#Is Optimism (OP) worth $1.31?

Text

Is Optimism (OP) worth $1.31?

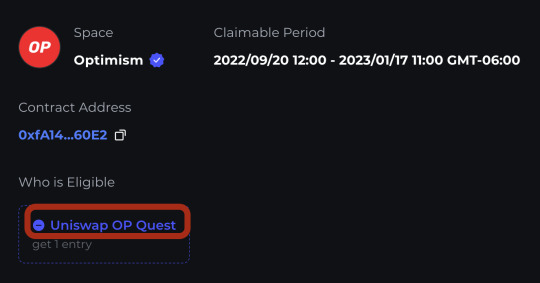

Interest in Optimism (OP) is high. For example, both CoinGecko and CoinMarketCap gave OP a $1.31 on 21 September 2023.

Optimism was CoinMarketCap’s 13th most trending cryptocurrency on 20 September 2023. Conversely, Optimism was CoinGecko’s seventh most trending cryptocurrency on the same day.

Moreover, CoinGecko named Optimism the 42ndlargest cryptocurrency, while CoinMarketCap labeled OP the…

View On WordPress

#How Optimism connects with Ethereum (ETH)#How Optimism Works#How they decentralize Optimism#How to Add Value to Optimism#Is Optimism (OP) worth $1.31?#Next Gen Fault Proofs#Optimism (OP)#The Optimism Ecosystem#What is Optimism?#What is the Optimism Superchain?#What Value does Optimism Offer?

0 notes

Text

Zach Eflin Looks to Put Final Touches on a Brilliant June

The Phillies will turn to Zach Eflin tonight in an attempt to salvage the final game of what has been a humbling series against the New York Yankees. They will hope that Eflin, who has spent much of June surprisingly playing the role of stopper, can add one more big-time start to what has been the 24-year-old right-hander’s finest month as a Major League pitcher.

His June began with a much needed 7.2 innings of one-run baseball against the Cubs that helped the Phillies wash away the bitter taste of a disastrous three-game sweep in San Francisco. He followed that key outing with a six-inning performance against the Brewers in which he allowed only two earned runs while striking out nine to help snap a four-game losing streak. His third start produced five innings of one-run baseball which helped the Phillies bounce back from a hideous 13-2 loss in the opening game at Milwaukee. Most recently, his latest start helped set the tone in the opener of an important series win in Washington.

Eflin’s June performance has been crucial to the Phillies’ ability to survive what has been a relentlessly difficult stretch of games against elite opponents, particularly given Jake Arrieta’s underwhelming 0-4 record and 6.66 ERA this month.

Just how good has Eflin been? He’s 4-0 in four starts, and his 2.28 ERA, 2.00 FIP, and 1.014 WHIP lead all Phillies starters this month.

Want more? I’ve got more. Have some.

He’s held opponents to a .227 batting average, .280 on-base percentage, .262 wOBA, and .594 OPS, all of which are best among Phils starters this month. Several of those numbers are among baseball’s best in June. Eflin’s June FIP ranks fifth among all starting pitchers that have logged at least 20 innings since the start of the month.

So what exactly has happened that has made him so much better than his mediocre month of May in which he posted a 4.50 ERA and 1.31 WHIP? Well, a few things. According to FanGraphs, his hard contact rate dropped from a 34.2% in May to 21.2% this month and his groundball rate has climbed from 28.8% to 43.1%. That’s typically going to yield favorable results for a guy who is known as a groundball pitcher. But there’s another factor at play here, which is perhaps the biggest reason for optimism regarding the sustainability of his improved performance. He is missing more bats.

Check out this chart which shows a dramatic linear improvement in his swinging strike percentage since his 2016 rookie season:

This graph demonstrates a direct correlation between his significantly declining ERA and FIP and his improving K/9 rate:

In fact, Eflin’s 9.24 K/9 this season is almost twice as high as his previous career best of 4.9 K/9 a year ago. The most obvious explanation for this radical improvement is that he’s finally healthy after battling shoulder, elbow, and knee injuries over the past few seasons. In terms of velocity, his average four-seam fastball sits at 95.1 mph, up from 93.7 mph last season. He’s throwing it almost twice as much as he did a season ago, and he’s relying on his sinker less.

It’s a rush to judgment to suggest that Eflin is in the process of turning himself into a legitimate middle of the rotation arm, but it’s not a preposterous idea at this point. Maybe he goes out tonight and gets pounded into submission by a daunting Yankees lineup and we cool the jets, but his progress is worth noting and keeping an eye on moving forward, particularly as the July 31 deadline nears. The Phillies could consider adding a veteran arm or a left-handed starter to help balance out their rotation. A few weeks ago, it seemed clear that Eflin would be the odd man out in that scenario. Now? Matt Klentak has something to think about.

The post Zach Eflin Looks to Put Final Touches on a Brilliant June appeared first on Crossing Broad.

Zach Eflin Looks to Put Final Touches on a Brilliant June published first on https://footballhighlightseurope.tumblr.com/

0 notes

Text

Inflation and Retail Sales Disappoint – Market Update

As a sports fan in Detroit, it was kind of a scary weekend. Michigan and Michigan State both made their games way closer than they needed to be, and the Lions definitely didn’t have their best performance. However, things are getting spooky around the NFL as well. I’d hate to be a Packers fan with the injury to quarterback Aaron Rodgers yesterday.

Some of the market data to come out last week showed scary weakness, but it wasn’t enough to give the stock market the creeps. Let’s open that creaking door and dive into the house of (sometimes) bizarre economic data.

Headline News

Quicken Loans Home Price Perception Index (HPPI)

Home appraisals are coming closer to homeowner estimates recently, and that trend continued in September, with the difference between these and appraiser opinions being just 1.14%. This was an improvement of 0.21% from last month.

In terms of regional data, homeowners in the West overestimated by just 0.93%. Homeowners in the South and Northeast overvalued their properties by just 1.14% and 1.21%, respectively. Estimates of Midwestern homeowners were off by 1.31%.

Dallas has the nation’s most undervalued housing market, with appraiser opinions coming in 2.87% higher than homeowner estimates. Philadelphia homeowners were at the other end of the spectrum, with estimates being 2.89% higher than actual appraisal values. Homeowners and appraisers were closest to agreement in Riverside, California. Residents underestimated value by just 0.03%.

Quicken Loans Home Value Index (HVI)

Home values were up 0.44% in September and have risen 3.38% since the same time last year. However, the data is a little uneven.

Values were down 1.33% in the South, but they’ve still risen 2.08% on the year. It’s possible the monthly drop has something to do with hurricane season. We’ll have to keep an eye on this. The South is the nation’s largest housing region in terms of new construction.

In the West, values were up 0.98%, rising 5.77% yearly. Northeastern homeowners saw values rise 0.91% for a 2.71% annual increase. The Midwest saw values rise 0.66%, up 5.64% on the year.

MBA Mortgage Applications

Mortgage applications fell 2.1% overall. Purchase applications were down 0.1%, but rates had a bigger impact on applications to refinance, which fell 4.0%. The average rate on a 30-year fixed conforming mortgage was up four basis points to 4.16%.

Jobless Claims

After being higher for several weeks in the aftermath of several hurricanes, initial jobless claims appear to be coming back to normal levels. They were down 15,000 last week to 243,000. With that said, claims in Puerto Rico are still very low, and analysts are assuming this is because displaced workers are having trouble filing claims due to power outages. Numbers in Virginia and South Carolina were also estimated.

Meanwhile, the four-week average of continuing claims was down 9,500 to come in at 257,500.

On the continuing claims side, these were down 32,000 to 1.889 million. The four-week average of continuing claims was down 12,000 to 1.925 million.

Producer Price Index (PPI)

The hurricanes caused increases in energy prices in September. Along with an uptick in services inflation, they were key in having prices increase 0.4% for producers in September, in line with analysts’ expectations. Production prices are up 2.6% on the year. However, when food and energy prices were taken out, prices rose 0.4% as well and are up 2.2%. When further removing trade services, production prices were up 0.2% and 2.1% annually.

Taking a deeper look at the numbers, energy prices were up 3.4% following Harvey and Irma. Food prices are unchanged. Trade services also increased 0.8%.

Consumer Price Index (CPI)

Consumer prices are where the Federal Reserve needs to decide whether they’re haunted enough to be put off another hike in short-term interest rates before the end of the year. That’s because inflation came in weaker than expected on the consumer side of the coin, up just 0.5% and 2.2% on the year in September. Consensus expectations had been for a 0.6% increase. When food and energy were taken out, prices were up 0.1% and 1.7% on the year, a little below targets.

While that may not sound like a big miss, with a 6.1% rise in energy prices related to hurricane season, analysts expected dire numbers. It shows that inflation is soft in other areas of the economy. Housing costs were up only 0.2%, and the cost of medical care was actually down 0.1%. The cost of prescriptions in particular was down 0.6%. Apparel prices were also down 0.1%.

Food prices were up 0.1%. Those that follow the wireless cell phone industry might feel like they’ve entered the Twilight Zone. After falling steadily for most of the year, prices were actually up 0.4%.

Retail Sales

Retail sales did bounce back from a 0.2% dip last month. They’re up 1.6% overall in September and have risen 1.0% when auto sales are taken out. When cars and gas were both removed, they’re up 0.5%. It’s worth noting that expectations had been for a 1.8% overall increase.

Restaurant sales were up 0.8% to come back strong. The hurricanes may have been the cause of an increase in grocery store sales, which rose 1%. Building materials were also up 2.1%. Finally, gasoline sales rose 5.8%.

Consumer Sentiment

Consumer sentiment spiked six points to 101.1 in preliminary October readings. It’s the highest reading in 13 years. The economy is at or near full employment, and there are indications that wages are moving up.

The expectations component is up almost 7 points to 91.3. Part of this optimism is low inflation expectations. Over the next year, consumers expect inflation to rise just 2.3%, and over the next five years, expectations fell to 2.4%. This is a bit of a problem for the Federal Reserve because without the expectation of inflation rising, consumers have less motivation to buy things now and spur the economy. The current conditions index was up nearly five points to 116.4.

Mortgage Rates

Fixed mortgage rates were up quite a bit for the second straight week. If you’re in the market, though, there’s still very low. It’s a great time to lock your rate.

The average rate on a 30-year fixed-rate mortgage was up six basis points to 3.91% for 0.5 points in fees. Last year at this time, the rate was 3.47%.

In shorter terms, the average rate on a 15-year fixed mortgage was up six basis points to 3.21% for 0.5 points. This is up from 2.76% a year ago.

Finally, the average rate on a 5-year treasury-indexed hybrid adjustable rate mortgage (ARM) fell two basis points to 3.16% for 0.4 points. This is up from 2.82% at this time last year.

Stock Market

Investors spent Friday betting that companies would have another strong earnings season in line with recent friends. This meant the Nasdaq hit record highs again Friday.

The Dow Jones industrial average was up 30.71 points on the day to close at 22,871.72. This was up 0.43% on the week. The S&P 500 was up 0.15% on the week to close at 2,553.17. It was up 2.24 points on the day. Finally, the Nasdaq closed at 6,605.80 after being up 14.29 points on the day and 0.24% on the week.

The Week Ahead

Tuesday, October 17

Industrial Production (9:15 a.m. ET) – The Federal Reserve’s monthly index of industrial production – and the related capacity indexes and capacity utilization rates – covers manufacturing, mining, and electric and gas utilities.

Housing Market Index (10:00 a.m. ET) – The National Association of Home Builders produces a housing market index based on a survey where respondents from the organization are asked to rate the general economy and housing market conditions. The index is a weighted average of separate diffusion indexes, including present sales of new homes, sales of new homes expected in the next six months and traffic of prospective buyers in new homes.

Wednesday, October 18

MBA Mortgage Applications (7:00 a.m. ET) – The mortgage applications index measures applications to mortgage lenders. This is a leading indicator for single-family home sales and housing construction.

Housing Starts (8:30 a.m. ET) – A housing start is registered when the construction of a new residential building begins. The start of construction is defined as the beginning of excavation of the foundation for the building.

Thursday, October 19

Jobless Claims (8:30 a.m. ET) – New unemployment claims are compiled weekly to report the number of individuals filing for unemployment insurance for the first time. An increasing trend suggests a deteriorating labor market. The four-week moving average of new claims smooths out weekly volatility.

Friday, October 20

Existing Home Sales (10:00 a.m. ET) – Existing Home Sales tallies the number of previously constructed homes, condominiums and co-ops in which a sale closed during the month. Existing homes (also known as home resales) account for a larger share of the market than new homes and indicate housing market trends.

There’s not much in the way of larger economic data outside of industrial production next week, but we do get lots of housing data. Meanwhile, plenty of companies do have earnings reports next week. We’ll have it covered in Market Update.

We know stocks and economic data aren’t always the most exciting things. If you subscribe to the Zing Blog below, we have plenty of home, money and life content to share with you. It’s time to really start thinking about those Halloween costumes. Here’s our list of 25 trending costumes for 2017. What’s your costume this year? Let us know in the comments. Have a great week!

The post Inflation and Retail Sales Disappoint – Market Update appeared first on ZING Blog by Quicken Loans.

from Updates About Loans https://www.quickenloans.com/blog/inflation-retail-sales-disappoint-market-update

0 notes

Text

Inflation and Retail Sales Disappoint – Market Update

As a sports fan in Detroit, it was kind of a scary weekend. Michigan and Michigan State both made their games way closer than they needed to be, and the Lions definitely didn’t have their best performance. However, things are getting spooky around the NFL as well. I’d hate to be a Packers fan with the injury to quarterback Aaron Rodgers yesterday.

Some of the market data to come out last week showed scary weakness, but it wasn’t enough to give the stock market the creeps. Let’s open that creaking door and dive into the house of (sometimes) bizarre economic data.

Headline News

Quicken Loans Home Price Perception Index (HPPI)

Home appraisals are coming closer to homeowner estimates recently, and that trend continued in September, with the difference between these and appraiser opinions being just 1.14%. This was an improvement of 0.21% from last month.

In terms of regional data, homeowners in the West overestimated by just 0.93%. Homeowners in the South and Northeast overvalued their properties by just 1.14% and 1.21%, respectively. Estimates of Midwestern homeowners were off by 1.31%.

Dallas has the nation’s most undervalued housing market, with appraiser opinions coming in 2.87% higher than homeowner estimates. Philadelphia homeowners were at the other end of the spectrum, with estimates being 2.89% higher than actual appraisal values. Homeowners and appraisers were closest to agreement in Riverside, California. Residents underestimated value by just 0.03%.

Quicken Loans Home Value Index (HVI)

Home values were up 0.44% in September and have risen 3.38% since the same time last year. However, the data is a little uneven.

Values were down 1.33% in the South, but they’ve still risen 2.08% on the year. It’s possible the monthly drop has something to do with hurricane season. We’ll have to keep an eye on this. The South is the nation’s largest housing region in terms of new construction.

In the West, values were up 0.98%, rising 5.77% yearly. Northeastern homeowners saw values rise 0.91% for a 2.71% annual increase. The Midwest saw values rise 0.66%, up 5.64% on the year.

MBA Mortgage Applications

Mortgage applications fell 2.1% overall. Purchase applications were down 0.1%, but rates had a bigger impact on applications to refinance, which fell 4.0%. The average rate on a 30-year fixed conforming mortgage was up four basis points to 4.16%.

Jobless Claims

After being higher for several weeks in the aftermath of several hurricanes, initial jobless claims appear to be coming back to normal levels. They were down 15,000 last week to 243,000. With that said, claims in Puerto Rico are still very low, and analysts are assuming this is because displaced workers are having trouble filing claims due to power outages. Numbers in Virginia and South Carolina were also estimated.

Meanwhile, the four-week average of continuing claims was down 9,500 to come in at 257,500.

On the continuing claims side, these were down 32,000 to 1.889 million. The four-week average of continuing claims was down 12,000 to 1.925 million.

Producer Price Index (PPI)

The hurricanes caused increases in energy prices in September. Along with an uptick in services inflation, they were key in having prices increase 0.4% for producers in September, in line with analysts’ expectations. Production prices are up 2.6% on the year. However, when food and energy prices were taken out, prices rose 0.4% as well and are up 2.2%. When further removing trade services, production prices were up 0.2% and 2.1% annually.

Taking a deeper look at the numbers, energy prices were up 3.4% following Harvey and Irma. Food prices are unchanged. Trade services also increased 0.8%.

Consumer Price Index (CPI)

Consumer prices are where the Federal Reserve needs to decide whether they’re haunted enough to be put off another hike in short-term interest rates before the end of the year. That’s because inflation came in weaker than expected on the consumer side of the coin, up just 0.5% and 2.2% on the year in September. Consensus expectations had been for a 0.6% increase. When food and energy were taken out, prices were up 0.1% and 1.7% on the year, a little below targets.

While that may not sound like a big miss, with a 6.1% rise in energy prices related to hurricane season, analysts expected dire numbers. It shows that inflation is soft in other areas of the economy. Housing costs were up only 0.2%, and the cost of medical care was actually down 0.1%. The cost of prescriptions in particular was down 0.6%. Apparel prices were also down 0.1%.

Food prices were up 0.1%. Those that follow the wireless cell phone industry might feel like they’ve entered the Twilight Zone. After falling steadily for most of the year, prices were actually up 0.4%.

Retail Sales

Retail sales did bounce back from a 0.2% dip last month. They’re up 1.6% overall in September and have risen 1.0% when auto sales are taken out. When cars and gas were both removed, they’re up 0.5%. It’s worth noting that expectations had been for a 1.8% overall increase.

Restaurant sales were up 0.8% to come back strong. The hurricanes may have been the cause of an increase in grocery store sales, which rose 1%. Building materials were also up 2.1%. Finally, gasoline sales rose 5.8%.

Consumer Sentiment

Consumer sentiment spiked six points to 101.1 in preliminary October readings. It’s the highest reading in 13 years. The economy is at or near full employment, and there are indications that wages are moving up.

The expectations component is up almost 7 points to 91.3. Part of this optimism is low inflation expectations. Over the next year, consumers expect inflation to rise just 2.3%, and over the next five years, expectations fell to 2.4%. This is a bit of a problem for the Federal Reserve because without the expectation of inflation rising, consumers have less motivation to buy things now and spur the economy. The current conditions index was up nearly five points to 116.4.

Mortgage Rates

Fixed mortgage rates were up quite a bit for the second straight week. If you’re in the market, though, there’s still very low. It’s a great time to lock your rate.

The average rate on a 30-year fixed-rate mortgage was up six basis points to 3.91% for 0.5 points in fees. Last year at this time, the rate was 3.47%.

In shorter terms, the average rate on a 15-year fixed mortgage was up six basis points to 3.21% for 0.5 points. This is up from 2.76% a year ago.

Finally, the average rate on a 5-year treasury-indexed hybrid adjustable rate mortgage (ARM) fell two basis points to 3.16% for 0.4 points. This is up from 2.82% at this time last year.

Stock Market

Investors spent Friday betting that companies would have another strong earnings season in line with recent friends. This meant the Nasdaq hit record highs again Friday.

The Dow Jones industrial average was up 30.71 points on the day to close at 22,871.72. This was up 0.43% on the week. The S&P 500 was up 0.15% on the week to close at 2,553.17. It was up 2.24 points on the day. Finally, the Nasdaq closed at 6,605.80 after being up 14.29 points on the day and 0.24% on the week.

The Week Ahead

Tuesday, October 17

Industrial Production (9:15 a.m. ET) – The Federal Reserve’s monthly index of industrial production – and the related capacity indexes and capacity utilization rates – covers manufacturing, mining, and electric and gas utilities.

Housing Market Index (10:00 a.m. ET) – The National Association of Home Builders produces a housing market index based on a survey where respondents from the organization are asked to rate the general economy and housing market conditions. The index is a weighted average of separate diffusion indexes, including present sales of new homes, sales of new homes expected in the next six months and traffic of prospective buyers in new homes.

Wednesday, October 18

MBA Mortgage Applications (7:00 a.m. ET) – The mortgage applications index measures applications to mortgage lenders. This is a leading indicator for single-family home sales and housing construction.

Housing Starts (8:30 a.m. ET) – A housing start is registered when the construction of a new residential building begins. The start of construction is defined as the beginning of excavation of the foundation for the building.

Thursday, October 19

Jobless Claims (8:30 a.m. ET) – New unemployment claims are compiled weekly to report the number of individuals filing for unemployment insurance for the first time. An increasing trend suggests a deteriorating labor market. The four-week moving average of new claims smooths out weekly volatility.

Friday, October 20

Existing Home Sales (10:00 a.m. ET) – Existing Home Sales tallies the number of previously constructed homes, condominiums and co-ops in which a sale closed during the month. Existing homes (also known as home resales) account for a larger share of the market than new homes and indicate housing market trends.

There’s not much in the way of larger economic data outside of industrial production next week, but we do get lots of housing data. Meanwhile, plenty of companies do have earnings reports next week. We’ll have it covered in Market Update.

We know stocks and economic data aren’t always the most exciting things. If you subscribe to the Zing Blog below, we have plenty of home, money and life content to share with you. It’s time to really start thinking about those Halloween costumes. Here’s our list of 25 trending costumes for 2017. What’s your costume this year? Let us know in the comments. Have a great week!

The post Inflation and Retail Sales Disappoint – Market Update appeared first on ZING Blog by Quicken Loans.

from Updates About Loans https://www.quickenloans.com/blog/inflation-retail-sales-disappoint-market-update

0 notes

Last Seen Blogs

wullver

Title

theshadowsbringthegleelight

Helem Montanator

kukolkanati

Nati Doll

kittenchloe

crybaby

123malay

Untitled