abri-chan

All Hail the King of Dunces!

ao3: abri_chan. ideator & host: @meravigliazine.

14760 posts

Last active 60 minutes ago

Don't wanna be here? Send us removal request.

Last Seen Blogs

postroika52

ПостройКа52 каркасные дома под ключ

trafalgar-prod-studio-blog

TRAFALGAR PROD. STUDIO

itsmieille

m i e i l l e

shorin011

Untitled

the-general-ask-blogge

The General Ask Blogge

Text

how to find literally any post on a blog in seconds (on desktop)

there are so many posts about ~tumblr is so broken, you can’t find any post on your own blog, it’s impossible, bluhrblub~

I am here to tell you otherwise! it is in fact INCREDIBLY easy to find a post on a blog if you’re on desktop/browser and you know what you’re doing:

url.tumblr.com/tagged/croissant will bring up EVERY post on the blog tagged with the specific and exact phrase #croissant. every single post, every single time. in chronological order starting with the most recent post. note: it will not find #croissants or that time you made the typo #croidnssants. for a tag with multiple words, it’s just /tagged/my-croissant and it will show you everything with the exact phrase #my croissant

url.tumblr.com/tagged/croissant/chrono will bring up EVERY post on the blog tagged with the exact phrase #croissant, but it will show them in reverse order with the oldest first

url.tumblr.com/search/croissant isn’t as perfect at finding everything, but it’s generally loads better than the search on mobile. it will find a good array of posts that have the word croissant in them somewhere. could be in the body of the post (op captioned it “look at my croissant”) or in the tags (#man I want a croissant). it won’t necessarily find EVERYTHING like /tagged/ does, but I find it’s still more reliable than search on mobile. you can sometimes even find posts by a specific user by searching their url. also, unlike whatever random assortment tumblr mobile pulls up, it will still show them in a more logically chronological order

url.tumblr.com/day/2020/11/05 will show you every post on the blog from november 5th, 2020, in case you’re taking a break from croissants to look for destiel election memes

url.tumblr.com/archive/ is search paradise. easily go to a particular month and see all posts as thumbnails! search by post type! search by tags but as thumbnails now

url.tumblr.com/archive/filter-by/audio will show you every audio post on your blog (you can also filter by other post types). sometimes a little imperfect if you’re looking for a video when the op embedded the video in a text post instead of posting as a video post, etc

url.tumblr.com/archive/tagged/croissant will show you EVERY post on the blog tagged with the specific and exact phrase #croissant, but it will show you them in the archive thumbnail view divided by months. very useful if you’re looking for a specific picture of a croissant that was reblogged 6 months ago and want to be able to scan for it quickly

url.tumblr.com/archive/filter-by/audio/tagged/croissant will show you every audio post tagged with the specific phrase #croissant (you can also filter by photo or text instead, because I don’t know why you have audio posts tagged croissant)

the tag system on desktop tumblr is GENUINELY amazing for searching within a specific blog!

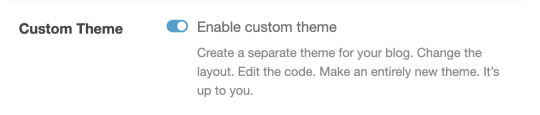

caveat: this assumes a person HAS a desktop theme (or “custom theme”) enabled. a “custom theme” is url.tumblr.com, as opposed to tumblr.com/url. I’ve heard you have to opt-into the former now, when it used to be the default, so not everyone HAS a custom theme where you can use all those neat url tricks.

if the person doesn’t have a “custom theme” enabled, you’re beholden to the search bar. still, I’ve found the search bar on tumblr.com/url is WAY more reliable than search on mobile. for starters, it tends to bring posts up in a sensible order, instead of dredging up random posts from 2013 before anything else

if you’re on mobile, I’m sorry. godspeed and good luck finding anything. (my one tip is that if you’re able to click ON a tag rather than go through the search bar, you’ll have better luck. if your mutual has recently reblogged a post tagged #croissant, you can click #croissant and it’ll bring up everything tagged #croissant just like /tagged/croissant. but if there’s no readily available tag to click on, you have to rely on the mobile search bar and its weird bizarre whims)

50K notes

·

View notes

Text

My face is having uncontrollable spasms. Great. It hurts really, really, really bad.

I think part of why I have trouble explaining pain to the doctor is when they ask about the pain scale I always think “Well, if someone threw me down a flight of stairs right now or punched me a few times, it would definitely hurt a lot more” so I end up saying a low number. I was reading an article that said that “10” is the most commonly reported number and that is baffling to me. When I woke up from surgery with an 8" incision in my body and I could hardly even speak, I was in the most horrific pain of my life but I said “6” because I thought “Well, if you hit me in the stomach, it would be worse.”

336K notes

·

View notes

Text

smartphone storage plateauing in favor of just storing everything in the cloud is such dogshit. i should be able to have like a fucking terabyte of data on my phone at this point. i hate the fucking cloud

130K notes

·

View notes

Text

I regret to inform you that Discord's new Terms of Service includes an arbitration clause. You can find it here https://discord.com/terms/#16. This clause includes an opt-out, which I have transcribed here:

You can decline this agreement to arbitrate by emailing an opt-out notice to [email protected] within 30 days of April 15, 2024 or when you first register your Discord account, whichever is later; otherwise, you shall be bound to arbitrate disputes in accordance with the terms of these paragraphs. If you opt out of these arbitration provisions, Discord also will not be bound by them.

These clauses are underhanded ways that corporations seek to deprive you of your right to participate in class-action lawsuits and your right to a jury trial. (This does only apply to us users ,other people still spread the word though )

49K notes

·

View notes

Text

When you order Blonde Slut Espresso:

3 notes

·

View notes

Text

Aizen: I'm just an uwu helpless baby in this chair.

41 notes

·

View notes

Text

being attracted to blond men is a sign something is really wrong with your psyche

28K notes

·

View notes

Text

that butler: Gay Hogwarts Arc

7 notes

·

View notes

Text

PSA: Don't use Open Office

I keep seeing people recommending Open Office as an alternative to Word, and uh... look, it is, technically, an open source alternative to Word. And it can do a lot of what Word can, genuinely! But it is also an abandoned project that hasn't been updated in nine years, and there's an active fork of it which is still receiving updates, and that fork is called LibreOffice, and it's fantastic.

Seriously, if you think that your choices are either "grit your teeth and pay Microsoft for a subscription" or "support free software but have a kind of subpar office suite experience", I guarantee that it's because you're working with outdated information, or outdated software. Most people I know who have used the latest version of LibreOffice prefer it to Word. I even know a handful of people who prefer it to Scrivener.

Open Office was the original project, and so it has the most name recognition, and as far as I can tell, that's really the only reason people are still recommending it. It's kind of like if people were saying "hey, the iPhone 14 isn't your only smart phone option!" but then were only ever recommending the Samsung Galaxy S5 as an alternative. LibreOffice is literally a version of the same exact program as Open Office that's just newer and better – please don't get locked into using a worse tool just because the updated version of the program has a different name!

59K notes

·

View notes

Text

ACA Enrollment Cheat Sheet!

so it’s open enrollment time, which means you need to pick a health insurance plan from the exchanges! it can be daunting as shit, for sure, especially if you don’t live in the filthy weeds that are the business side of our garbage health care industry like yours truly does.

so! here’s a quick rundown of some of the vocabulary:

premiums: this is what you pay per month for the glorious honor of having insurance coverage. it does not count towards your deductible or out of pocket maximum. depending on your income, you may be eligible for a subsidy or other financial assistance to make your premiums more affordable.

deductible: this is how much in health care costs you have to pay before your insurance starts really kicking in. for example, my insurance through work had a $1,500 deductible, so the copays and coinsurances and lab costs that i had to pay early in the year, before i had another surgery, were fully my responsibility until i’d paid out $1,500; after that, my insurance started covering a flat 80% of everything, including copays. basically, the deductible is how many actual dollars you have to pay out for medical costs before your insurance takes over.

if you’re someone who goes to the doctor a lot, like me, you’re probably going to want a plan with a lower deductible, which will have a higher premium; however, in the long run, you’ll come out more ahead with a high premium/lower deductible.

on the flip side, if you’re generally healthy and just need an annual checkup, flu shot, ob-gyn annual, etc., then you probably want a lower premium/higher deductible plan.

out of pocket maximum: this is the cap on how much– aside from premiums– you should have to pay in health care costs in a year. most plans on the exchanges right now have a high deductible and higher OOP max.

network: this is the collection of providers (doctors, surgeons, urgent care facilities, imaging facilities, etc.– any clinical medical care or medical service provider) that are contracted with the insurance plan. this means that they have an agreement with the plan to accept payment from that plan for services. you can still see out of network providers, but your plan may have a separate out of network deductible that is higher and that you pay separately from your main deductible (for example, if your plan deductible if $5,000, you might have a separate out of network deductible of $5,500; even if you’ve already paid of $4,950 of your regular deductible, if you see an out of network doctor, you’re going to have to hit the $5,500 deductible in copays and whatnot before the insurance covers them fully).

most insurers have their own website that identifies what doctors are in network. sometimes you can access this without being on the plan already, sometimes you can’t. a decent, though inconsistent, workaround is to use zocdoc, where you can put in the plan type you’re thinking about switching to and see what doctors are in network. the drawback to zocdoc is that contract status is doctor-reported, so if the doctor’s office in question is slow to update, the records may be out of date.

another option to determine network availability for a specific doctor or care group is, if you’re okay hopping on the phone, to just give them a call and ask outright if they’re going to be in network for plan ___ in 2018.

if you’re like me and hate talking on the phone, the other option is that large provider groups, and a good number of smaller groups and individual providers, will often also have accepted insurances on their websites. in my experience almost all providers who have privileges at a hospital will have that listed on their pages on the hospital’s website.

copay: this is a flat fee you pay to a provider when you see them. it’s like the cover charge at a bar: you pay $20 to get in the door, and then you get the dubious honor of also paying for the drinks and food you buy inside on top of that.

coinsurance: this is a percentage charge for seeing a provider. instead of a $20 copay for the cost of the visit to see doctor bob, you’re charged, say, 10% of the total cost of all charges associated with you visit to see doctor bob. if you don’t get much done, this may only like $10; if you get a full metabolic panel run and a bunch of xrays, it might be $100.

and the plan types:

hmo: health management organization. the concept of this plan is that you have a pcp (primary care provider - your regular doctor) who functions as your primary point of contact for all medical care. if you want to see a non-pcp doctor, you have to first see your pcp, who will write you a referral to see said specialist. specialists include orthopedists, physical therapists, neurologists, ob-gyns, etc. - any provider who isn’t your pcp, basically.

hmos tend to be cheaper for you, the beneficiary

this is because of how they’re paid out: pcp doctors receive a capitation (aka, a set flat amount) payment from the insurer for each beneficiary (you) who has them as a pcp.

so, if i’m a primary care doc and i have 200 blue cross hmo patients and i get $100 per patient, i get $20,000 from blue cross, ostensibly for the cost of care provided, but the provider keeps all $20,000 even if they only end up incurring $15,000 in costs. the downside of this for you as a patient is that this encourages pcps to get a lot of people to sign up as their patients, and then to see them as little as possible/push them out to specialists for actual care, as this lowers their costs and increases their revenues.

you may end up feeling like you’re going in circles trying to get actual care because you’re getting pushed from one doctor to another.

note: hmo plans sometimes do not cover out of network providers at all.

ppo: preferred provider organization. this plan is a free for all: if they’re in network, you can go to whomever you want. they tend to be a bit pricier (almost always on premiums, 50/50 on deductibles) than hmo plans, but you’re basically paying for ease of access. you can make an appointment directly with any specialist you so choose. these plans are ideal for people like me, since i have to see orthopedists and hematologists and physical therapists pretty regularly, and going through a pcp for each of those would be a pain.

you’ll tend to have relatively low copays within the network and higher ones outside of it

unlike some hmo plans, most ppo plans will provide coverage for out of network providers, just at a less favorable rate

epo: exclusive provider organization. this is the bastard child of the hmo and ppo and is also an increasingly common option on most of the exchanges. like a ppo, no pcp or referrals are provided; however, the network tends to be narrower and you have less choice of in-network providers and, crucially, they don’t tend to cover any out of network providers except for emergencies

important note: the classification of “emergency” isn’t just “emergency situation”, but generally is limited to a proven medical emergency in which you go to an actual emergency room or emergency department.

insurers will frequently challenge ER/ED bills to confirm medical necessity because–

in their defense, since they’re meant to cover almost the entirety of emergency bills and also because one of the quantifiable measures of success in moving to value-based care that the ACA established is lowering avoidable ER/ED admissions

–they don’t want to encourage people to go the ER/ED for just anything

high deductible/catastrophic: these are exactly what they sound like– plans for healthy young people who are pretty much only going to wind up with medical costs if something terrible and, well, catastrophic, like a car accident, happens. they have low premiums and very high deductibles (often approaching ~$10,000). these are only available to people under the age of thirty, because clearly as soon as you turn thirty you must turn into a total drain on all healthcare resources :|

so what does all of this boil down to for you and your enrollment?

start by figuring out what financial help you’re eligible for! the exchanges generally have an option at the front end of the process for you to identify your annual income and number of dependents on your plan. this will let you know if you’re eligible for a subsidy or other financial help, and, if so, how much; you should also have an option when searching through plans on the exchanges to input estimated financial help, which will adjust the premiums in the search engine.

after that, start digging into the individual plan options. every exchange plan should provide a summary of benefits and coverage. it’ll be a pdf and will look like this:

that red circle in the top right there? that’s where you can identify what type of plan you’re looking at. the first page in the summary of benefits will always look the same– it’s the basic overview of the costs and definitions.

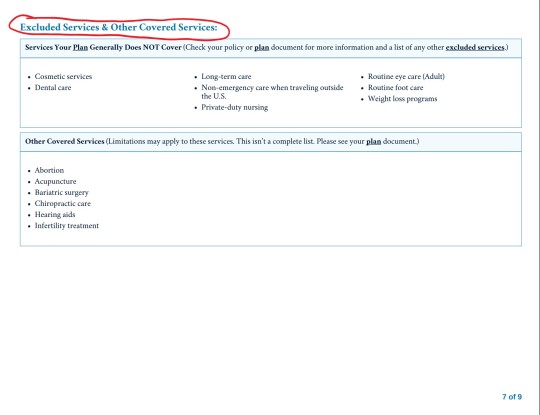

this document will also list excluded services. it’ll generally be somewhere in the middle/back half of the document and will have a clear header like this:

for me, this is the first thing i look for after verifying premium and deductible amounts. as the above picture indicates, you can find more information in the plan documents. these aren’t always directly linked to on the exchange website, but you can generally find them on the insurance providers website. these will be a lot more detailed and can be anywhere between twenty and 200 pages. ctrl + f your heart out: as frustrating and complicated as insurers can be, they can’t actually fail to disclose if they, for example, don’t cover all forms of contraceptives. they’ll disclose it in the plan documents, even if they don’t, unfortunately, have to be clear and up front about it.

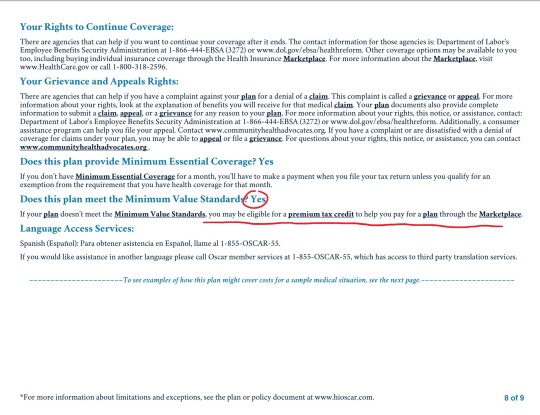

NOTE: MINIMUM VALUE STANDARDS

towards the end of the summary of benefits document will be a page that looks like this:

minimum value standards roughs out to basically meaning that at least 60% of all medical charges are covered. if the plan you’re on does not meet minimum value standards, you might be able to get a tax credit to help you buy another marketplace plan. always check for this verification when you’re researching plans.

what does all of this shit mean?

it means start here and then find your state’s exchange from there. the garbage carrot in chief established “maintenance times” on this website throughout the open enrollment period (sunday afternoons, i believe), so schedule around that. sit down on a monday or wednesday or saturday with some snacks and a cup of your favorite beer/wine/tea/whathaveyou and crank up some good music to jam to and do some research:

start with figuring out what you can afford monthly and if something terrible happens and you have to cover ER and/or surgery bills

if you have a specific doctor you want to stay with, figure out which insurances they’ll be accepting

check for coverage info in the summary of benefits documents and, if you want more detail, in the plan documents

narrow it down to a few and compare the prices

take a break and have a cookie, you deserve it at this point

pick a plan! if you’re not feeling super certain about it, go for a walk, do some laundry, pet your cat– just take a break, walk away, come back to it with fresh eyes. this is a big deal, so you don’t want to wear your brain out and give yourself a headache and then just pick one at random because you have eye strain and want to be done. open enrollment goes until december 15, so don’t rush yourself.

sign up for your plan

have another cookie and pat yourself on the back, because you just signed up for health insurance for 2018!

now take a nap because that was fucking exhausting and you deserve it

as always, i’m here for any questions you might have!

if i don’t know the answer, i can point you towards someone or some resource that will. don’t be afraid to ask me or anyone else for help! this is a complicated situation and even though the current administration is trying really hard to make it worse, there are still always resources available to you for help and guidance. all you have to do is ask :)

16K notes

·

View notes

Text

the Quincy way // I see some parallels in Uryu's approach to Orihime when it comes to Jugram/Nanao

The Quincy Way:

Inability to express an emotion and say it out loud but still love.

#bleach#IseHasch#the fact he wanted Nanao to mark him so badly // this is such an internal convo tho // if you know you know#the quincy urge to be marked bc their king did it first

6 notes

·

View notes

Text

the Quincy way // I see some parallels in Uryu's approach to Orihime when it comes to Jugram/Nanao

The Quincy Way:

Inability to express an emotion and say it out loud but still love.

#anime manga rambles#not tagging the anime or should i because very ship specific and fic specific to mine so#isehasch#i want to a moment with ryuken too bc all pretty boy quincies share one melancholy look tm

6 notes

·

View notes

Text

Ukitake when Stark called Lilynette over: I could have adopted that child!

3 notes

·

View notes