies. Make a note of any negative items, such as late payments, defaults, or collections, as these will require specific attention during the repair process.

Disputing Inaccurate Information

If you identify any inaccuracies or incorrect information on your credit report, it is essential to dispute them promptly. Contact the credit bureaus in writing, providing detailed explanations and supporting documentation to back up your claims. The credit bureaus are obligated to investigate and correct any errors within a reasonable timeframe.

Paying Off Outstanding Debts

Addressing outstanding debts is a crucial step in repairing your credit report. Create a strategy to pay off your debts systematically, starting with those that have the highest interest rates or are in collections. Consider negotiating with creditors for a favorable settlement or setting up payment plans to make the process more manageable.

Building Positive Credit History

To rebuild your credit, it is important to demonstrate responsible credit behavior. Start by making timely payments on your existing credit accounts. If you don't have any active credit, consider opening a secured credit card or becoming an authorized user on someone else's credit card to establish positive credit history.

Utilizing Secured Credit Cards

Secured credit cards are an excellent tool for rebuilding credit. With a secured credit card, you provide a security deposit, which becomes your credit limit. Use the card responsibly, making small purchases and paying off the balance in full each month. Over time, this will help improve your credit score.

Managing Credit Utilization Ratio

Your credit utilization ratio is the percentage of your available credit that you are currently using. Aim to keep your credit utilization below 30% to demonstrate responsible credit management. Avoid maxing out your credit cards or carrying high balances, as this can negatively impact your credit score.

Creating a Budget and Sticking to It

Developing a budget is essential for maintaining healthy financial habits. Track your income and expenses to ensure you have a clear understanding of your financial situation. Allocate funds for essential expenses, debt repayment, and savings. By sticking to a budget, you can avoid overspending and reduce financial stress.

Seeking Professional Assistance

If you find the credit repair process overwhelming or need expert guidance, consider seeking professional assistance. Credit counseling agencies and reputable credit repair companies can provide valuable insights, personalized advice, and strategies tailored to your unique situation.

Monitoring Your Progress

As you embark on your credit repair journey, it is important to monitor your progress regularly. Keep track of your credit score and review your credit reports periodically to ensure that the changes you have made are reflected accurately. Celebrate small victories along the way, as every positive step contributes to a stronger credit profile.

The Importance of Patience and Persistence

Repairing your credit takes time and effort. It is crucial to maintain patience and persistence throughout the process. Understand that rebuilding your credit is a marathon, not a sprint. Stay committed to your financial goals, make responsible credit choices, and embrace the positive changes you are making in your financial life.

Conclusion

Fixing your credit report in Louisville, KY, is an achievable goal with the right strategies and mindset. By following the steps outlined in this article, you can rebuild and restore your credit, paving the way for a brighter financial future. Remember to stay informed, take proactive measures, and remain patient as you work towards improving your creditworthiness.

FAQs (Frequently Asked Questions)

Q1. How long does it take to fix a credit report?

A1. The time required to fix a credit report can vary depending on the complexity of your situation. It may take several months or even years to fully repair your credit. However, with consistent effort and responsible credit behavior, you can start seeing improvements within a few months.

Q2. Can I fix my credit report on my own, or do I need professional help?

A2. While you can fix your credit report on your own, professional help can provide valuable guidance and expertise. Credit counseling agencies and reputable credit repair companies can offer personalized strategies and assist you in navigating the process effectively.

Q3. Will fixing my credit report automatically improve my credit score?

A3. Repairing your credit report is a crucial step towards improving your credit score. However, other factors, such as payment history, credit utilization, and length of credit history, also influence your credit score. By addressing all aspects of your credit, you can work towards a better credit score.

Q4. Can I remove accurate negative information from my credit report?

A4. Accurate negative information, such as missed payments or defaults, generally cannot be removed from your credit report. However, it will have less impact over time as you build a positive credit history. Focus on making timely payments and establishing good credit habits to mitigate the effects of negative information.

Q5. How often should I check my credit reports?

A5. It is recommended to check your credit reports at least once a year. Regular monitoring allows you to detect any errors or fraudulent activities promptly. You can obtain free copies of your credit reports from each of the major credit bureaus once every 12 months.

Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

#CreditLawyer#Payingoffyourcollections#Creditcounseling#creditkarma#creditrepairservices#creditrestoration

0 notes

Text

Achieve Financial Freedom: Elevating Your Credit Score in Columbus, OH

Are you looking to achieve financial freedom and improve your credit score in Columbus, Ohio? Having a good credit score is crucial for various aspects of your financial life, from securing loans and credit cards to obtaining favorable interest rates. In this article, we will explore practical strategies and tips to help you elevate your credit score and take control of your financial future.

Understanding Credit Scores

Before delving into the steps to improve your credit score, it's essential to understand what a credit score is and how it affects your financial standing. A credit score is a numerical representation of your creditworthiness, ranging from 300 to 850. The higher your credit score, the more likely you are to be approved for loans and credit with favorable terms.

Assessing Your Current Credit Situation

The first step towards elevating your credit score is to assess your current credit situation. Obtain a copy of your credit report from the major credit bureaus - Equifax, Experian, and TransUnion. Review the report for any errors or inaccuracies that could be negatively impacting your score. Dispute any incorrect information and ensure that your credit report reflects accurate data.

Creating a Budget and Payment Plan

A crucial aspect of improving your credit score is managing your finances responsibly. Create a comprehensive budget that outlines your monthly income and expenses. Identify areas where you can cut back on unnecessary spending and allocate more funds towards paying off debts.

Develop a payment plan that prioritizes timely payments on all your bills and debts. Late or missed payments can significantly impact your credit score. Set up automatic payments or reminders to ensure you stay on track with your payment schedule.

Managing Credit Card Debt

Credit card debt can be a significant hurdle in elevating your credit score. Develop a strategy to tackle your outstanding balances effectively. Consider the snowball or avalanche method to pay off your debts systematically. The snowball method involves paying off the smallest balance first, while the avalanche method focuses on paying off debts with the highest interest rates.

It's important to keep your credit card balances low and avoid maxing out your cards. Aim to keep your credit utilization ratio below 30%. Pay more than the minimum payment each month, if possible, to accelerate debt repayment.

Building a Positive Credit History

Building a positive credit history is vital for improving your credit score in the long term. Make sure to pay all your bills, including utilities and rent, on time. Consider opening a secured credit card or becoming an authorized user on someone else's account to establish or rebuild credit.

Diversify your credit mix by having different types of credit, such as credit cards, auto loans, or mortgages. However, be cautious and avoid taking on excessive debt that you cannot comfortably manage.

Utilizing Credit-Boosting Techniques

Several techniques can help boost your credit score. Consider contacting your creditors to negotiate lower interest rates or request a goodwill adjustment for any late payments. Additionally, you can explore the option of credit counseling, debt consolidation, or debt settlement if you're struggling to manage your debts effectively.

Another effective method is becoming an authorized user on a credit card with a positive payment history. This can potentially improve your credit score by piggybacking on the account owner's responsible credit behavior.

Monitoring Your Credit Regularly

Regularly monitoring your credit is essential for identifying any changes or potential issues promptly. Take advantage of the free annual credit reports provided by the major credit bureaus. You can also sign up for credit monitoring services that alert you to any significant changes or suspicious activity on your credit report.

Seeking Professional Guidance

If you find it challenging to navigate the complexities of credit improvement on your own, don't hesitate to seek professional guidance. Credit counseling agencies and financial advisors can provide valuable insights and personalized strategies to help you achieve your credit goals.

Conclusion

Achieving financial freedom starts with elevating your credit score in Columbus, OH. By following the steps outlined in this article, you can take control of your financial future and open doors to better opportunities. Remember to stay disciplined, make responsible financial decisions, and consistently monitor and improve your credit score over time.

FAQs

1. How long does it take to improve a credit score?

The time it takes to improve a credit score varies depending on individual circumstances. With consistent effort and responsible financial habits, you can start seeing improvements in as little as a few months. However, significant changes may take longer, and it's important to be patient and persistent.

2. Will closing unused credit cards improve my credit score?

Closing unused credit cards can potentially impact your credit score negatively. It reduces your overall available credit and can increase your credit utilization ratio. It's generally advisable to keep unused credit cards open, especially if they have a long credit history and no annual fees.

3. Can I improve my credit score if I have a bankruptcy on my record?

While bankruptcy has a significant impact on your credit score, it's not permanent. With time, responsible financial behavior, and a positive credit history, you can rebuild your credit score even after bankruptcy. It's important to focus on improving your credit habits and gradually demonstrate your creditworthiness.

4. How often should I check my credit score?

It's recommended to check your credit score at least once a year by obtaining your free annual credit reports. However, if you're actively working on improving your credit or have concerns about identity theft, it's beneficial to monitor your credit more frequently, such as through a credit monitoring service.

5. Can I hire a credit repair company to improve my credit score?

While there are credit repair companies that claim to improve your credit score, it's important to exercise caution. Some companies may engage in unethical practices or charge high fees for services you can do yourself. It's advisable to research and choose reputable organizations, or consider working directly with credit counseling agencies or financial advisors for guidance.

Call today at (888) 803-7889 for a free consultation. We look forward to helping you, Bloom!

0 notes

Text

Empower Your Finances: Exploring Credit Counseling Services in Chicago, IL

In the bustling city of Chicago, IL, many individuals face financial challenges that can impact their overall well-being. From overwhelming debt to low credit scores, these financial burdens can create stress and hinder progress towards financial stability. However, there is a solution available: credit counseling services. This article aims to shed light on the benefits of credit counseling services in Chicago and how they can empower you to regain control of your finances and improve your financial future.

Understanding Credit Counseling

Credit counseling is a professional service designed to assist individuals in managing their finances effectively. Credit counselors are trained experts who assess your financial situation, provide personalized guidance, and develop strategies to address your specific financial challenges.

Assessing Your Financial Situation

The first step in credit counseling is a thorough assessment of your financial situation. Credit counselors will review your income, expenses, debts, and credit history to gain a comprehensive understanding of your financial health. This assessment helps identify the root causes of your financial difficulties and enables credit counselors to provide tailored advice.

Creating a Personalized Financial Plan

Based on the assessment, credit counselors create a personalized financial plan that aligns with your goals and addresses your financial challenges. This plan may include strategies such as debt consolidation, budgeting techniques, and prioritizing debt repayment. A personalized financial plan sets you on the path towards financial stability and empowers you to make informed financial decisions.

Developing Effective Budgeting Strategies

Credit counseling services in Chicago emphasize the importance of budgeting. Credit counselors work with you to develop effective budgeting strategies that align with your income, expenses, and financial goals. By implementing a budget, you gain better control over your finances, track your spending, and ensure that you can meet your financial obligations.

Debt Management and Negotiation

Credit counseling services play a vital role in helping you manage and reduce your debt. Credit counselors negotiate with your creditors on your behalf to secure lower interest rates, reduced monthly payments, and potential waivers of late fees. They help you develop a debt management plan that outlines a structured approach to paying off your debts efficiently.

Improving Credit Scores

A low credit score can limit your financial opportunities and hinder your ability to obtain favorable loans or secure housing. Credit counseling services provide guidance on improving your credit score. By implementing effective credit management strategies and addressing negative items on your credit report, you can work towards rebuilding your credit and achieving a healthier credit score.

Providing Financial Education

Credit counseling services go beyond immediate financial assistance. They offer valuable financial education resources, workshops, and counseling sessions to enhance your financial literacy. These educational resources cover topics such as budgeting, savings, credit management, and responsible financial practices. By empowering you with knowledge, credit counselors equip you with the tools needed to make sound financial decisions.

Building Long-Term Financial Health

Credit counseling services focus not only on addressing immediate financial challenges but also on building long-term financial health. Credit counselors provide ongoing support, monitoring your progress, and adjusting your financial plan as needed. They help you establish good financial habits, set realistic goals, and develop a solid foundation for a brighter financial future.

Finding Reputable Credit Counseling Services in Chicago

To benefit from credit counseling services, it is important to find reputable and reliable providers in Chicago. Start by researching accredited credit counseling agencies that have a track record of success. Look for client testimonials, reviews, and certifications to ensure you choose a reputable service provider. Additionally, consider their expertise in handling specific financial challenges that align with your needs.

Frequently Asked Questions (FAQs)

What is credit counseling?

Credit counseling is a professional service that helps individuals manage their finances, address debt-related issues, and improve their overall financial well-being.

How can credit counseling services help with debt management?

Credit counseling services can assist with debt management by providing strategies such as debt consolidation, negotiation with creditors, and developing structured debt repayment plans.

Will credit counseling services affect my credit score?

Credit counseling services themselves do not directly impact credit scores. However, by following the guidance and strategies provided by credit counselors, you can improve your credit score over time.

How long does credit counseling take?

The duration of credit counseling varies depending on your unique financial situation. It may take several months to a few years to complete the program successfully. The duration is determined by your commitment and the complexity of your financial challenges.

How do I find reliable credit counseling services in Chicago?

To find reliable credit counseling services in Chicago, research accredited agencies, read client reviews and testimonials, and ensure that the agency adheres to ethical practices. It is also beneficial to seek recommendations from trusted sources.

Conclusion

Credit counseling services in Chicago offer a lifeline to individuals grappling with financial challenges. By providing personalized financial plans, effective budgeting strategies, debt management assistance, and financial education, credit counseling services empower you to take control of your finances. They pave the way for long-term financial health and help you build a stronger, more secure financial future. If you're facing financial difficulties in Chicago, consider seeking the assistance of credit counseling services to transform your financial life.

Give us a call today at (888) 803-7889.

0 notes

Text

The Power of 680: Supercharge Your Finances in St. Louis, MO

Are you a resident of St. Louis, MO, looking to take control of your financial future? One crucial aspect that can significantly impact your financial standing is your credit score. A credit score of 680 holds immense power and can supercharge your finances, opening up a world of opportunities. In this article, we will explore the importance of a 680 credit score, the benefits it brings, and how you can harness its power to transform your financial life in St. Louis. Let's dive in!

Understanding the Significance of a Credit Score

In today's financial landscape, your credit score plays a vital role in determining your financial health and opportunities. It serves as a numerical representation of your creditworthiness, reflecting your ability to handle credit and repay debts. A credit score of 680 is considered good and can open doors to favorable financial prospects in St. Louis.

What is a Credit Score?

A credit score is a three-digit number that lenders use to assess your creditworthiness. It is calculated based on various factors such as payment history, credit utilization, length of credit history, credit mix, and new credit applications. The higher your credit score, the more financially trustworthy you appear to potential lenders.

Factors Affecting Your Credit Score

Several factors influence your credit score. These include your payment history, amounts owed, length of credit history, types of credit used, and recent credit applications. Understanding these factors empowers you to make informed decisions to improve your creditworthiness.

The Impact of a 680 Credit Score

A credit score of 680 holds significant impact when it comes to your financial life in St. Louis. It positions you favorably as a reliable borrower, increasing your chances of obtaining favorable interest rates, higher credit limits, and improved loan approval rates.

Benefits of a 680 Credit Score

Access to Better Interest Rates

One of the primary benefits of a 680 credit score is the ability to access loans and credit cards with better interest rates. Lenders view individuals with higher credit scores as less risky, resulting in lower interest rates on credit products.

Increased Loan Approval Chances

With a credit score of 680, you enhance your prospects of loan approvals. Whether you're looking to finance a car, purchase a home, or start a business in St. Louis, having a good credit score makes you a more attractive candidate to lenders.

Higher Credit Limits

A 680 credit score can lead to higher credit limits on your credit cards. This increased credit capacity offers you greater flexibility in managing your finances and handling unexpected expenses.

Favorable Insurance Premiums

Insurance companies often consider credit scores when determining premiums for auto, home, or rental insurance. With a credit score of 680, you may be eligible for lower insurance premiums, saving you money in the long run.

Rental and Housing Opportunities