Last Seen Blogs

paleo-pines

Paleo Pines

celestialnxva

yours truly, lady whistledown

thaomoc

Untitled

danishubhi

Untitled

savwotome

"Y/N?"ᵒᵗᵒᵐᵉ

Text

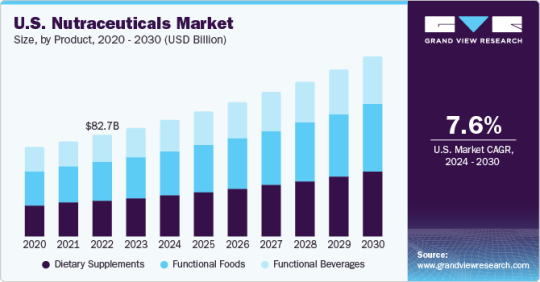

Nutraceuticals Market Is Expected To Grow Swiftly By 2030

The global nutraceuticals market size is projected to reach USD 599.71 billion by 2030, according to a new report by Grand View Research, Inc. The market is anticipated to grow at a CAGR of 9.6% from 2024 to 2030. Rising awareness regarding calorie reduction and weight loss in the major markets including the U.S., China, and India is expected to promote the application of the health and wellness segment and thus, in turn, will have a substantial impact on the industry.

Nutraceuticals are products that provide health advantages and additional nutrition to the human body. It comprises fortified nutrients, such as taurine, CoQ10, omega-3, calcium, zinc, and antioxidants, that develop the complete health of consumers. These nutrients further benefit in averting medical conditions such as hypertension, diabetes, heart diseases, and allergies. As nutraceuticals develop the digestive and immune systems and enhance the cognitive behavior of consumers, their demand is witnessing a surge at the global level.

The increasing trend among consumers to alter dietary habits is likely to boost the demand for nutraceuticals. The consumer belief that improper diet results in an increase in the costs of pharmaceuticals is anticipated to boost the demand for nutraceuticals. This would also help the government as it would result in lesser expenditure on healthcare and low social security costs.

A rise in disposable income, increasing consumer awareness concerning health issues, and rapid urbanization are likely to boost the market growth over the forecast years. A positive outlook towards medical nutrition owing to the high prevalence of weight management programs, along with cardiovascular diseases, is anticipated to propel the product demand.

The rise and evolution of wellness-focused diets such as keto and paleo are driving food producers to cater their products in this direction. Functional food products such as probiotics and omega-3 are highly used in yogurt and fish oils to reduce the risk of cardiovascular diseases and develop the quality of intestinal microflora, which is further projected to fuel the growth of the functional food segment over the coming years.

Request a free sample copy or view report summary: Nutraceuticals Market Report

Nutraceuticals Market Report Highlights

Based on ingredient, in 2023, probiotics held a dominant position in the market; with a share of 27.7% owing to the majority of food manufacturing companies using probiotics as a primary ingredient to provide better nourishment and reduce health problems caused by harmful bacteria

The vitamins segment captured a significant market share in 2023. The segment is expected to witness significant growth in the coming years

In terms of product, the functional foods segment dominated the market with a revenue share of 37.65% in 2023. Rising healthcare costs, coupled with the increasing geriatric population across the world, are anticipated to assist the segment growth over the forecast period

North America held the largest revenue share of over 34.90% in 2023. The growing health concerns amongst consumers and increasing awareness regarding nutraceuticals are likely to be the major drivers of the North America market.

The market represents a highly competitive landscape. Key market players dominate the market space and have been focusing on various strategic initiatives including mergers & acquisitions, product innovation, and portfolio expansion

Nutraceuticals Market Segmentation

Grand View Research has segmented the global nutraceuticals market based on ingredient, product, application, and region:

Nutraceuticals Ingredient Outlook (Revenue, USD Million, 2018 - 2030)

Aloe vera

Amino acids

Botanical Ingredients

Ashwagandha

Curcumin

Ginseng

Hemp

Others

Cannabidiol (CBD)

Carbohydrates

Carnitine

Food Color

Carotenoids

Astaxanthin

Lutein

Lycopene

Other carotenoids (Zeaxanthin, Betacarotene)

Spirulina

Collagen

Colostrum

Cultures and fermentation starters

Dairy ingredients

Emulsifiers

Enzymes

Essential oils

Fat replacers

Fats and oils

Fibers

Flavors

Fruit and vegetable products

Glucosamine / Chondroitin

Isoflavones

Juices and concentrates

Krill

Lipids / Fatty Acids

Marine ingredients

Minerals

Calcium

Iron

Magnesium

Selenium

Others

Omega-3s

Marine Derived

Plant-derived

Prebiotics

Probiotics

Proteins

Sweeteners

Stevia

Monkfruit

Others (Honey, sucrose, fructose, etc.)

Vitamins

Vitamin A

Vitamin B

Vitamin C

Vitamin D

Vitamin E

Vitamin K

Whey proteins

Other

Nutraceuticals Product Outlook (Revenue, USD Million, 2018 - 2030)

Dietary supplements

Functional foods

Functional beverages

Nutraceuticals Application Outlook (Revenue, USD Million, 2018 - 2030)

Allergy & intolerance

Animal nutrition

Healthy ageing

Bone & joint health

Cancer prevention

Children's health

Cognitive health

Diabetes

Digestive / Gut health

Energy & endurance

Eye health

Heart health

Immune system

Infant health

Inflammation

Maternal health

Men's health

Nutricosmetics

Oral care

Personalized nutrition

Post Pregnancy and reproductive health

Sexual health

Skin health

Sports nutrition

Weight management & satiety

Women's health

Other

Nutraceuticals Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

Germany

France

Italy

UK

Spain

The Netherlands

Asia Pacific

China

Japan

India

Australia & New Zealand

South Korea

Central & South America

Brazil

Argentina

Middle East & Africa

UAE

South Africa

List of Key Players in the Nutraceuticals Market

DSM

Amway

Pfizer Inc.

Nestle

The Kraft Heinz Company

The Hain Celestial Group, Inc.

Nature's Bounty

General Mills Inc.

Danone

Tyson Foods

0 notes

Text

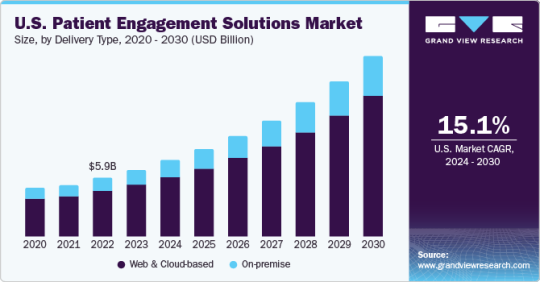

Patient Engagement Solutions Market Is Anticipated To Attain Around $70.3 Billion By 2030

The global patient engagement solutions market size is expected to reach USD 70.3 billion by 2030, expanding at a CAGR of 17.7% from 2024 to 2030, according to a new report by Grand View Research, Inc. Key factors fueling the market growth include rising digitalization across healthcare, increasing prevalence of chronic conditions, and technological advancements. COVID-19 pandemic boosted digitalization across healthcare. This, in turn, has fueled the awareness and adoption of patient engagement solutions, thus propelling the market growth.

As healthcare providers were battling the constant upsurge in cases, patients were looking to digital technologies for care delivery and monitoring. This contributed to the market growth. Key companies released multiple COVID-19-related features as part of their patient engagement lineup to enhance their offerings. In December 2020, athenahealth released new features to its athenaOne platform-such as scheduling, workflow, documentation, and reporting capabilities-to enable immediate administration of COVID-19 vaccines as and when they become available.

The necessity of social distancing resulted in increased demand for remote patient monitoring solutions and prerequisite for the precise and timely exchange of patient well-being records. Pandemic has also made healthcare professionals look for alternate methods to traditional processes and systems. As a result, market participants have developed COVID-19-related features in their existing patient engagement solutions. For instance, in June 2020, Orion Health partnered with a network of more than 350 healthcare facilities called Keystone Health Information Exchange to enable real-time automated COVID-19 reporting for improved public health data collection across Pennsylvania and New Jersey.

As per a survey by Twilio, a cloud communications provider and customer engagement, 68% of respondents reported accelerated digitalization in their organizations due to COVID-19. Companies reported easing of barriers at organizational levels, such as getting executive approvals, the need for a clear strategy, and reluctance to replace legacy software. In fact, according to the Chief Product Officer at Mount Sinai Health System, their newly developed text?to?chat platform witnessed a 10x surge in volume due to the pandemic. Growing number of smartphone users around the globe expedited the adoption of digital health technologies across the sector, both from providers and consumers, which, in turn, has augmented the dependability of patients on mHealth apps.

Mobile technology has emerged as a pivotal driver of healthcare's digital and telemedicine revolution. Smartphones, tablets, and wearable devices have simplified access to healthcare support & patient records, elevated the quality of patient care, and streamlined back-office operations & medical training. Leveraging platforms such as WhatsApp for engagement enabled hospitals to manage patient interactions through an accessible communication channel. Solutions such as Easyrewardz Healthcare CRM empower hospital staff to automate patient communication, appointment scheduling, and room availability checks. These advancements are poised to fuel market growth over the forecast period.

Request a free sample copy or view report summary: Patient Engagement Solutions Market Report

Patient Engagement Solutions Market Report Highlights

Based on delivery type, the web and cloud-based segment emerged as the largest segment in 2023 as it supports hassle-free information flow between patients and healthcare providers. Moreover, bulk data can be stored in these platforms and accessed remotely

Based on component, the software and hardware segment dominated the market with a revenue share of 62.7% in 2023, owing to the continuous development of patient engagement solutions and increasing applications in health and wellness, patient education, and chronic disease management

Based on therapeutic area, the chronic disease management segment dominated the market in 2023. The growth is attributed to the rising in the geriatric population and the increased prevalence of chronic diseases

Based on functionality, the communication segment dominated the market in 2023 as it forms the core of any patient engagement solution. Market players are continuously releasing upgrades and new features to enhance offerings. For instance, in November 2020, Cerner partnered with WELL Health Inc. to boost the communication capabilities of its patient portal- HealtheLife.

Based on end-use, the providers segment dominated the market due to increasing adoption of patient and customer engagement solutions that promote widespread coverage and enable value-based care delivery

North America dominated the global market in 2023 owing to the increased adoption of m-health and electronic health records (EHRs) and growing investments in patient engagement software by major companies

Companies are adopting various strategies to sustain competition. New product/solution development, partnerships, mergers, acquisitions, strategic collaborations, and geographical penetration are some of the key strategies adopted by market players

Patient Engagement Solutions Market Segmentation

Grand View Research has segmented the global patient engagement solutions market based on delivery type, component, functionality, therapeutic area, application, end-use, and region:

Patient Engagement Solutions Delivery Type Outlook (Revenue, USD Million, 2018 - 2030)

Web & Cloud-based

On-premise

Patient Engagement Solutions Component Outlook (Revenue, USD Million, 2018 - 2030)

Software & Hardware

Standalone

Integrated

Services

Consulting

Implementation & Training

Support & Maintenance

Others

Patient Engagement Solutions Functionality Outlook (Revenue, USD Million, 2018 - 2030)

Communication

Health Tracking & Insights

Billing & Payments

Administrative

Patient Education

Others

Patient Engagement Solutions Therapeutic Area Outlook (Revenue, USD Million, 2018 - 2030)

Health & Wellness

Chronic Disease Management

Others

Patient Engagement Solutions Application Outlook (Revenue, USD Million, 2018 - 2030)

Population Health Management

Outpatient Health Management

In-patient Health Management

Others

Patient Engagement Solutions End-use Outlook (Revenue, USD Million, 2018 - 2030)

Payers

Providers

Others

Patient Engagement Solutions Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Europe

Germany

UK

France

Italy

Spain

Sweden

Norway

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

MEA

South Africa

Saudi Arabia

Kuwait

UAE

List of Key Players in the Patient Engagement Solutions Market

Cerner Corporation (Oracle)

NextGen Healthcare, Inc.

Epic Systems Corporation

Allscripts Healthcare, LLC

McKesson Corporation

ResMed

Koninklijke Philips N.V.

Klara Technologies, Inc.

CPSI

Experian Information Solutions, Inc.

athenahealth, Inc.

Solutionreach, Inc.

IBM

MEDHOST

Nuance Communications, Inc.

0 notes

Text

Corporate Wellness Market Expected To Achieve Lucrative Growth By 2030

The global corporate wellness market size is expected to reach USD 74.9 billion by 2030, expanding at a CAGR of 4.47% during the forecast period, based on a new report by Grand View Research, Inc. Rising obese and overweight population increases insurance costs that account for the financial burden on employers. Corporate wellness initiatives target particular health risk factors such as stress, obesity, smoking, poor eating, and lack of exercise.

The pandemic has caused a change in the process of delivering wellness services. Although in-person sessions have resumed to some extent, the virtual platform has been made available to at-risk employees to meet their psychological and fitness needs. Initially, the lockdown imposed due to COVID-19 resulted in a transition to work from home, causing a great deal of stress. Companies around the globe are modifying their corporate wellness strategies to meet the emerging public health crisis due to COVID-19.

Organizations are increasingly using corporate wellness programmes to boost employee health and productivity, mitigate health risks, and minimize employee healthcare expenses. Businesses are more conscious of the importance of maintaining a psychologically and physically healthy workforce. As a result, capital investment in employee wellness programmes, solutions, and services has surged. Absenteeism expenses are reduced by USD 2.7 for every dollar spent on fitness programmes, according to a study conducted by Harvard economists. As a direct consequence, employees must be encouraged to live a healthier lifestyle in order to perform better.

Employers providing the programs have noticed a significant rise in productivity and a decline in leaves and attrition. In addition, companies in the U.K. initiated the Fit for Work service, which offers a tax benefit of USD 663.3 per year. Organizations are providing wearables, such as Fitbit, Apple, and Google watches, which helps in keeping track of parameters such as heart rate and blood pressure.

Moreover, the International Labor Organization (ILO) estimates that the Asia-Pacific employs 1.9 billion people. Globalization has led in significant economic expansion throughout the region, with most countries experiencing a continuous increase in the number of employees. Additionally, the region's workforce is aging, with the region's population aged 60 and over predicted to grow by 24% by 2050, according to the United Nations report. This would result in an increase in the burden of chronic diseases among the region's working population in the following years. These factors create a potential for the market to grow in emerging countries throughout the forecast period.

Request a free sample copy or view report summary: Corporate Wellness Market Report

Corporate Wellness Market Report Highlights

In terms of service, the health risk assessment segment dominated the corporate wellness market in 2022. The health assessment activities enable employers to implement strategic initiatives to deal with the identified health risks

The stress management segment is likely to showcase the fastest growth rate from 2023 to 2030, owing to the rising preference for on-site yoga and meditation services and the rising prevalence of depression and anxiety due to the COVID-19 pandemic.

Based on End-Use, large scale organizations segment dominated the market in 2022. The infrastructure in large scale companies makes conducting fitness services easier and convenient

North America dominated the market in 2022 due to the popularity of corporate wellness in the region. According to a survey by Benefits Canada conducted on 1300 employers, North America had the highest number of corporate wellness programs. More than 80.0% of the employers in North America are offering corporate wellness services to their employees

Corporate Wellness Market Segmentation

Grand View Research has segmented the global corporate wellness market based on service, end-use, category, delivery model, and region:

Corporate Wellness Service Outlook (Revenue, USD Million, 2016 - 2030)

Health Risk Assessment

Fitness

Smoking Cessation

Health Screening

Nutrition & Weight Management

Stress Management

Others

Corporate Wellness End-Use Outlook (Revenue, USD Million, 2016 - 2030)

Small Scale Organizations

Medium Scale Organizations

Large Scale Organizations

Corporate Wellness Category Outlook (Revenue, USD Million, 2016 - 2030)

Fitness & Nutrition Consultants

Psychological Therapists

Organizations/Employers

Corporate Wellness Delivery Model Outlook (Revenue, USD Million, 2016 - 2030)

Onsite

Offsite

Corporate Wellness Regional Outlook (Revenue, USD Million, 2016 - 2030)

North America

U.S.

Canada

Europe

U.K.

Germany

France

Italy

Spain

Russia

Netherlands

Switzerland

Asia Pacific

Japan

China

India

Australia

New Zealand

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East & Africa (MEA)

South Africa

Saudi Arabia

UAE

List of Key Players of the Corporate Wellness Market

ComPsych

Wellness Corporate Solutions

Virgin Pulse

EXOS

Marino Wellness

Privia Health

Vitality

Wellsource, Inc.

Central Corporate Wellness

Truworth Wellness

SOL Wellness

0 notes

Text

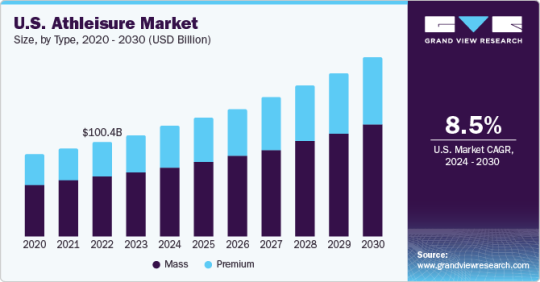

Athleisure Market Is Expected To Witness Higher Demands Till 2030

The global athleisure market size is expected to reach USD 662.56 billion by 2030, expanding at a CAGR of 9.3% from 2024 to 2030, according to a new report by Grand View Research, Inc. Athleisure is a popular category as it taps into several broad trends, including a global shift toward consumers wearing more casual clothing & seeking comfortable clothing. The rising popularity of athletic activities that require performance clothing will support market growth. True Fit’s Fashion Genome (via Direct Commerce), which analyses data from 17,000 brands and 180 million True Fit users, confirms that athleisure orders have increased by 84% since the pandemic began; sales of women’s athleisure bottoms in the United Kingdom alone were five times higher in December 2020 than in April 2020. In addition, order volumes for men's athleisure wear sales increased by 20% from the previous year.

Target’s activewear line, All in Motion, which had only been launched before the pandemic, reportedly surpassed $1 billion in sales. Despite this bleak outlook for fresh commercial opportunities, independent gear manufacturers continue to emerge. The majority of these new firms are a result of their creators’ desire for a fresh running-apparel aesthetic or their ongoing hunt for high-quality athletic apparel. According to GQ, at least a dozen new businesses have joined the market with identical origin stories in the previous five years. The British companies Ashmei and Iffley Road; the Danish brand Doxarun; and the American brands Isaora and Tracksmith, are some examples. The demand for highly comfortable clothes with sports features while undertaking any activity has increased in recent years, and wide pockets and elastic knot elements have become important products for carrying large mobile phones, purses, and a few other daily essentials. The growing utility fashion trend has spurred the demand for utility-active apparel.

Request a free sample copy or view report summary: Athleisure Market Report

Athleisure Market Report Highlights

The mass athleisure segment dominated the overall market in 2023 and is projected to grow substantially over the forecast period

The rising popularity and benefits of yoga as a mind-body fitness activity is leading to an increased number of yoga enthusiasts across the world

North America had the largest revenue share in 2023 while Asia Pacific is anticipated to register the fastest CAGR from 2024 to 2030

The global industry is highly competitive owing to the presence of a large number of international and regional players that strive to innovate persistently

Athleisure Market Segmentation

Grand View Research has segmented the global athleisure market on the basis of type, product, end-user, distribution channel, and region:

Athleisure Type Outlook (Revenue, USD Billion, 2018 - 2030)

Mass

Premium

Athleisure Product Outlook (Revenue, USD Billion, 2018 - 2030)

Yoga Apparels

Tops

Pants

Shorts

Unitards

Capris

Others

Shirts

Leggings

Shorts

Others

Athleisure End-user Outlook (Revenue, USD Billion, 2018 - 2030)

Men

Women

Children

Athleisure Distribution Channel Outlook (Revenue, USD Billion, 2018 - 2030)

Online

Offline

Athleisure Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

Germany

U.K.

France

Italy

Spain

Asia Pacific

China

Japan

India

Australia & New Zealand

Singapore

Central & South America

Brazil

Middle East & Africa

South Africa

UAE

List of Key Players of Athleisure Market

Hanes Brands, Inc.

Adidas AG

Vuori

PANGAIA

Under Armour, Inc.

Outerknown

EILEEN FISHER

Patagonia, Inc.

Wear Pact, LLC

Lululemon Athletica

0 notes

Text

Physical Security Market Likely To Reach Beyond $216.43 Billion By 2030

The global physical security market size is expected to reach USD 216.43 billion by 2030, registering CAGR of 6.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. Lack of physical security leads to higher rates of burglaries and thefts. Therefore, safeguarding the physical perimeter and individual assets, including expensive technological equipment, has gained importance and is driving the market growth.

Increasing awareness about securing the perimeter in developing economies has led to a rise in deployment of IP-based cameras in residential societies as well as commercial complexes and offices. Furthermore, increasing terror threats, border disputes, and refugee crises drive the adoption of stringent safety measures, thereby driving the market growth.

For instance, in February 2022, Hangzhou Hikvision Digital Technology Co., Ltd, the world's prominent manufacturer of innovative video surveillance systems and solutions, introduced the TandemVu PTZ camera line, which combines PTZ and bullet camera capabilities into a single unit. These cameras can monitor broad regions and zoom in on individual security incidents while simultaneously maintaining attention on both viewpoints. Further, this camera would be deployed in commercial complexes and residential societies to reduce terror threats and adopt more physical security on the premises.

The increasing convergence of IT and OT technologies have potentially increased concern towards inbuilt security operations that are added into a network. As network video recorders (NVRs) and IP-based surveillance camera are network devices, they are vulnerable to become a target vector to get into a system. Furthermore, camera & biometrics offer robust physical security benefits. However, in a growing threat ecosystem, these devices are expected to evolve in order to enable safety for deployment in a critical infrastructure asset’s network.

Thus, securing the converged IT & OT network is emerging as one of the top priorities for several companies. For instance, in November 2021, InsightCyber Group, Inc., a company that offers physical, cyber systems to protect businesses, built an AI-driven physical security device for various industries such as transportation, manufacturing supply chain, and others. The physical security device has a wide range of OT machines and IT hardware technologies which would provide safety and protection to all customers, employees, and assets of the company with more security.

The technological advancement in physical security systems such as video analytics and machine learning are expected to drive the overall market. Moreover, the hardware is also gaining high traction which attributes to significant enhancement to the legacy surveillance camera system. For instance, in April 2022, Matrix Comsec., a prominent security solutions provider, launched a new 8MP dome IP camera. Large organizations and project environments will benefit from Matrix Project Series Dome Cameras. The cameras are suitable for outdoor and indoor monitoring needs, making them ideal for the modern businesses.

Further, the cameras have been designed with technology that improves image quality and provides robust physical security around the surroundings. Besides, in March 2022, Axis Communications AB., a Sweden-based company that offers services to private sectors and governments, launched a lightweight bullet camera- AXIS M2036-LE which offers quad HD 1440p and around 129° horizontal view, which supports machine learning and deep learning. These offerings have enticed customers and enterprises to witness the advantages of multiple connected cameras for security operations, thereby fuelling the market growth.

Leveraging IoT technology to enhance physical security is anticipated to be a potential factor driving the market growth. The IoT offers several ways to improve physical security and access control system. The connected sensors and devices, and automated alert system enhance the effectiveness of the security products and provide robust abilities such as intelligence monitoring, tampering alert, perimeter protection, and automobile tracking among others.

Thus, technological development and its exponential growth are anticipated to positively impact the market dynamics of the physical security market during the forecast period. For instance, in October 2022, Viakoo Inc., an American cybersecurity company, launched Action Platform, an automated IoT device management platform for managing, securing, and updating firmware, ensuring device password compliance, and providing IoT device certificates. The platform enables organizations to identify and resolve security flaws on connected systems and secure these devices' safety and security. Such innovative solutions and their deployment in the region are propelling the growth of the physical security market forward.

Request a free sample copy or view report summary: Physical Security Market Report

Physical Security Market Report Highlights

Video surveillance system led the market in 2022, as these systems enable real-time continuous monitoring and help lower chances of theft

System integration is anticipated to dominate the market through the forecast period owing to the factors such as stringent regulations and demand for the cost-effective systems

The residential segment is predicted to register the highest CAGR during the forecast period owing to the measures taken by the consumers to protect their assets from potential threats

North America dominated the market in 2022 and is estimated to remain dominant throughout the forecast period. The presence of key physical security market vendors such as Cisco Systems, Inc., Honeywell International, Inc., and Pelco is primarily responsible for the region's market growth. Businesses across the region are increasingly deploying physical security solutions to prevent identity theft, cyber-attacks, and commercial spying, as well as to ensure data security and privacy to facilitate business continuity

Physical Security Market Segmentation

Grand View Research has segmented the global physical security market report based on the component, organization size, end-user, and region:

Physical Security Component Outlook (Revenue, USD Billion, 2017 - 2030)

Systems

Physical Access Control System (PACS)

Video Surveillance System

Perimeter Intrusion Detection And Prevention

Physical Security Information Management (PSIM)

Physical Identity & Access Management (PIAM)

Fire And Life Safety

Services

System Integration

Remote Monitoring

Others

Physical Security Organization Size Outlook (Revenue, USD Billion, 2017 - 2030)

SMEs

Large Enterprises

Physical Security End-user Outlook (Revenue, USD Billion, 2017 - 2030)

Transportation

Government

Banking & Finance

Utility & Energy

Residential

Industrial

Retail

Commercial

Hospitality

Others

Physical Security Regional Outlook (Revenue, USD Billion 2017 - 2030)

North America

U.S.

Canada

Mexico

Europe

U.K.

Germany

France

Asia Pacific

China

India

Japan

South America

Brazil

Middle East & Africa

List of The Key Players in the Physical Security Market

Hangzhou Hikvision Digital Technology Co., Ltd.

Honeywell International, Inc.

Genetec Inc.

Cisco Systems Inc.

Axis Communications AB

Pelco

Robert Bosch GmbH

Johnson Controls

ADT LLC

Siemens

0 notes

Text

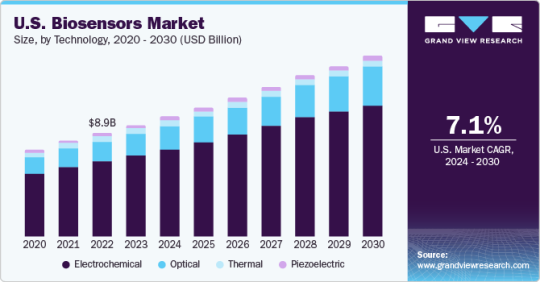

Biosensors Market Is Expected To Grow Swiftly By 2030

The global biosensors market size was estimated at USD 28.9 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 8.0% from 2024 to 2030. The key factors driving the industry growth include various applications in the healthcare/medical sector, increasing demand in the bioprocessing industry, and rapid technological advancements in drug screening due to the COVID-19 pandemic. Moreover, the pandemic led to the rapid expansion of the biosensor industry due to an increase in the number of hospitals worldwide.

Over the forecast period, technological advancements are expected to be significant growth drivers for the industry. For example, in January 2022, a U.S. medical device manufacturer, Abbott, launched a universal consumer wearable device with biosensors. The company announced the development of a new line of consumer biometric wearable devices called Lingo, designed for more general fitness and wellness purposes. In addition, increasing demand for biosensors and bioreactors for new drug development is likely to lead to industry expansion in the near future due to improved biosensor technology.

Request a free sample copy or view report summary: Biosensors Market Report

Biosensors Market Report Highlights

The electrochemical biosensors technology segment accounted for the largest revenue share in 2023

The segment is anticipated to witness significant growth over the forecast period owing to the widespread applications for analysis & quantification in biochemical and biological processes

Based on the application, the medical segment dominated the industry in 2023. This device is considered an essential tool in the monitoring and detection of a wide range of medical conditions, such as cancer and diabetes

Middle East & Africa is expected to witness the fastest growth rate over the forecast period

This is owing to a rise in research & development activities and constantly improving healthcare facilities in the region.

Biosensors Market Segmentation

Grand View Research has segmented the biosensors market report on the basis of technology, application, end-user, and region:

Biosensors Technology Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Thermal

Electrochemical

Piezoelectric

Optical

Biosensors Application Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Medical

Cholesterol

Blood Glucose

Blood Gas Analyzer

Pregnancy Testing

Drug Discovery

Infectious Disease

Food Toxicity

Bioreactor

Agriculture

Environment

Others

Biosensors End-user Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Home Healthcare Diagnostics

POC Testing

Food Industry

Research Laboratories

Security and Bio-Defense

Biosensors Regional Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Europe

UK

Germany

France

Italy

Spain

Belgium

Switzerland

The Netherlands

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Indonesia

Thailand

Latin America

Brazil

Mexico

Argentina

Colombia

Middle East and Africa (MEA)

South Africa

Saudi Arabia

UAE

Turkey

Kuwait

List of Key Players of Biosensors Market

Bio-Rad Laboratories Inc.

Medtronic

Abbott Laboratories

Biosensors International Group, Ltd.

Pinnacle Technologies Inc.

Ercon, Inc.

DuPont Biosensor Materials

Johnson & Johnson

Koninklijke Philips N.V.

LifeScan, Inc.

QTL Biodetection LLC

Molecular Devices Corp.

Nova Biomedical

Molex LLC

TDK Corp.

Zimmer & Peacock AS

0 notes

Text

Automotive Lighting Market Is Anticipated To Attain Around $34.65 Billion By 2030

The automotive lighting market is anticipated to reach USD 34.65 billion by 2022. Strict government policies and rising safety concerns are likely to propel growth over the forecast period. In addition, growing consumer awareness concerning the significance of adaptive lighting including dynamic bend light and a glare-free high beam is also expected to have a positive impact on the exterior lighting market.

Increasing apprehensions about using energy-efficient methods coupled with rising consumer disposable income are expected to drive the industry. In addition, growing demand for vehicles and technological advancements in the automotive industry is expected to propel utilization. Attractive growth opportunities for new entrants are expected in the industry owing to the growing number of total vehicles purchased y-o-y across BRIC nations. However, there is a need for legislative authorities to collaborate with light sourcing technology suppliers to develop flexible design techniques.

THE Automotive LED market is estimated to demonstrate considerable growth at a CAGR of over 12.0% from 2015 to 2022. Halogen lights contributed to over 66.0% of overall industry revenue in 2014, followed by LED and xenon. It has gained prominence on account of easy availability, low purchasing costs, and low replacement costs. However, rising fuel prices are expected to pose a threat to the industry.

Asia Pacific automotive lighting market, by technology, 2012 - 2022 (USD Million)

To request a sample copy or view summary of this report, click the link below:

http://www.grandviewresearch.com/industry-analysis/automotive-lighting-market

The increase in demand for eco-friendly LED technologies on account of high efficiency, reduced CO2 levels, and high power, is expected to propel growth. Companies have been trying to develop eco-friendly LEDs to promote product differentiation and strengthen their global foothold. LEDs are used in daytime running lights (DRL), parking light, brake lights, and turning lights. LEDs are preferred over xenon and halogen lights owing to optimum light-bearing capacities and improved design, which lead to increased shelf life.

The adaptive headlight is an active safety feature that is intended to enhance the drivers’ visibility in poorly illuminated areas. It encompasses functionalities including automatic rotation which can sync with sensors and adjust brightness and intensity of light. The front lighting segment accounted for over 70.0% of the total revenue in 2014 owing to the availability of advanced features including automatic rotation which can sync with automatic brightness modules and sensor response. Extreme climatic conditions in Europe and North America are expected to trigger demand for fog lights over the forecast period.

The automotive lighting industry in Asia Pacific is estimated to grow at a CAGR of over 8.0% and acquire a market share of about 45.0% over the forecast period. The continuous expansion of suppliers coupled with a vast production base is expected to position this region as the market leader. Countries including India, Japan, and China account for the major production base for vehicles globally, thus offering extensive growth opportunities.

Key companies including Hella KGaA Hueck & Co., Koito Manufacturing Co., Magneti Marelli S.p.A and Valeo. Vendors usually employ the strategy of new product development and mergers & acquisitions to enter new markets. The introduction of low-cost LEDs and energy-efficient alternatives is foreseen as a cost-effective strategy for the industry.

Grand View Research has segmented the automotive lighting market on the basis of technology, application, and region:

Automotive Lighting Technology Outlook (Revenue, USD Million, 2012 - 2022)

Halogen

Xenon

LED

Automotive Lighting Application Outlook (Revenue, USD Million, 2012 - 2022)

Front/headlamps

Rear

Side

Interior

Automotive Lighting Regional Outlook (Revenue, USD Million, 2012 - 2022)

North America

Europe

Asia Pacific

RoW

0 notes